One issue that has attracted growing attention in recent years is the “gender pension gap” – the fact that on average, women have lower private pension wealth and lower income in retirement than men. But before rushing to conclusions about how to “fix” this, it is crucial to understand what lies behind any pension differences between men and women.

There are three main potential drivers behind this phenomenon:

Different labour market experiences: the “gender pay gap”, and the fact that men have longer paid working lives than women;

Different investment strategies: when it comes to defined contribution pensions, men choose to invest in portfolios with a higher expected rate of return.

Different saving rates: as we investigate below, men and women may also differ in how likely they are to be offered a pension in their job, or tend to work for employers that contribute more or less to a pension, or tend to make different contributions themselves.

Importantly, the role of these potential drivers will have changed over time for various reasons. Mothers have increasingly participated in the labour market over the years, for example. Final salary pensions have been reformed to career average schemes, which in particular reduced the generosity for long stayers and those with stronger pay growth, affecting men more than women. Also, automatic enrolment has been introduced for workplace pensions, which affected everyone’s participation in them.

Gaps in pension income today may therefore reflect labour markets and pension arrangements from many years ago, and the gap in pension income for current working-age individuals may be quite different when they reach retirement. In an ongoing programme of work at the Institute for Fiscal Studies, funded by the Nuffield Foundation, we are examining in detail differences in pension saving rates between men and women that will contribute to a future “gender pension gap” for today’s working age individuals.

Making sense of the gap

In a first publication, we have documented differences in average pension saving between male and female employees before the introduction of automatic enrolment in 2012. We found that on average across all employees (whether saving in a pension or not), women of all ages actually contributed more as a proportion of their earnings each year than men.

However, this was driven by the fact that women were more likely to work in the public sector, where contribution rates are typically higher. Examining average pension saving among men and women within each sector reveals a different pattern. The average saving rates of male and female employees were similar until around age 35 but then diverged, with average contributions continuing to increase with age for men but not changing for women.

