The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set. Timo Henckel is the non-voting chair of the Board.

In Greece the economic tragedy appears to be in its final act, while dramatic falls in the Chinese stock market highlight the weaknesses of its economy. Domestic economic data is mixed: unemployment has fallen slightly but consumer and producer confidence have weakened. Inflation remains comfortably within the RBA’s target band.

The CAMA RBA Shadow Board on balance prefers to hold firm. While it attaches only a small probability to the need for a rate cut, this probability has increased from the previous month. In particular, the Shadow Board recommends the cash rate be held at its current level of 2%; it attaches a 57% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 8%, up from 2% in the previous month, while the confidence in a required rate hike stands at 35%.

Australia’s jobless rate, according to the Australian Bureau of Statistics, fell to 6% in May. Encouragingly, in the same month full-time employment and total employment have increased significantly while the participation rate is virtually unchanged. No new data has been released on wage growth, which recently has been at a record low of 2.3% per quarter.

The Aussie dollar keeps hovering around the 76 US¢ mark. Yields on Australian 10-year government bonds have continued to rise, now equalling 3.02%, implying a further steepening of the yield curve, normally an indication that the economy is improving.

The S&P/ASX 200 stock market index has retreated from its all-time high in April, taking some of the froth out of the market. High real estate prices, which carry the risk of misallocated investment and a costly price correction, remain a concern for many Shadow Board members and are often cited for a reason not to cut the cash rate any further.

Overseas, the Greek debt crisis and the faltering Chinese economy give cause for concern. While Australia’s direct exposure to the Greek economy is minimal, a complete breakdown of negotiations between Greece and the European Union, followed by a Greek exit from the Euro, may have noticeable ramifications for global financial markets.

Of greater concern is China, Australia’s largest trading partner, which grew by only 7% in the first quarter of this year, its weakest performance in six years. Some analysts, taking into account the recent tumble of the Chinese stock market and weak gauges of factory activity, entertain the possibility of a further slowing of the Chinese economy. Meanwhile, the US economy is looking more promising, but continued turmoil in the international economy will likely delay the long-awaited increase of the federal funds rate by the Federal Reserve Bank. Commodity prices are likely to remain soft and possibly fall further.

Consumer and producer confidence remain volatile and moderately weak. The AIG Manufacturing Index decreased from 52.29 in May 2015 to 44.20 in June, while the Westpac/Melbourne Institute Consumer Sentiment Index fell from 102.40 in May 2015 to 95.30 in June. The AIG Services Index increased slightly from 49.60 in May 2015 to 51.20 in June. These sentiment numbers are reflected in weak capital expenditure and weak consumer spending.

What the Shadow Board believes

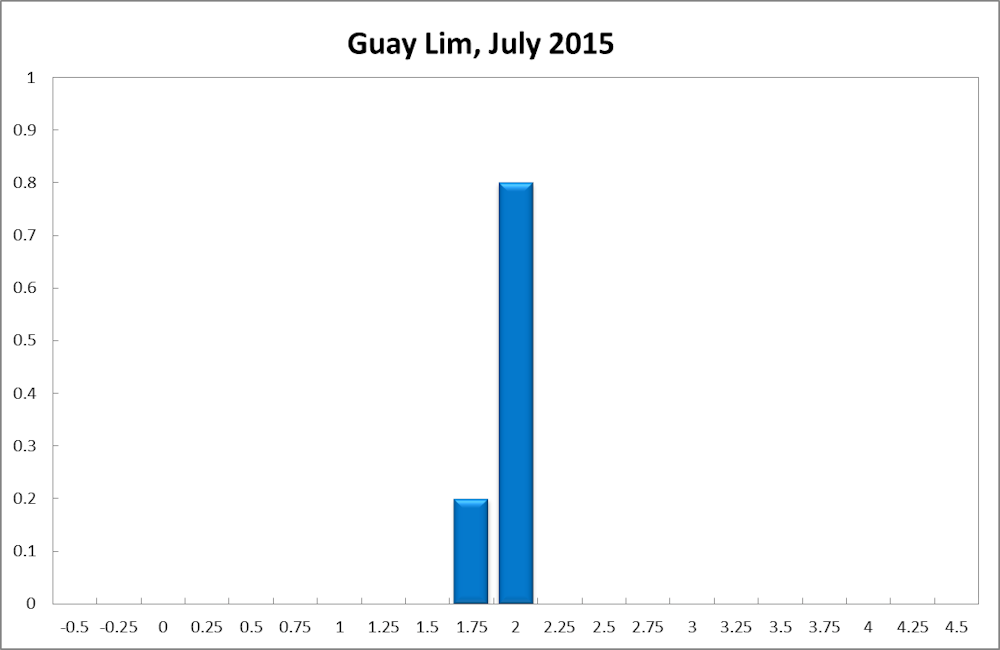

The Shadow Board’s confidence that the cash rate should remain at its current level of 2% equals 57% (down from 60% in June). The confidence that a rate cut is appropriate has increased from 2% in June to 8%; conversely, the confidence that a rate increase, to 2.25% or higher, is called for has decreased from 38% in June to 35%.

