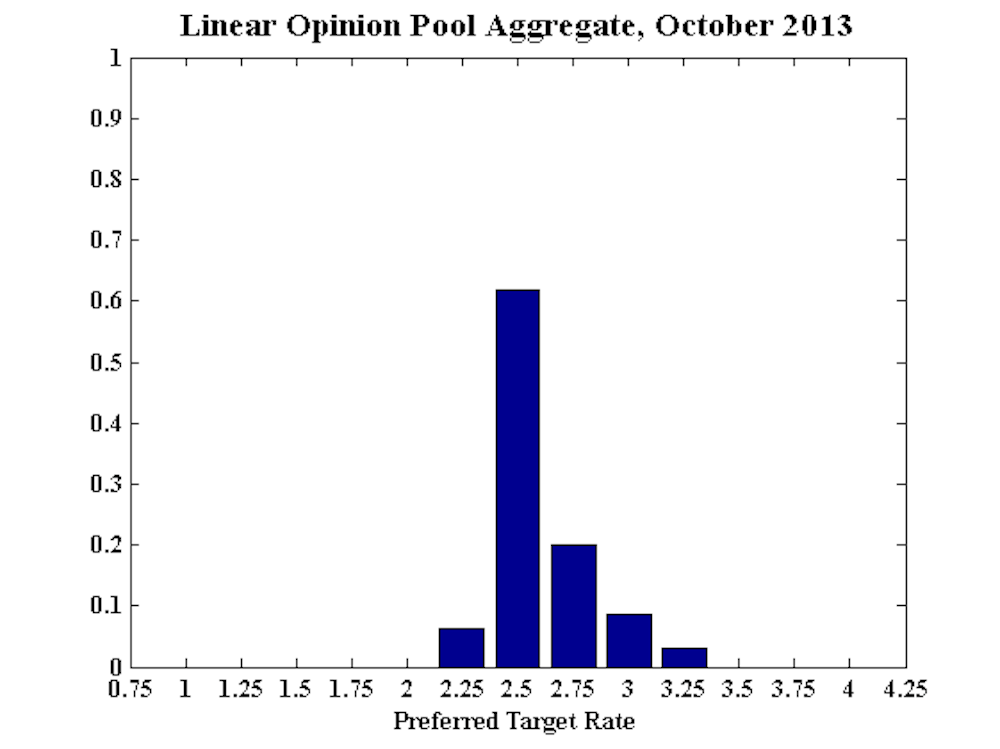

With uncertainty surrounding the recent federal election subsiding and positive economic news from abroad, several Shadow Board members worry that the Reserve Bank of Australia’s loose monetary stance may fuel a housing price bubble. The consensus is to keep the cash rate at its current level of 2.5% but at longer horizons there is a noticeable shift towards the need for higher rates.

The outlook for the US economy has improved slightly although the US Federal Reserve would like to see a stronger rebound and thus surprised the markets by delaying the tapering of its quantitative easing program, known as QE3.

Uncertainty surrounding the financial conditions of numerous Asian countries persists. In many economies public debt is at reasonable levels but private debt has soared during the past decade. At the same time countries invested heavily in US Treasuries (China, Japan and other Asian governments) will experience dramatic capital losses once the US starts to exit its quantitative easing program.

So far economic growth in the region has held up satisfactorily but there is increasing concern that the region’s economic growth is largely debt-fuelled and so the potential for another credit crunch in Asia remains.

For several members of the Shadow Board the main domestic concern lies with the frothy housing market. Rising prices and clearance rates in the major Australian cities are becoming disconnected from their flagging fundamentals. At this stage of the cycle, in which monetary policy is still very accommodative, the RBA would do well to signal to the markets that speculation in the housing market needs be contained.

