Is solar power the technology of the future? It is certainly the fastest-growing energy generation technology in the UK. By the early 2020s, according to a new report, it will be cost-competitive with gas and coal power. If so, the goal of having unsubsidised renewable energy is in sight.

The report, by Berlin-based think tank Thema1, concludes that this is possible without radical technology improvements or similar step changes. This somewhat disagrees with similar studies, which tend to point to the next big thing as being just around the corner.

Bright hopes

There are lots of exciting developments in the laboratories but to make a real difference they need time – more than the 10-year time frame in Thema1’s forecasts, so their report is right not to factor them in. The majority of new technologies focus on the photovoltaic (PV) module itself, promising higher power output per unit (by using graphene or nanotechnologies) or much reduced production costs (using novel materials like organic solar cells).

Higher rates of converting light into electricity (“efficiencies”) are always welcome in new PV devices, but their viability depends on the production costs. It is possible today to produce cells that can convert up to 46% of the sun’s power into electricity, but costs render these commercially unfeasible. The incumbent technology, wafer-based silicon PV modules, converts about 22% of sunlight at a fraction of the cost.

On the other hand, there is a lot of excitement around technologies such as organic solar cells that are less efficient but have much reduced costs. But this approach tends to shift the balance of costs from the module to the other system components such as mounting structures and can make the system more expensive. To be commercially viable, these devices need a minimum efficiency of about 10%-12%. This recently led to the demise of virtually all thin-film silicon manufacturers, for example, which struggled to get the double-digit efficiencies in cost-effective production times.

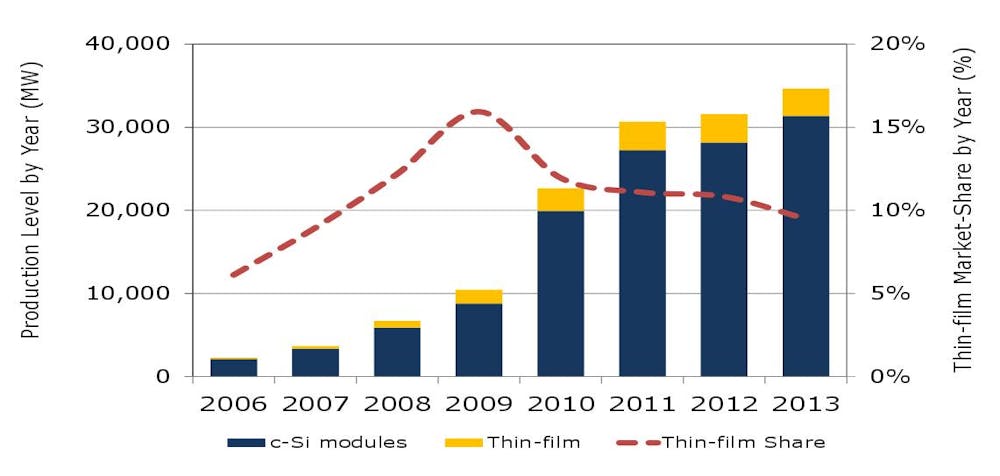

Market shares of regular and thin-film PV

The reality is that the road from laboratory cell to a full-size module is surprisingly difficult and slow. This can be seen when looking at current polysilicon thin-film technologies and how long it took them to come to their current competitive position. There is no reason to believe that other technologies will be much luckier.

Tech-free advances

Having said this, the Thema1 report is right to say that PV can achieve the costs required to survive without subsidies without any step change in technology. All it needs is the political will. If governments offer sufficient subsidies in the short term, solar will cut costs just by doing things better. This was the underlying idea of solar subsidies all around the world in recent years. Yet Thema1 suggests that all we now need to do is incrementally reduce these subsidies and by 2020 will have learned how to do things at the market price. This is not completely impossible, but there are some major caveats.

The reductions to UK subsidies of recent years are in fact one of the biggest issues in the industry at present. There were step cuts in funding that incentivised developers to rush through solar projects before cut-off dates, which resulted in installation gluts. This has been detrimental for the quality of installations, resulting in higher operation and maintenance costs and thus higher energy costs.

Governments might argue that subsidy reduction has happened each year and is therefore foreseeable, However, this ignores the fact that these “cliffs” result in a rushed building phase to meet the deadlines. Reductions typically occur in April. This means most building happens in the first quarter of the year, when the weather affects ground conditions and can drive up costs. Changing this hard funding cliff to a softer decline and shifting the timing to later in the year may actually make a noticeable difference in system costs.

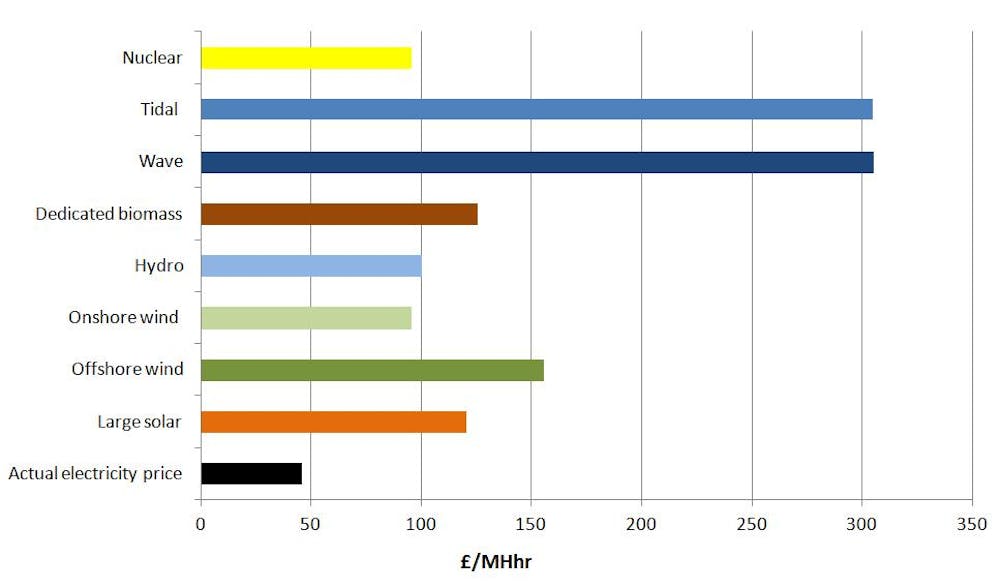

UK renewables subsidies 2014/15

The cost of connections is another major issue in the UK, especially with larger developments. The connection cost is sometimes nearly as expensive as the system itself – clearly rendering the investment impossible. This may be down to weaknesses in the grid and should be addressed on a national scale. All new technologies for producing electricity have required major grid investment, so saying such moves are too expensive for solar is a bit of a smoke screen.

An answer to intermittency

The most mentioned solution to making solar more competitive is to make it possible to store the electricity to get around the problem that the amount of solar energy varies during days and seasons. But this is potentially not required in the medium term. One reason is that people make the mistake of looking at technologies in isolation. There have been studies in Germany that indicate that this variability can be offset by using wind and solar together, for example. One would need to look at the combinations for the UK to see if this is true in this country as well.

It is also worth pointing out that subsidies are paid to renewable electricity irrespective of the time of generation. If they were somewhat redistributed to include a timing element, it could be a way of cutting the price of PV energy without improving the technology. You can also maximise the amount of generation by shifting the orientation of the panels.

In short, the factor that has the power to make or break solar power is the political support. Combine such changes with the fact that PV still does have amazing cost-saving potential through technological progress and you have a future that could still be very sunny indeed. It is no exaggeration to say that incentive-free solar really could be on the horizon.