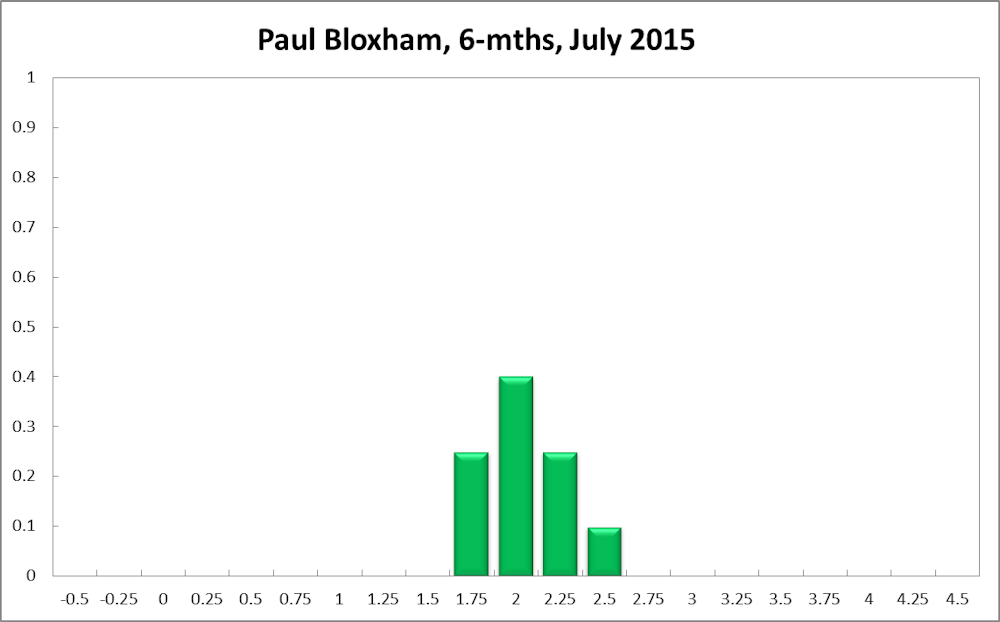

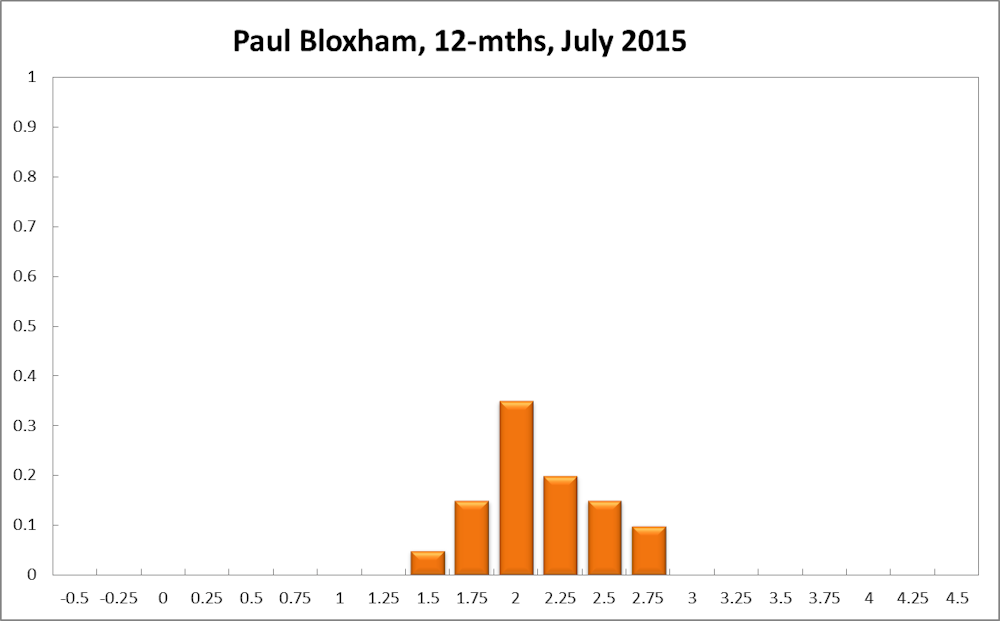

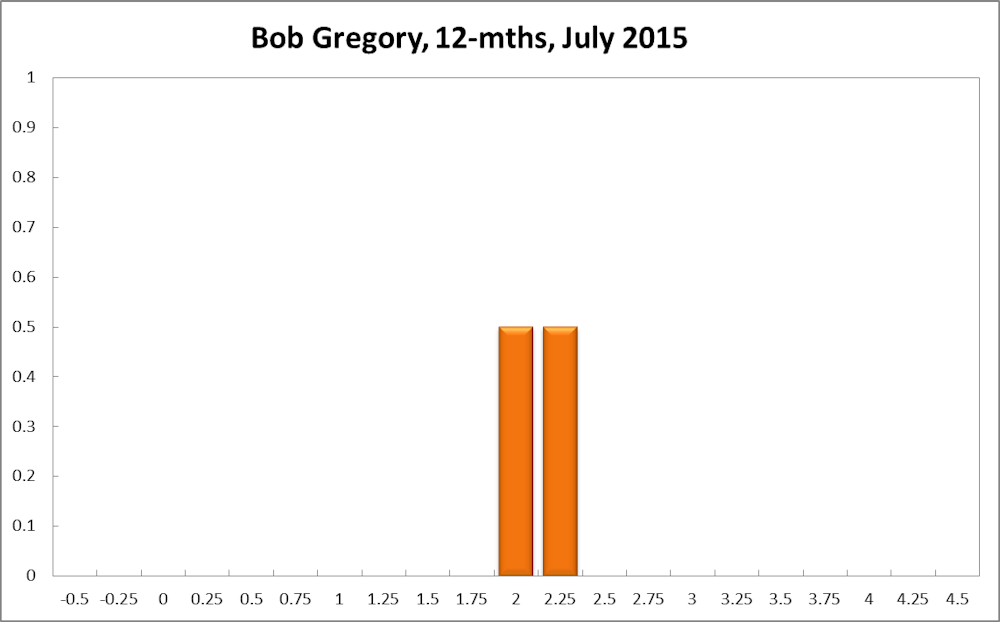

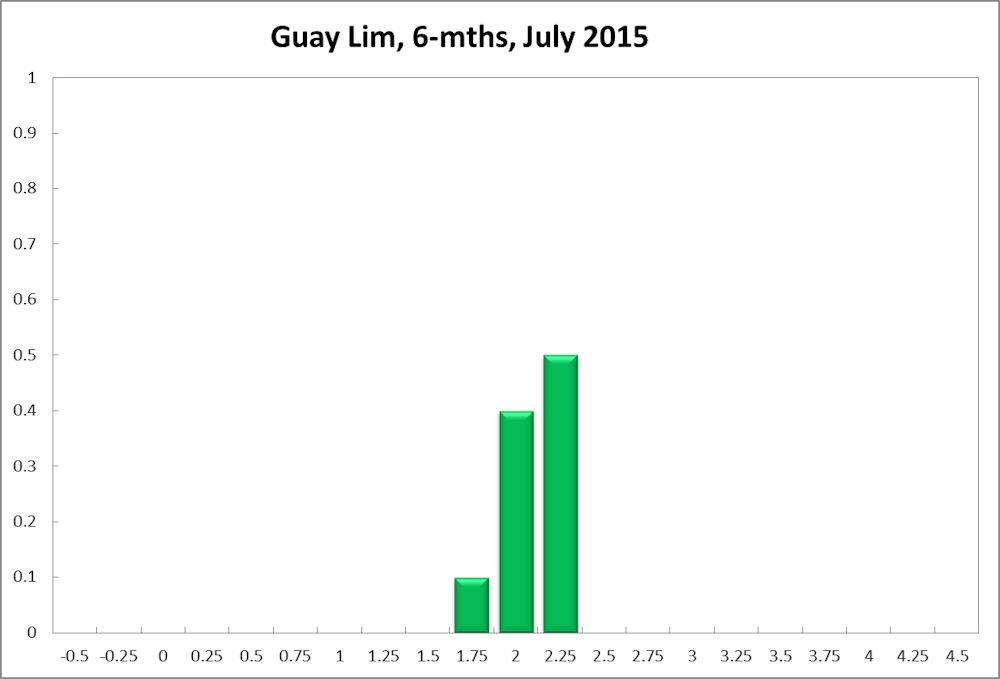

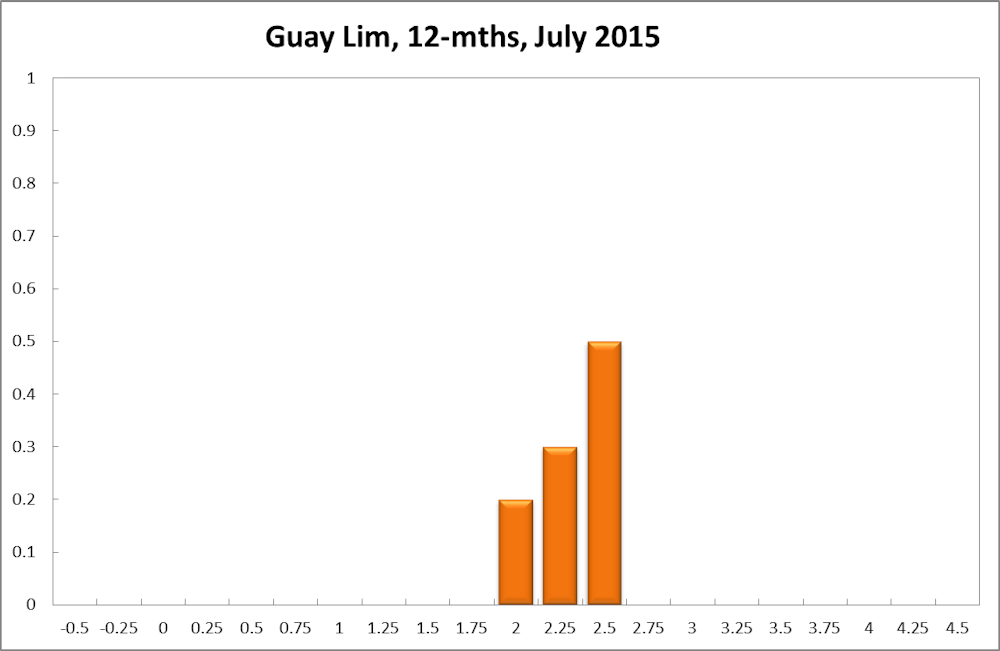

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2% equals 