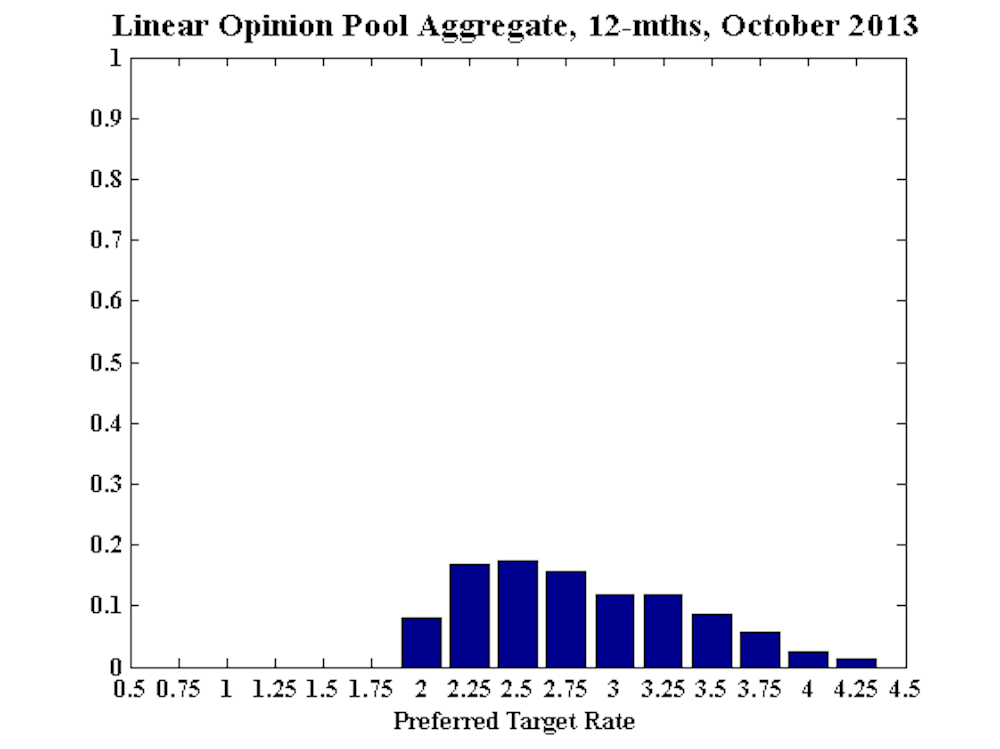

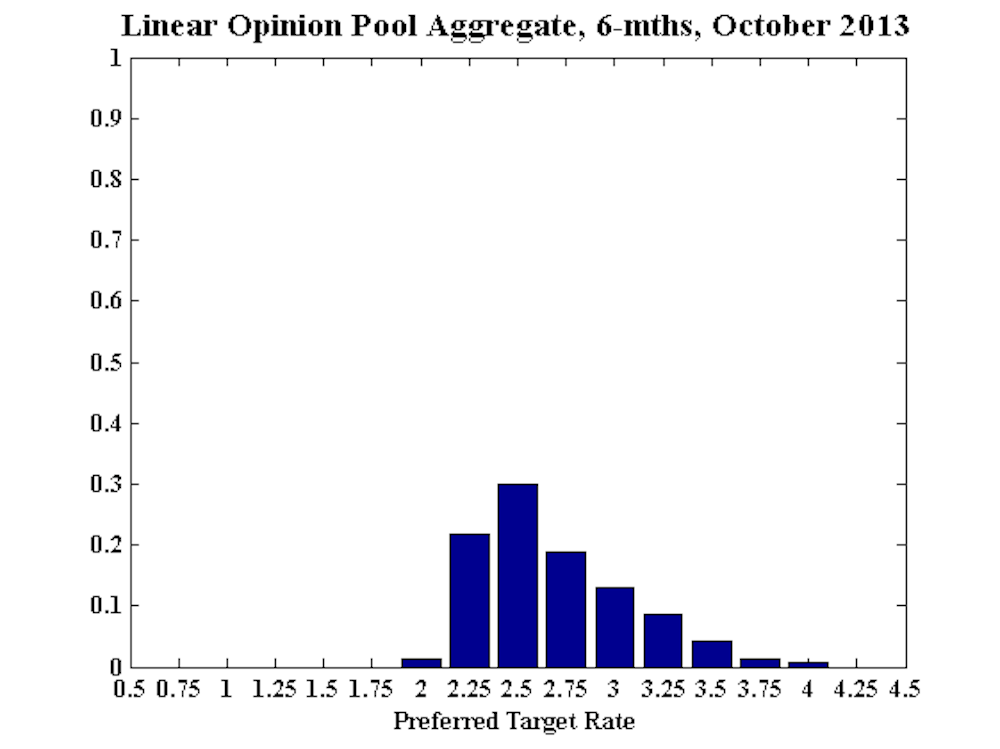

The Shadow Board’s confidence in keeping the cash rate unchanged has fallen slightly from 65% in September to 62%. The probability attached to the need for a further rate cut now lies at 6%, down from 13%, while a 32% probability is attached to the need for a higher current rate.

This shift towards higher interest rates is also reflected at longer horizons: the probability that rates will need to rise in the next six months has risen 6 percentage points to 47%, while the probability that rates ought to