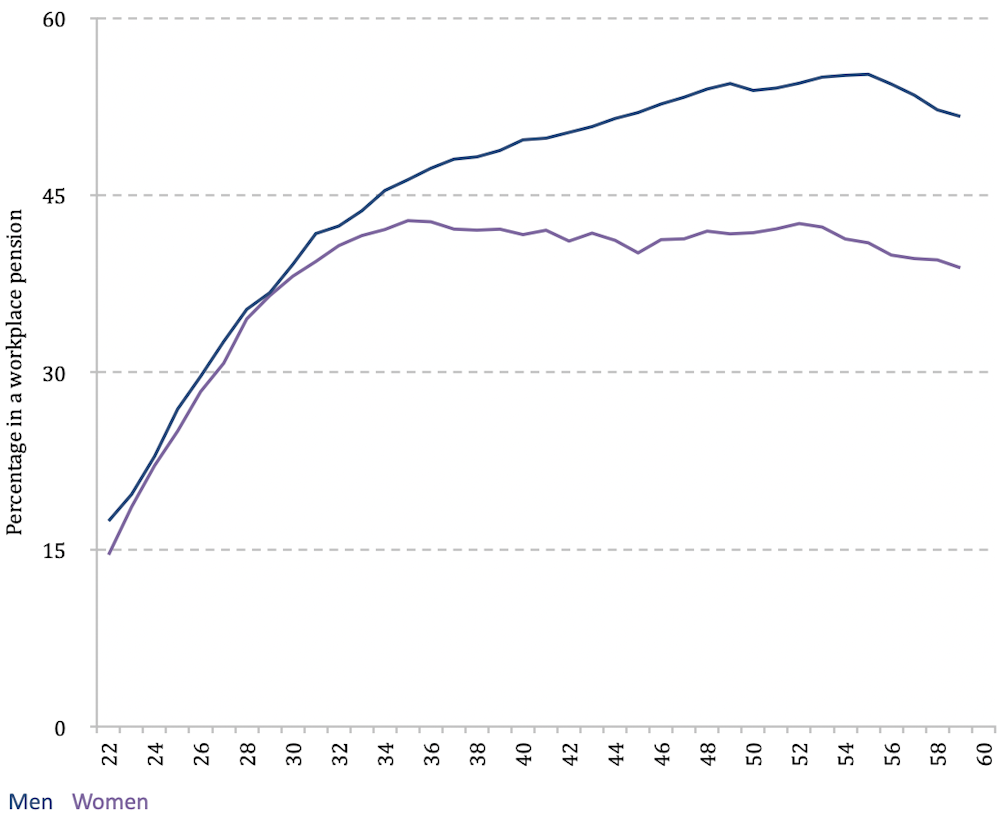

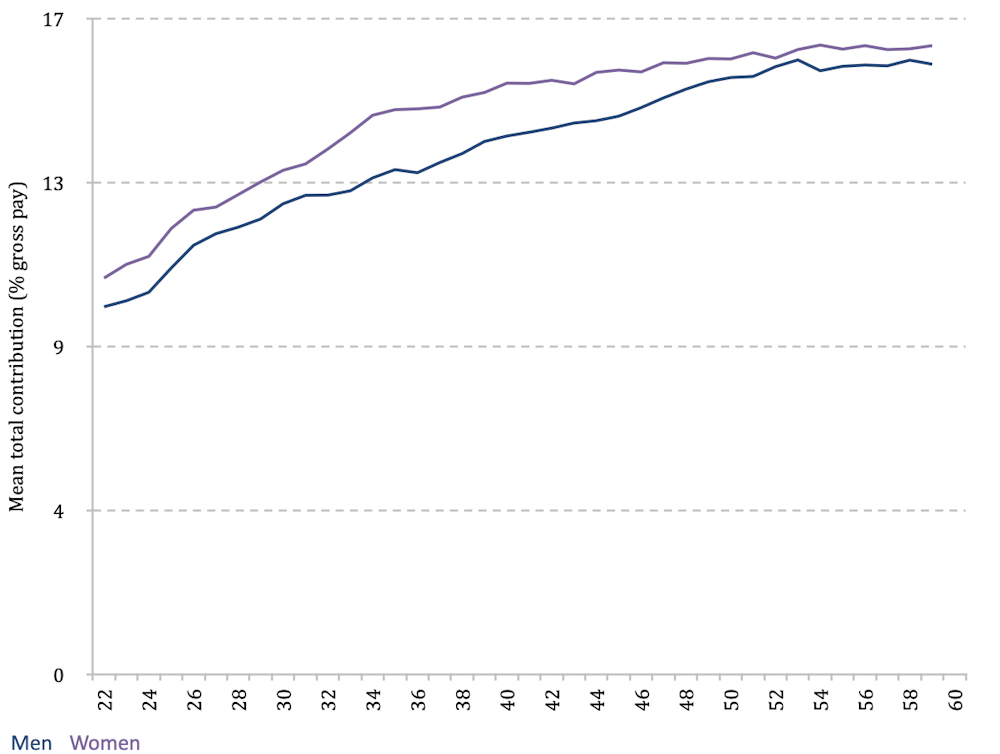

The graphs below unpick what was driving this pattern among private-sector employees in Great Britain (though the pattern was broadly similar for public-sector employees). It was caused by the extent to which men and women participated in a pension.

The proportion of men and women saving anything in a private pension was similar until around age 30 but then diverged, with men increasingly likely to be saving in a pension as they get older, while women’s pension participation plateaued. On the other hand, average contribution rates for those saving in a pension were actually slightly higher as a share of earnings among women than men.

Pension participation in overall savings

Average contribution rates in pension savings

What might have been driving differences in pension participation? The timing of the divergence in people’s lives mirrored the evolution of the gender gaps in pay, commuting and firm productivity, and suggested that the arrival of children and related employment decisions was an important factor.

So in our ongoing programme of research we are examining whether the gap in pension participation is associated with the arrival of children, and the extent to which female employees received a different pension offer from their employer, or made different saving decisions when presented with the same offer as male employees.

Effect of automatic enrolment

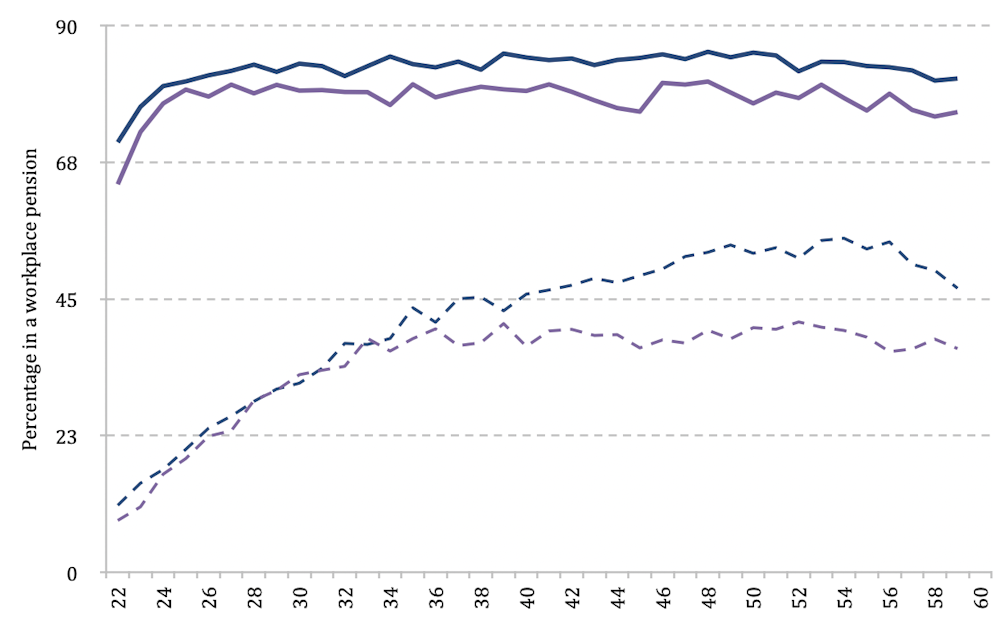

The introduction of automatic enrolment into workplace pensions has substantially changed pension-saving behaviour – in particular, substantially increasing pension participation among employees targeted by the policy. The graph below shows the proportion of male and female employees of different ages who were saving in a private workplace pension in 2012 and 2019 in Great Britain.

The pattern in 2012 is represented by the two sets of dashed lines, with men again in blue and women in purple. It is similar to that estimated in the first graph in this article.

But the pattern in 2019 is totally different. Rather than participation diverging at a particular age, women are now slightly less likely to be in a pension at all ages than men (but the level of participation among both is considerably higher). Automatic enrolment will therefore have fundamentally changed the nature of the gender gap in pension-saving rates going forwards.

Pension participation 2019 vs 2012

This highlights the importance of examining gender differences in saving rates, rather than just accrued pension wealth or pension income. Focusing on the latter risks developing policies to fix a perceived problem that has already changed.