24% (23% in June). The estimated need for an interest rate increase lies at 69% (76% in June), while the need for a rate decrease is estimated at 6% (3% in June). A year out, the Shadow Board members’ confidence in a required cash rate increase equals 77% (down from 81% in June), in a required cash rate decrease 4% (2% in June) and in a required hold of the cash rate 19% (up from 17% in June).

Comments from Shadow Reserve bank members

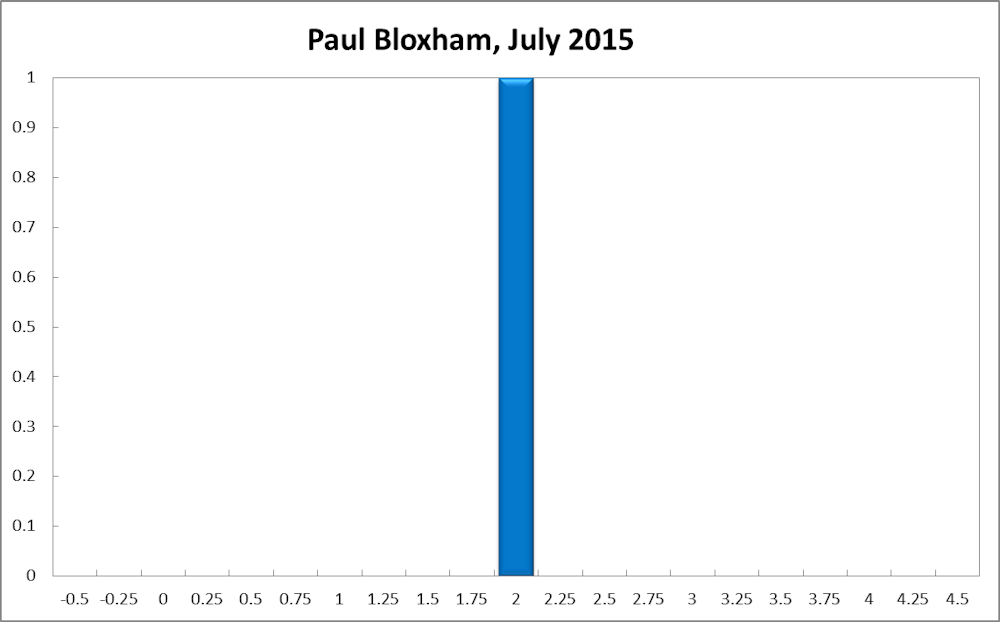

Paul Bloxham, Professor of Economics at Australian National University:

Having delivered 50bp of cuts in the first half there is no need to consider cutting rates again this month, particularly given recent signs that the labour market is improving. At the same time, activity in the Sydney and Melbourne housing markets continues apace, with the Sydney market, in particular, showing signs of worrisome exuberance. Although a lower AUD could help to speed up the re-balancing of growth, it is not clear that the domestic cash rate setting is having much influence on the currency. What is clear, is that further rate cuts risk over-inflating the housing market. In my view, the costs associated with cutting the cash rate further outweigh the benefits that lower rates could deliver in terms of supporting sustainable growth.

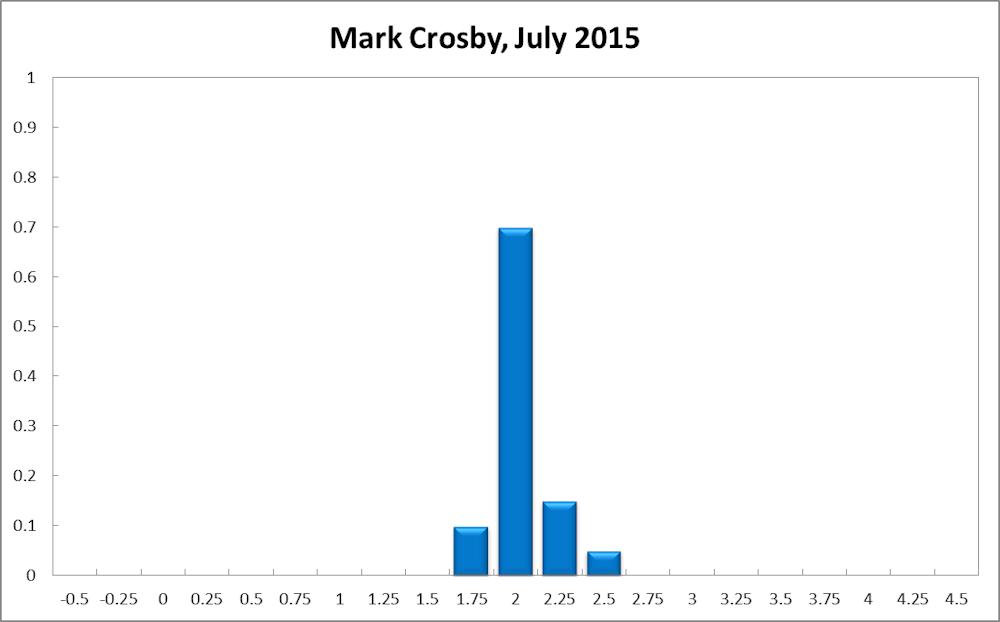

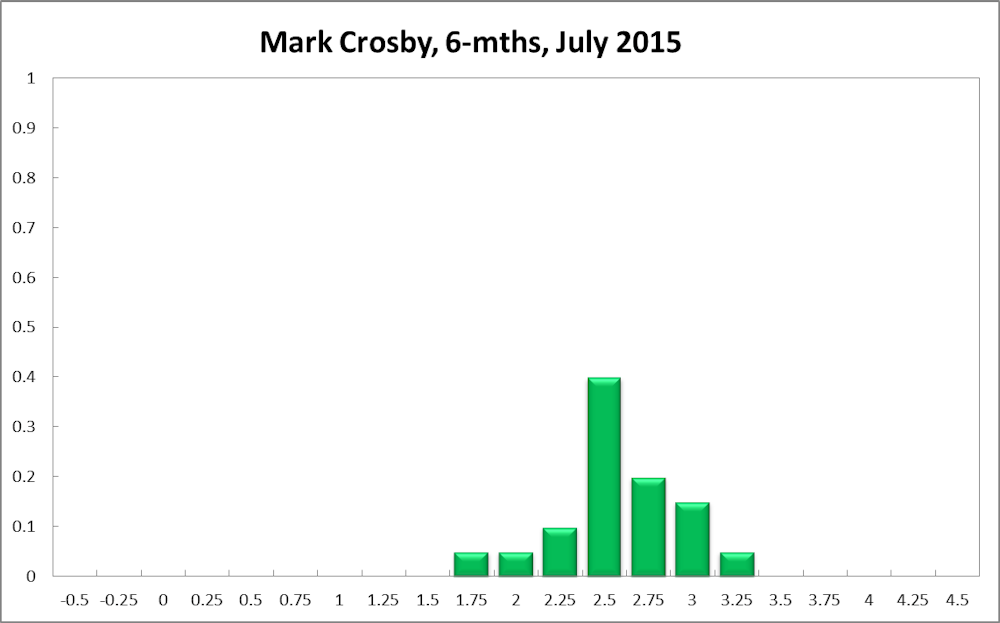

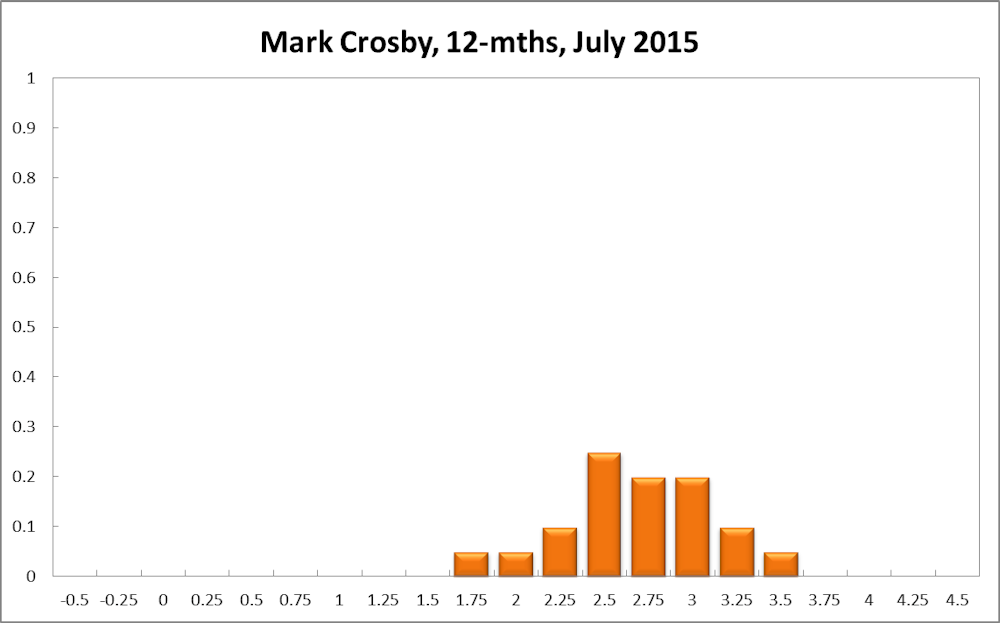

Mark Crosby, Associate Professor, Melbourne Business School:

“If there is Grexit…the RBA might reasonably cut to calm nerves.”

In this case more than ever events in the rest of the world right up until the Board makes its decision are likely to influence the outcome. If there is Grexit then the likely ramifications for European and global economies are small, but we really can’t know. If that were to occur then the RBA might reasonably cut to calm nerves. However in the more likely event that the Europeans kick the can down the road again, sitting on their hands seems the optimal decision to make.

