Market volatility has affected banks internationally in the US, UK and Europe but even though Australian banks remain insulated from turbulence abroad it might not be all smooth sailing.

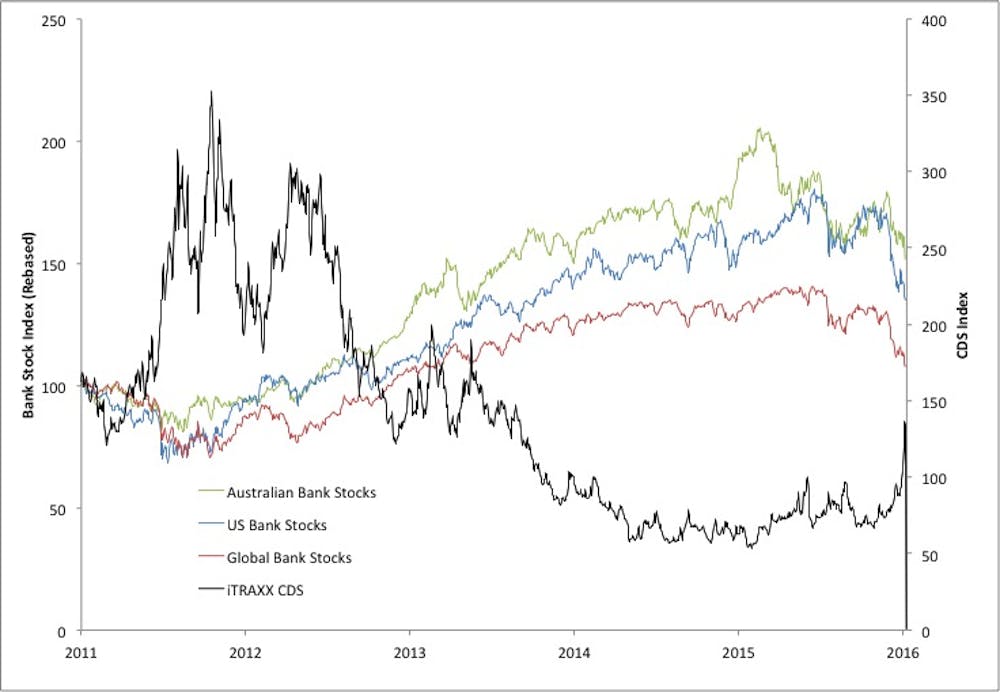

The MSCI index of global banks has fallen by 16% since the start of the year, while the S&P index for US banks has fallen by 20%. The chief executive of Deutsche Bank (one of the world’s largest banks) was forced to announce that his bank was “rock solid” after the share price had fallen more than 30% from the start of the year and rumours circulated of problems with contingent convertible (CoCo) bonds.

The fall in international bank stocks has coincided with a perception of rising risk levels within the banking sector. The iTRAXX CDS index indicates the cost of insuring debt for a selection of global banks – the index increases as the cost of insurance becomes more expensive, indicating the market perceives that the debt is riskier. So far this year the index has risen 65% - the sharpest increase since the European sovereign debt crisis of 2011-12.

Falling commodity prices are the current focus

The main source of concern for financial markets at the moment is related to the commodity markets. Past high commodity prices encouraged many firms to invest heavily building huge new mines, liquefied natural gas (LNG) plants, and expanding production in shale oil. This investment required large amounts of borrowing, and banks have provided this directly (loans) and indirectly (purchasing bonds).

In the last year, crude oil prices have fallen 54%, LNG prices have fallen 32%, and iron ore prices are down around 30% (according to Datastream). The result is that many of the projects, some of which are still to come online, are not profitable – some may never be profitable – and the debt may not be repaid.

Credit ratings agencies such as Moody’s suggests that much of the debt issued by U.S. energy companies will be downgraded to junk in the near future, while Standard & Poor’s stated that debt at Chesapeake Energy (one of the largest US shale producers) is unsustainable.

