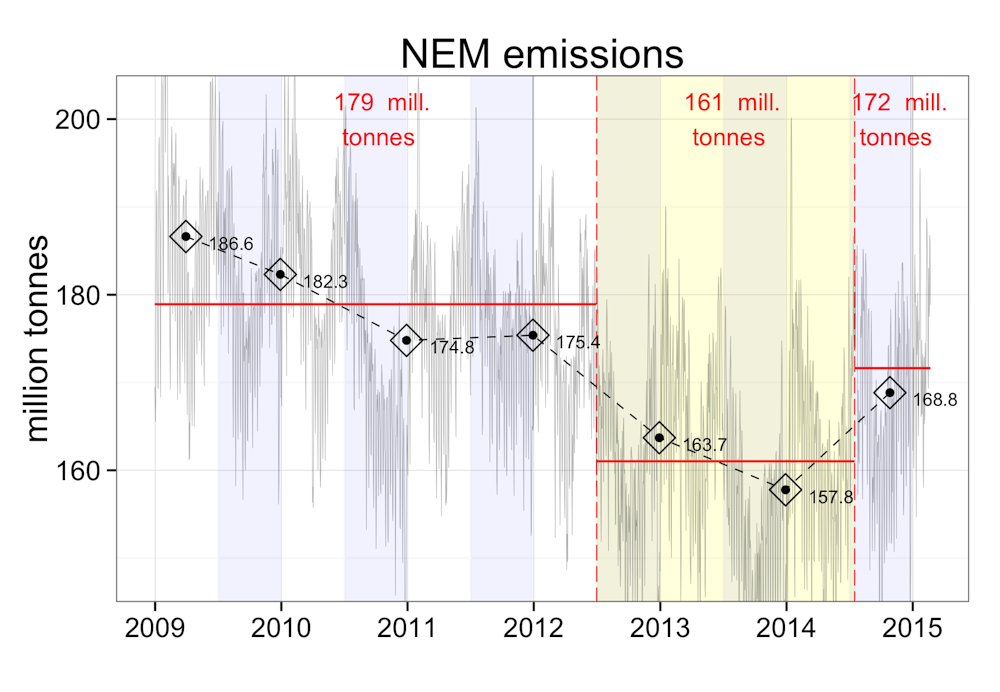

Several factors combined to deliver seemingly astonishing reductions in Australian electricity sector emissions over the carbon tax years. With those gains now being reversed, as shown in the figure below, we might ask what we learnt from our experiment with carbon pricing? One insight that has received little comment to date, is the tantalising glimpse carbon pricing provided of the Tasmanian opportunity as a net electricity exporter in a carbon constrained world.

First some background on electricity sector emissions, reiterating some of the points made in several of my previous posts.

As now well documented, one of the factors responsible for emissions reductions in recent times, including the carbon tax years, has been the falling demand for grid based electricity. From 2009 demand on the National Electricity Market - or NEM - has fallen at an average annual rate of 1.7% or 350 megawatts. Declining demand has contributed a drop in annual NEM greenhouse gas emissions of about 3 million tonnes each year [see note 1].

But it was changes in the mix of generation that really helped drive NEM emissions down during the carbon tax years. Compared to the year before carbon pricing hydro output increased by around 460 megawatts while wind output increased by 220 megawatts [see note 2]. Together they accounted for a reduction in emissions of about 7 million tonnes over the year.

