Discrimination is a great taboo of our times, and yet one huge industry gets away with it every day. The insurance sector looks at us as risk with legs. It puts us into groups, and if we are in a group deemed riskier, we have to pay more. It’s even written into law. Anti-discrimination legislation usually includes exemptions for insurance pricing.

Behind this approach lies the fear of an economic phenomenon known as “adverse selection”. In insurance terms it refers to the idea that you are more likely to buy insurance if you think you are going to need it.

This happens when insurers are not allowed to discriminate and the cost of risk has to be spread among the entire group. It means that insurance becomes a better deal for higher-risk people. Further down the line, the conventional wisdom is that this leads to higher average prices and fewer people insured – a bad outcome for insurers and society.

But is that conventional wisdom faulty? Thus far it has justified the insurance industry’s ability to charge more to some people for the same product. That may not always be justified after all.

Loss coverage

To explore this phenomenon, let’s look at a simple example on an island with a population of 10 people (and a curiously well-developed insurance industry).

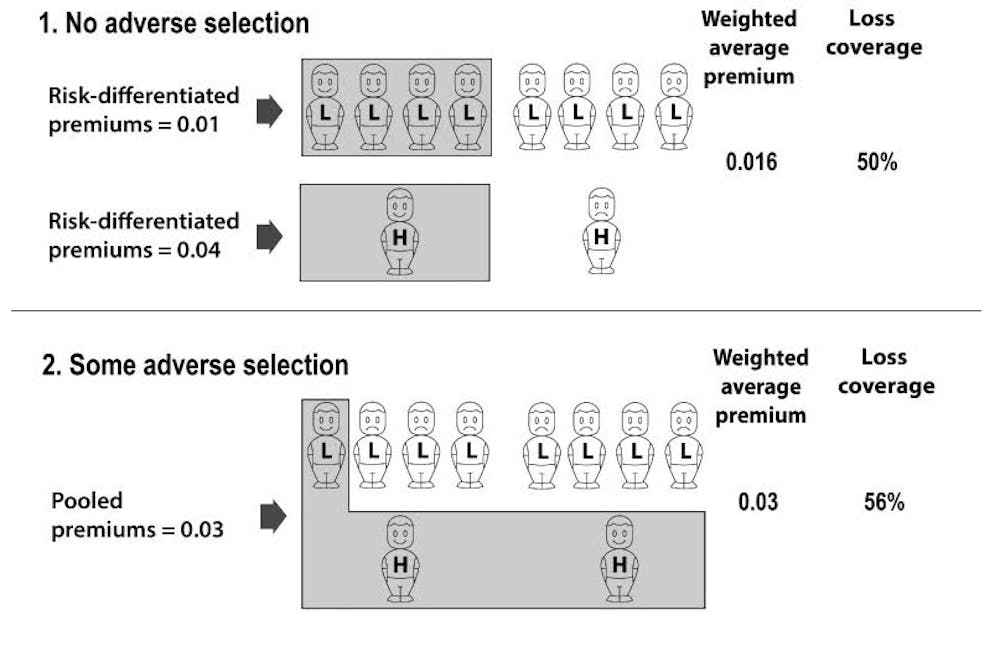

With no bar on discrimination at all, an insurance company would set prices which matched risk. And so if eight of our island residents were low-risk and two were high-risk (let’s say they are genetically predisposed to illness), the premiums charged to each group would reflect their expected claims.

Evidence suggests that under that system, about half in each group would buy the insurance. The mix of higher and lower risks among the insured is the same as in the population. This means there is no adverse selection. It also means that half the population’s losses are compensated by insurance. We can call this a loss coverage of 50%.

Now suppose our island’s curiously well-developed regulators stepped in to ban insurers from discriminating between higher and lower risks. Now they have to put all the islanders into one risk pool and charge the same premium to them all.

For insurers to break even, the pooled premium will need to be relatively expensive for the lower risks, leading fewer of them to buy – and it will be cheaper for the higher risks, leading more of them to buy. And so we have the dreaded adverse selection in play.

You can follow the pattern in the images below. Here, the different premiums are expressed as a figure between zero and one. On average, people in the second example are paying more for their insurance than before. And the number of people who buy is lower too (three, compared with five). These features – higher average price and lower numbers insured – are the classic features of adverse selection.

But wait. There is also a nice surprise. In the second example, with no discrimination but with consequent adverse selection, the loss coverage is now higher. That is, 56% of the island population’s expected losses are now compensated by insurance, compared with 50% before. The better outcome arises not despite adverse selection, but because of adverse selection.

Tweaking the rules

It’s not all plain sailing. If pooled premiums are set too high – so that lower risk people don’t bother with insurance at all – then adverse selection can be extreme and loss coverage plummets. But it seems from the above example that some limits on discrimination, leading to moderate adverse selection, can help. If we accept that the whole point of insurance is to compensate the population’s losses, then tweaking the rules of insurance to increase loss coverage seems a reasonable goal.

One way to do that is to make everyone buy insurance. That’s what we do for motorists, where the central goal is to protect other people and the need is the same for every driver. But what about life insurance?

Life insurance is very important for many people, but not for everyone. If you don’t have dependants, you probably don’t need life insurance – or perhaps your employer already provides it. Where individual needs vary so much, making everyone buy insurance doesn’t work well.

But if we leave people free to make their own choices, we can still tweak the rules to increase loss coverage. The key here is to allow only the level of discrimination in pricing which delivers the right amount of adverse selection.

The insurance industry complained noisily when the EU stopped companies from applying different prices for men and women. But in truth this probably makes insurance work better, and so might limiting some other traditional exemptions. At present, insurers get almost a free pass from age and disability discrimination laws, on the grounds that discriminatory pricing is necessary to stamp out adverse selection. But if some adverse selection makes insurance work better – as my argument suggests – then we need to look at the exemptions again.