There are now 116,000 non-doms. It is costing at least hundreds of millions of pounds to our country. And it cannot be justified. It makes Britain an offshore tax haven for a few.

Ed Miliband, Labour party leader in a speech at the University of Warwick

The Labour party wants to abolish the non-domiciled (non-dom) resident status for UK tax purpose. This includes removal of some or all of the tax advantages that non-doms enjoy, including the “remittance basis” which means they can avoid paying tax on income outside the UK.

People can claim non-dom status if they were born outside the UK, but now live here. The status, which has been around for 200 years, can also be inherited through the father. Ed Miliband, the leader of the Labour party, claimed that the reform would raise “hundreds of millions” for the UK. However, in January 2015 shadow chancellor Ed Balls contradicted the campaign by saying that scrapping the rule “would cost Britain money”. If the non-dom status is abolished using a cold-turkey approach, many non-doms may leave Britain, which could result in huge losses to the economy.

Miliband later explained that the Labour party proposes to scrap the rule giving non-doms a transition period of around two years to “get their affairs in order”.

Current non-dom tax policy

UK residents with non-dom status can currently choose whether to pay taxes in Britain on their overseas earnings. Although they are already taxed in full on their UK income and capital gains, they can opt to be taxed on the remittance basis, which allows them to pay an annual fee to avoid tax on their overseas earnings.

In particular, claiming the remittance basis implies that the non-dom loses tax-free allowance for income and capital gains in the UK, and pays an annual charge depending on how long they have been in the country. The fee is £30,000 if resident in the UK for at least seven of the previous nine years, £60,000 for 12 of the previous 14 years, or £90,000 for longer stays. Non-doms also enjoy favourable treatment of non-resident trusts.

According to the most recent available data from 2012-13 from HMRC, the Institute of Fiscal Studies, and law firm Pinset Masons, the HMRC raised £8.2 billion from the 114,800 people who claimed non-dom status in the UK, which amounts to 5% of the total revenue from income tax collected by the HMRC.

Only 46,700 non-doms took advantage of the remittance basis and 5,100 of them are paying the fees. More of them are not paying the charges presumably because they have lived in the UK for less than seven years. Only 19% of the total £226m total HMRC received in charges were paid by 3,700 non-doms who had lived in the UK for seven to 12 years. The remaining £183m was paid by 1,400 non-doms who had lived in the UK for more than 12 years.

According to figures released with the 2014 autumn statement, a recent increase to the fees from April 2015 will raise a further £90m a year from those who have lived in the UK for more than 12 years.

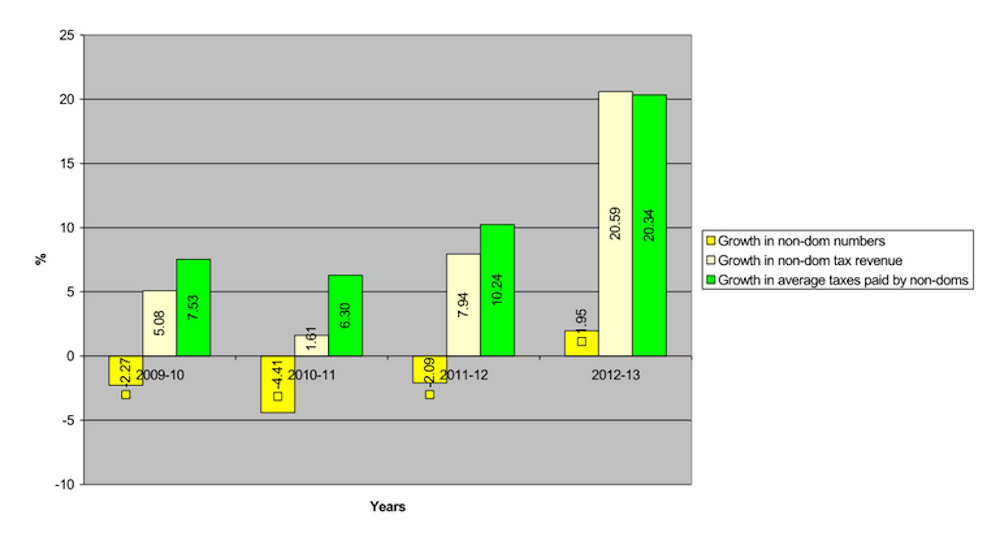

In the UK, the number of non-doms in 2013 was 6.7% less than that in 2008, the year when the remittance basis and the charges were introduced. Between 2008 and 2013, the total revenue and the average revenue per person in taxes from non-doms increased by 39% and 51.6%, respectively. Following the introduction of the charge, in the past six years the UK has experienced a 1.7% average decline in the number of non-doms per year, together with 8.8% average growth in the total tax revenue from them, as the graph below shows.

Abolishing non-dom status

There are some potential sources of additional revenue from Labour’s proposed reform. The 5,100 non-doms who had lived in the UK between seven and 12 years who pay the fees do so because it is less than the taxes on their unremitted income or capital gains would be if they were domiciled in the UK.

The majority of this group of non-doms have lived in the UK for a relatively short period and therefore may face a high cost of migration, because their “sunk cost” is high and they have not lived long enough to recover it. So the proposed reform, if implemented effectively, is likely to collect higher revenue than the total proceeds from the charges paid by this group – currently £43m.

The relatively more settled fee-paying non-doms – currently 27.5% of the total – can leave the UK incurring very low cost – because they have already spent more than 12 years in the UK to recover their sunk costs. If the majority of the fee-paying non-doms – the ones who have lived less than 12 years – remain in the UK and pay taxes accordingly, it is likely to increase the total proceeds from this group.

However, this depends largely on HMRC’s set of information on the unremitted income and gains of non-doms in other countries, which is not available because currently the fee-paying non-doms do not have to disclose these. Similar uncertainty (due to lack of information) is associated with the removal of the tax advantages on non-resident trusts.

Verdict

Whether the proposed reform will generate “hundreds of millions of pounds” for the UK remains uncertain. Apart from the extreme response of leaving the UK, it is likely that the non-doms will pay accountants to avoid taxes. That will add to the existing costs of foregone revenue from and tax compliance of the non-doms, and therefore may result in loss of total revenue.

Other behavioural responses, such as transferring assets to family members abroad, spending more time abroad, or utilising the non-resident trusts more, may also add to this loss. The “higher end” non-doms, who can explore any other tax-haven and can buy a good life in any other location (such as the Middle East) can leave the UK at any stage of their residency. It is therefore very likely that following the reform, HMRC will not be able to raise the projected £90m every year from the charges.

The net revenue effect of this proposed reform remains uncertain, and the claims made by the Labour party are too premature, and to some extent, misleading. We need more details before assessing the credibility of the projection of revenue-gains from this reform.

Review

There is no question that this is extremely difficult to calculate with any precision for two reasons. First, a lack of relevant information about offshore assets owned by non-doms. It is such assets that give rise to the income and capital gains which are potentially to be brought into the UK tax net under the proposed changes. It’s also not known to what extent such income and gains will be sheltered by double tax relief for tax paid in the country of origin.

Second is the behavioural response of the non-doms, which will be mixed depending on the circumstances. Non-doms are not a homogeneous population and their motivation for remaining in the UK either physically or for tax purposes is not uniform, so their response to any change won’t be either.

To suggest, however, that being a non-dom who at present is claiming the remittance basis indicates a propensity to avoid tax (“will pay accountants to avoid taxes”) is not entirely appropriate.

Click here to request a check. Please include the statement you would like us to check, the date it was made, and a link if possible. You can also email factcheck@theconversation.com