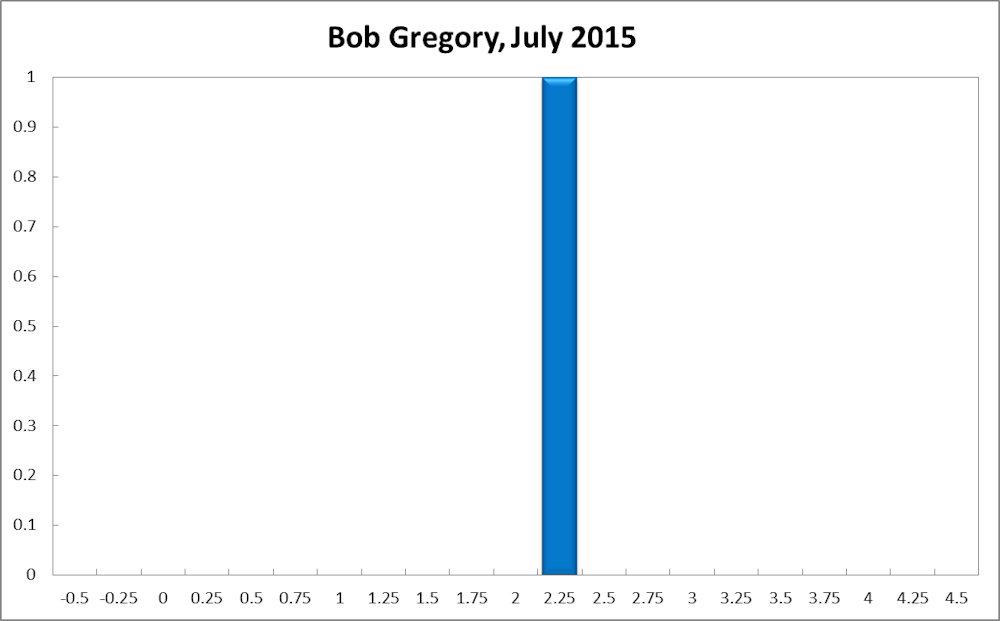

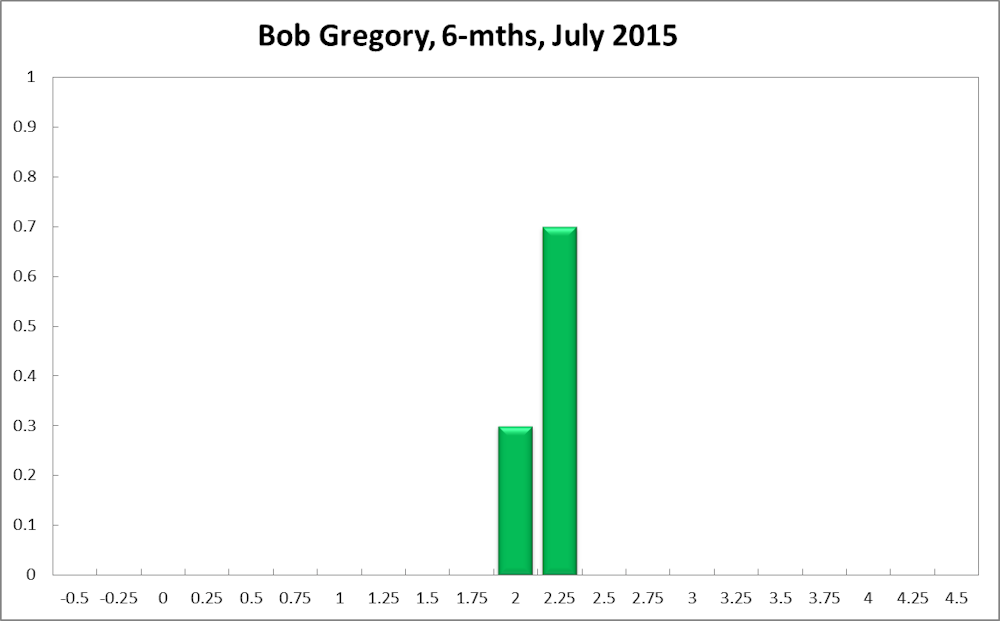

Bob Gregory, Professor of Economics at Australian National University:

I am really of the view that what we gain from lower interest rates is not worth the loss in increasing house prices.

Guay Lim, Professorial Fellow, Deputy Director, Melbourne Institute:

“Consumers remain worried about future conditions.”

There are signs that the economy is doing ‘alright’ – GDP growth was a strong 0.9 per cent in the March quarter of 2015, the trimmed mean measure of inflation was 2.3 per cent (2014:Q1-2015:Q1) and the unemployment rate dropped to 6.0 per cent in May 2015 (from a revised 6.1 percent in April). Unfortunately, there is no convincing evidence of momentum from forward-looking indicators. Neither the Westpac-MI Leading Index of Activity nor the Index of Unemployment Expectations are signaling steady improvements in activity. Consumers remain worried about future conditions; specifically, the Expectations component of the consumer sentiment index has been below the neutral mark of 100 since December 2013. On balance, it seems prudent to keep the cash rate steady for a while. This is especially important, considering the possibility of global “uncertainty” impacting negatively on the Australian economy. In the absence of action from the fiscal arm of policy, we may need the monetary arm to act quickly and decisively.