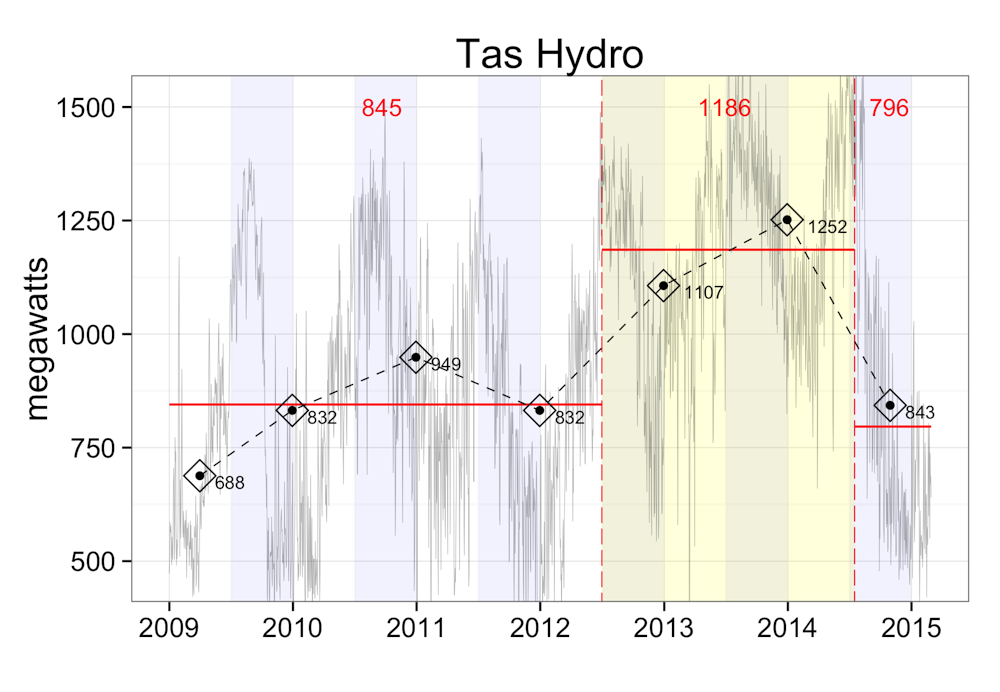

However, the catch was that the level of hydro output during the carbon-tax years couldn’t be sustained.

Since repeal of the carbon tax, hydro output has dived by around 590 megawatts, with some 390 megawatts due to Tasmanian hydro reductions. Importantly, the draw down of hydro reservoir capacity during the carbon tax years meant hydro output needed to be curtailed independently of repeal.

The cost we are now paying is an additional 5 million tonnes to be added NEM emissions in this financial year, along with a dramatic reduction in hydro revenues.

What happened to Tasmanian hydro?

Tasmanian hydro power is central to this. To understand we need to go back to mid 2009 and the end of the Millennium drought.