Attempts by the Chinese government at intervening in the currency markets have also created volatility for banks. This has served to create a sense of uncertainty within the financial markets – and when this is the case there is often a reduction in the willingness to invest in “risky assets” such as stocks. Unlike in 2008, heavily indebted governments will have much less ammunition to bail out banks that fail this time around.

Longer term, the change in the regulatory environment is affecting the risk-taking ability of banks, and reducing profitability (even viability) of many areas. Increased capital requirements, particularly in areas that regulators deem to be too risky, mean that many banks are exiting equity, fixed income, and currency trading – divisions that have previously generated substantial profits for banks.

Of course, there is also ongoing regulatory investigation into a variety of cases of apparent financial market manipulation such as the recent LIBOR, and Foreign Exchange, fixing scandals that saw heavy fines imposed on US and European banks. This has even spread to Australia, where ANZ appears to be under investigation by ASIC for possible interest rate rigging.

Meanwhile in Australia

In Australia, banks have performed very well over the course of the last five years. At one point in 2012 Australian banks were worth more than the whole of the European banking sector! Record levels of profitability in Australian banks have supported large dividend payments to shareholders and helped push share prices to all-time highs in 2015.

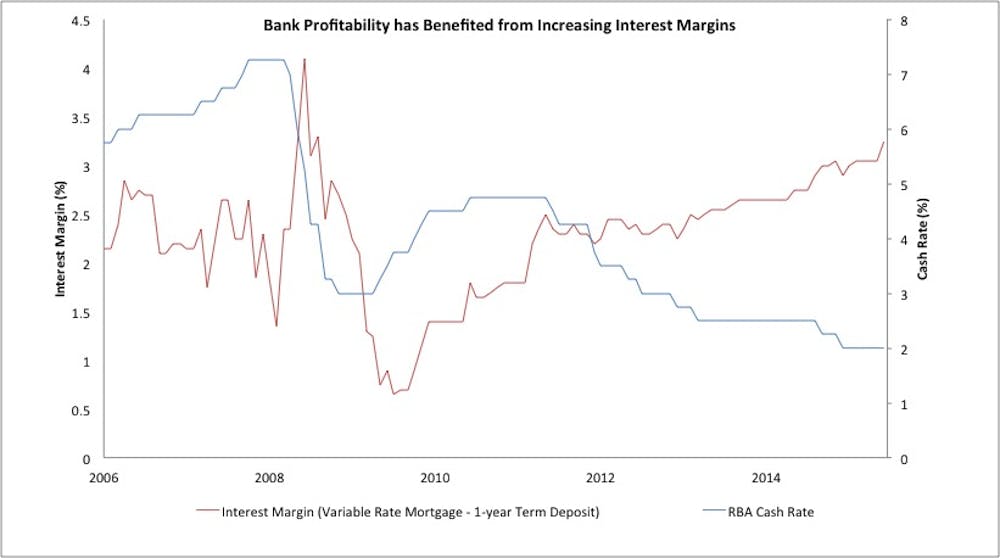

Earlier this week, CBA announced another rise in earnings for the first half of the year – to A$4.8 billion. Much of this profitability is a result of increasing interest margins. As the Reserve Bank of Australia cash rate has fallen, banks have been quick to cut the rates offered to savers, but slow to pass on the rate decrease to borrowers (if they have done so at all). Even a small increase in this margin can boost profits if total assets are measured in the hundreds of billions of dollars.

However, this profitability may not last as margins are under pressure on two counts. First, tighter lending standards, particularly for investors, have slowed lending in the housing market. The housing market appears to be slowing and this may increase bad debts in the future.

Australian banks are not totally immune to the impact of falling commodity prices, and CBA with ownership of Bankwest may be particularly exposed to a slowdown in Western Australia.

On the other side of the coin, funding is becoming more expensive for banks at the same time that increased capital requirements require them to hold more. Funding through international sources is particularly scarce (the CDS index indicates this is becoming more expensive), and this matters because Australian banks require a substantial amount of offshore funding.