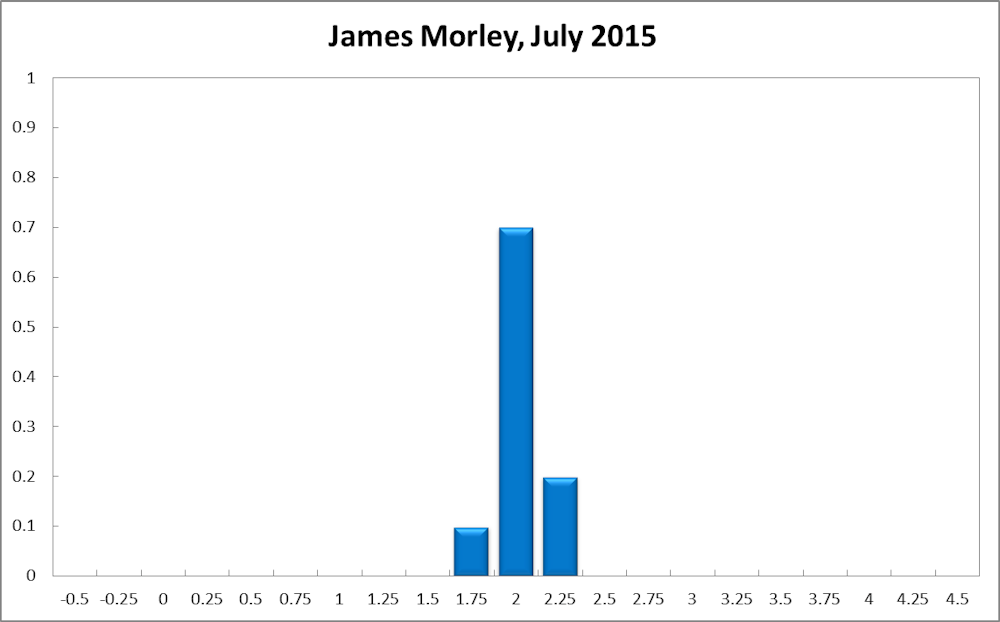

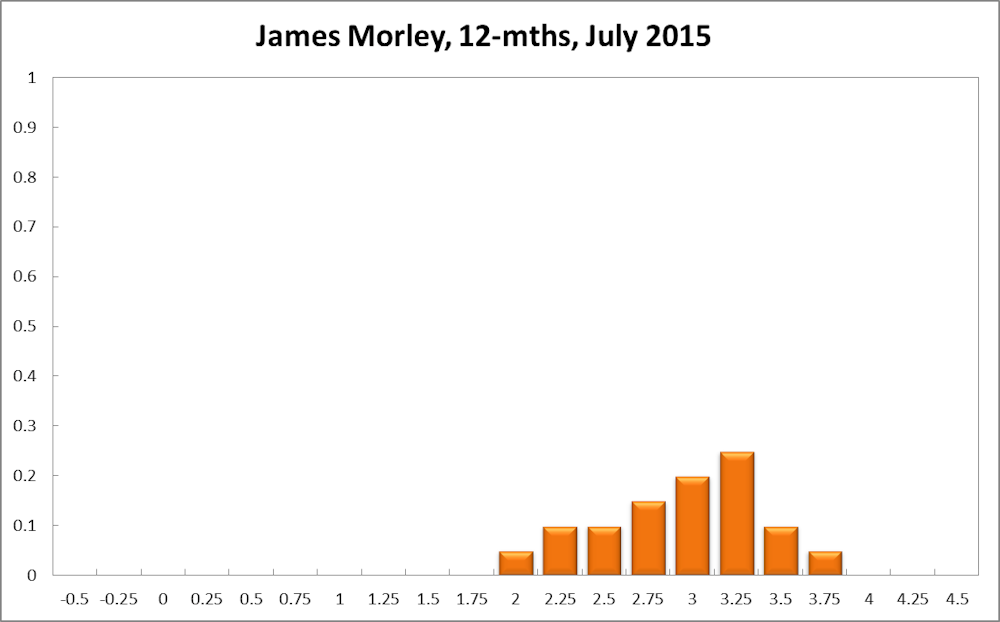

James Morley, Professor of Economics and Associate Dean (Research) at UNSW Australia Business School:

“Given the economic turmoil in Europe, this is definitely not the moment to start raising rates.”

With underlying inflation well within the RBA’s target range at 2.3 percent and the latest unemployment rate easing slightly down to 6.0 percent, the RBA should hold its policy rate steady, with a bias towards raising it in the future to return interest rates back to more neutral levels. Given the economic turmoil in Europe, this is definitely not the moment to start raising rates. It is true that Greece has little direct effect on Australia. But there are many implications for the position of other larger economies within the Eurozone if Greece were to exit. In any event, this turmoil could delay liftoff for the US interest rates, which will put upward pressure on the Australian dollar. Therefore, in the absence of domestic inflation pressures, the RBA should not raise rates until the European turmoil and the timing of liftoff for US interest rates is resolved.