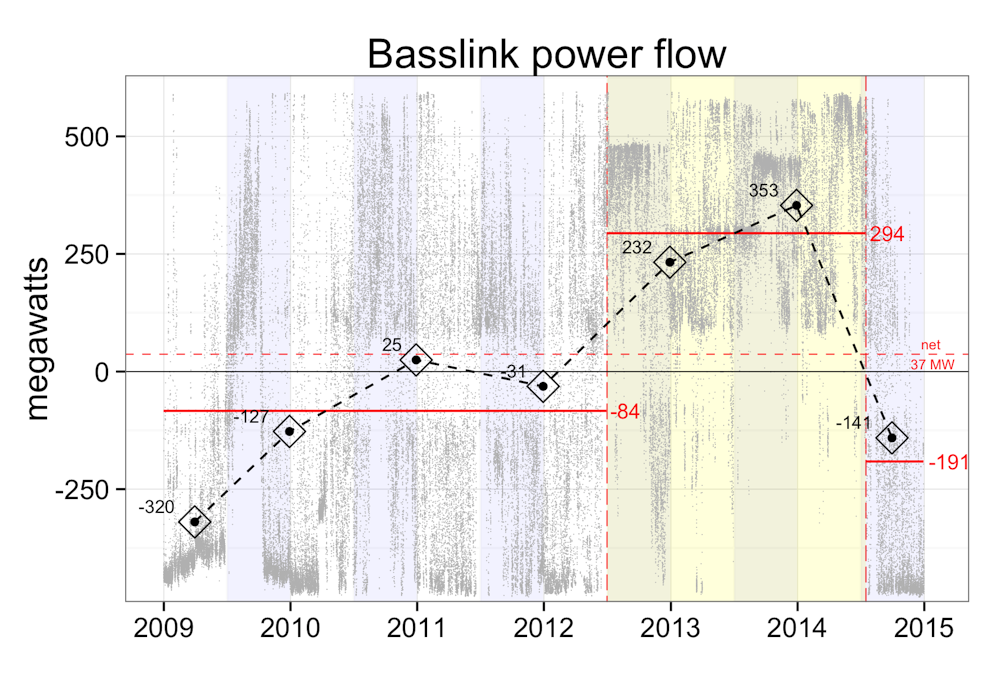

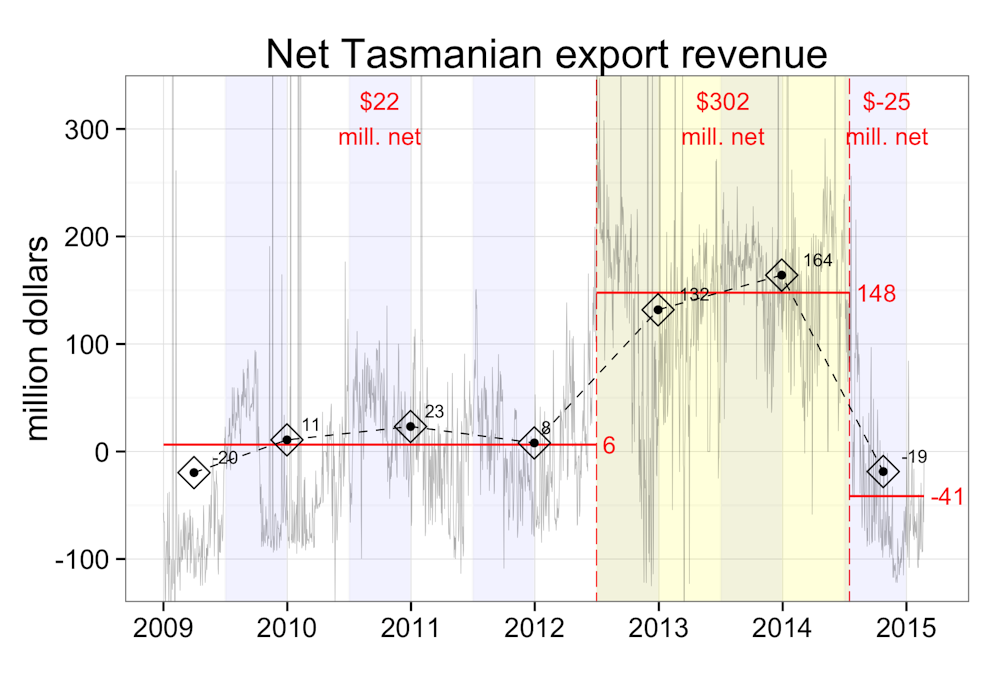

Through the last stages of the Millenium drought, as much as 30% of Tasmanian power demand was supplied by imports from Victoria via the Basslink Interconnector. In the first six months of 2009, the net power flow across Basslink was directed southwards at an average rate of more than 300 megawatts - or about 2/3 the full southbound capacity of the link. Some northbound hydro output was dispatched into Victoria during the extreme spot price hikes that accompanied the heatwaves of early 2009. In the first half 2009, the arbitrage return limited the net cost of power exchanges to Tasmania to $22 million in wholesale market terms.

By FY2011-12, following breaking of the drought, increases in hydro output resulted in a reversal of the net flow across Basslink. Some judicious banking of hydro reserves in FY 2012-13 was supported by net imports. Net revenue flow on wholesale exchange across Basslink was in Tasmania’s favour, but only to the tune of $8 million partly because the arbitrage opportunity on the Victorian wholesale market collapsed on the back of falling demand and a relatively mild summer.

During the carbon tax years the Tasmanian hydro operators (wisely) capitalised their resource by sending hydro power north at unprecedented rates. The northward flow across Basslink averaged almost 300 megawatts across the carbon pricing years with the windfall for Tasmanian generators valued at $302 million in wholesale market terms.

By mid 2014, hydro capacity was so depleted that Tasmania has since had to resort to importing electricity. In the fourth quarter of 2014, Tasmanian imports averaged 320 megawatts with annualised change from the previous year’s fourth quarter amounting to a staggering 688 megawatts. Since repeal the balance of flows across Basslink is costing Tasmania around $41 million in wholesale terms on an annualised basis.

The reversal of net flow on Basslink since repeal has provided a boon for Victoria’s long-suffering Latrobe valley generators. Despite a fall in Victorian demand of around 400 megawatts, output from the Latrobe Valley has increased by around 300 megawatts or about 6% since repeal [see note 1]. For the first time in at least the last six years, the combined output from the Latrobe generators is on target to exceed Victorian demand over FY2014-15, by 200-250 megawatts.

Sustaining Tasmanian exports

The policy uncertainty surrounding carbon pricing, and more recently the Renewable Energy Target, has effectively quelled appetite for investment in new low emission generation in Australia over the last few years. Consequently, temporal fuel-shifting generation, for little long-term climate benefit, was all that was possible and the hydro generators played their hand to the maximum, arbitraging off the carbon price uncertainty. Having borrowed those emissions reductions from the future, we are now repaying the debt as we wait the the dams to refill.

