The raising of the cap on tuition fees charged by universities in England to £9,000 per year in 2012 does not currently look like it will save the government much money – but it has led to a substantial increase in the funds universities receive to teach undergraduates. That is the finding of new research published by the Institute for Fiscal Studies, funded by Universities UK.

Universities in England receive income for teaching students from two main sources: teaching grants, which are paid by the government to universities based on the numbers of students taking certain subjects; and tuition fees, which are paid by students.

The government’s 2012 reforms to higher education funding in England scrapped teaching grants for all but the most expensive subjects and instead enabled universities to charge substantially higher tuition fees – raising the cap from £3,375 to £9,000 per year.

Many institutions have raised tuition fees to this limit: we estimate that around 60% of young English full-time undergraduates who started courses at universities in England in the first year of the new regime from 2012-13 paid tuition fees of £9,000 in their first year.

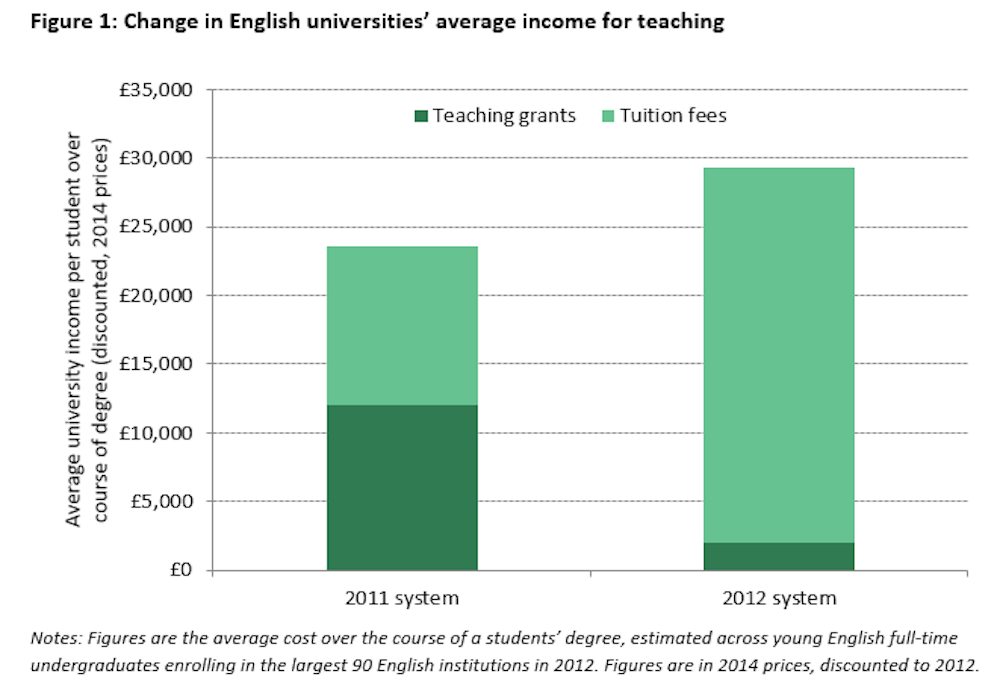

This increase in tuition fees more than outweighed the reduction in teaching grants, with universities set to receive an additional £6,000 per student, on average, over the course of their degree under the new system compared to the old system (which was in place up to 2011).

This is equivalent to an increase in funding of around 25% when taking into account both teaching grants and tuition fees.

While these reforms have certainly led to an increase in funding for universities, whether they have saved the government any money is far less certain. Students can borrow money from the government to cover their tuition and maintenance costs – and only have to repay these loans once their income is above £21,000 a year and for up to a maximum of 30 years.

This means the amount that will be repaid, and hence the overall cost of higher education, depends on how much graduates will earn over the next 30 years (amongst other things, such as the repayment behaviour of graduates).

Under our baseline assumptions, we’ve estimated that for each £1 loaned out to cover tuition and maintenance costs, the average long-run cost to the government will be 43p. This figure, expressed in percentage terms, is sometimes referred to as the Resource Accounting and Budgeting (RAB) charge, a term used to identify the government subsidy inherent in the student loan system.