However, in doing so, we have glimpsed an opportunity for Tasmania in a carbon constrained world as a net energy exporter. Not without some sense of irony, Tasmania’s long investment in hydro makes it the greenest, low-emission power supplier in Australia by a very long margin.

As a window into a carbon constrained world, the last few years have shown us just how well positioned Tasmania is by virtue of being connected via Basslink directly into one of the developed world’s most emission intensive jurisdictions - namely Victoria.

The catch is that over the long-term Tasmania has only enough generation capacity to provide for itself. With its power supply vulnerable to the vicissitudes of the seasonal rainfall variability, the primary roles of Basslink to date have been to provide Tasmania with security of supply and, for its generators, a market arbitrage opportunity.

But the carbon pricing years show how Basslink also provides Tasmania with the infrastructure for sustained export of electricity, should it increase generation capacity.

Hydro has particular value in managing electricity systems in a carbon constrained world. With its large storage capacity, and ability to adjust output quickly, it provides the battery potential to firm more variable generation such as wind power. Indeed, the inherent value of wind is increased by coupling with a large dispatch-able storage system such as hydro. Consequently Tasmania potentially provides one of the best investment opportunities for wind generation in Australia.

With Basslink able to sustain around 500 megawatts of additional northward flow, Tasmania could accommodate an investment of as much as 1400 megawatts in new wind, assuming a wind resource with a capacity factor of around 35%.

Such an investment would cost around $2.8 billion for the generation capacity plus some for the local transmission extension to connect into Basslink. It would provide around 2000 job years during the build phase, up to 300 ongoing jobs and, depending on the cost of carbon, return around $150 - $250 million each year in wholesale market returns and a similar amount in Renewable Energy Certificates.

An additional 1.4 gigawatt capacity delivering on average 500 megawatt output, firmed by the existing hydro capacity, would generate an additional 4,400 gigawatt hours of reliable power each year, representing over 10% of the current large scale RET target, currently enshrined at 41,000 gigawatt hours.

And the clincher for Tasmania - the investment could be entirely paid for by mainland consumers. As we glimpsed during the carbon tax years, the northward flow electrons is one way of exciting the southward flow of dollars for much needed investment in Tasmanian industry.

What needs to happen

With all such investments there will be winners and losers, and for this to happen careful consideration needs to be given as to how costs and benefits are partitioned.

Mainland generation would necessarily suffer. How and where will depend on how the costs of emissions are factored into our power generation sector. At carbon prices of around $20 per tonne we have seen that Tasmanian generation effectively displaces Latrobe Valley generation. But with no price, as we now have, it is more likely to be black coal or gas that is displaced.

While it maybe in the short-term interests of Victorian consumers to maximise low cost power provided by the Latrobe Valley generators, they should be alert to their exposure should the world move to a more determined action on carbon emissions. With an emission rate of 1.2 tonnes CO2 per megawatt hour of electricity produced, the Victorian economy is more exposed than just about any in the developed world. Replacing its most emissions intensive power generation with 500 megawatts of zero emission energy sourced via Basslink would reduce Victorian electricity sector emissions by 7 million tonnes over the year, or by about 12%, and go some way to alleviating this exposure.

Notes

[1] Across the first 8 months of FY2014-15 demand has continued to decline across the NEM, albeit at a slower rate than the previous years. The exception is Victoria where the drop in demand has accelerated due in part to the closure of the Point Henry aluminium refinery and in part to the cooler summer, compared to recent years. The close of Point Henry has literally seen the bottom fall out of the market, as illustrated by the daily demand curve in the figure below.

Despite the falling demand in Victoria, output from the Victoria’s Latrobe Valley brown coal generators has increased, primarily to fill the gap left by reduced hydro output.

In consequence, output from the Latrobe Valley is on track to exceed Victorian demand over FY 2014-15 by about 200-250 megawatts.

[2] The figures below shows (1) the total hydro production on the NEM (black), the Tasmanian hydro output (red) the mainland hydro (blue) and, (2) the wind output on the NEM since 2011. Tasmanian hydro constitutes about 2/3 of the total, and about 40% of total renewable energy dispatched since 2011.