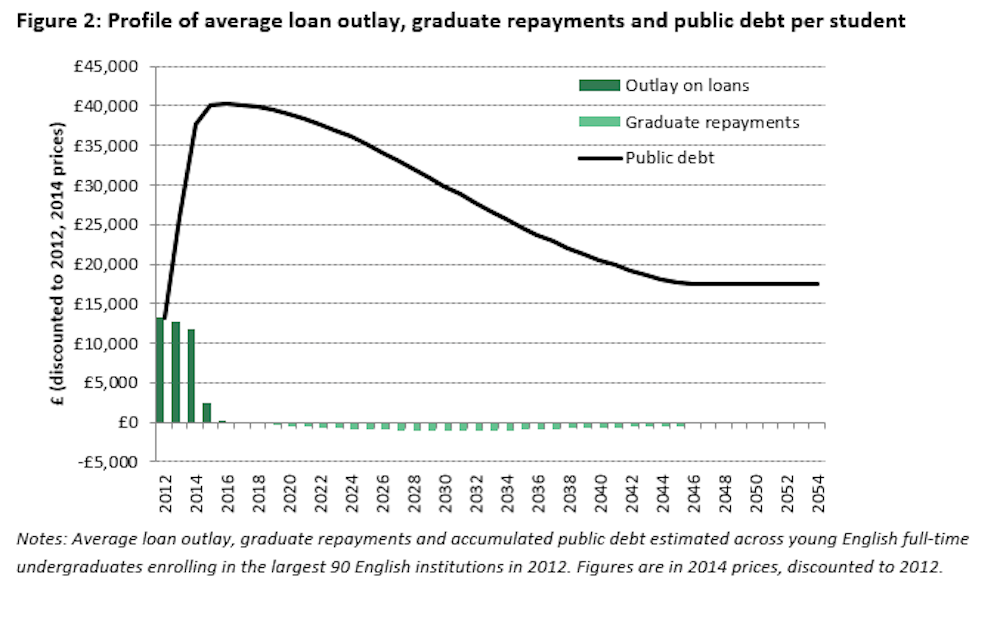

The average amount lent to each student is estimated to be just over £40,000 in today’s money, meaning that the average loan subsidy amounts to just over £17,000 per student.

The figure below shows that public debt initially rises as loans are made to students, to just over £40,000 per student, and then falls over time as repayments are made, reaching just over £17,000 at the end of the repayment period. This is equivalent to the average public subsidy on each loan made.

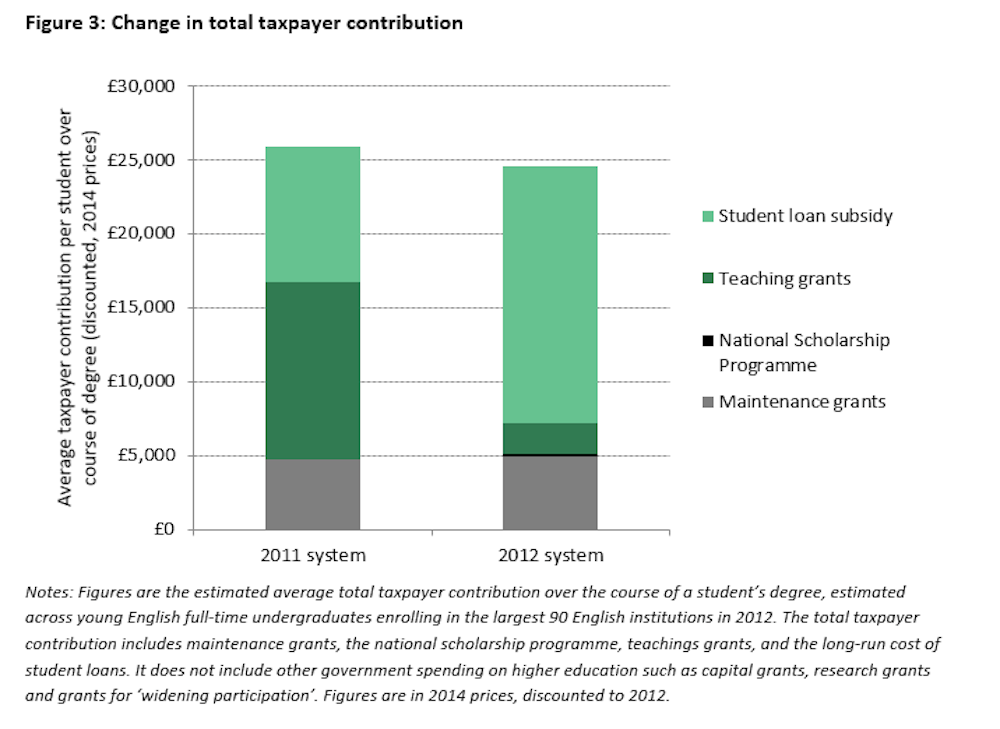

Adding in other sources of government spending on undergraduates, such as the remaining teaching grants and maintenance grants, increases the total taxpayer contribution per student to just over £24,500 in today’s money over the course of their degree.

Crucially, this is just 5% less (around £1,250 per student in 2014 prices) than we estimate it would have been under the old higher education finance system that was in place before 2012. Therefore our analysis suggests that the 2012 reforms currently look unlikely to save the government much money, as shown by Figure 3.

But these estimates are extremely sensitive to assumptions about what happens to graduates’ earnings over the next 30 years.

The baseline estimates assume that earnings grow in line with forecasts of earnings growth made by the independent Office for Budget Responsibility (OBR) in December 2013.

If earnings were instead to follow the more optimistic path forecast by the OBR in March 2012, the estimated average long-run cost to the government would fall to 34p per £1 issued, and the amount saved relative to the old system would increase from 5% to 15%.

The 2012 fee reforms have undoubtedly increased the resources available to universities to cover the cost of teaching undergraduates. What is less clear is whether they have also saved the government money.

This depends fundamentally on what happens to graduate earnings over the next 30 years, which the government can only estimate at this stage. The impact of the reforms on the public finances has therefore primarily been an increase in uncertainty, with the certain costs of providing teaching grants replaced by the highly uncertain costs associated with issuing larger student loans.

Hard Evidence is a series of articles in which academics use research evidence to tackle the trickiest public policy questions.