be lower than the current rate has fallen from 32% to 23%. A year out, the shadow board members attach a 58% probability to the need for an increase in the cash rate (up from 52% in September) and a 25% probability to the need for a decrease in the cash rate (down from 31% in September).

The Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

The project is designed to test and improve transparency of central bank deliberations by revealing the monthly opinions of individual members, emphasising the underlying macroeconomic uncertainties.

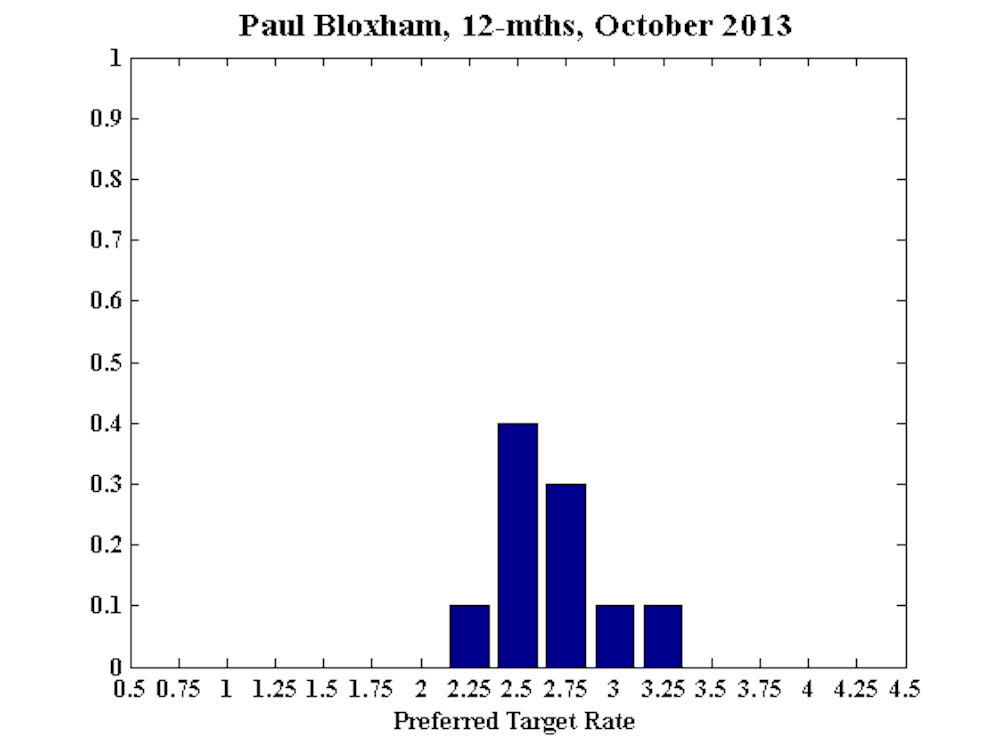

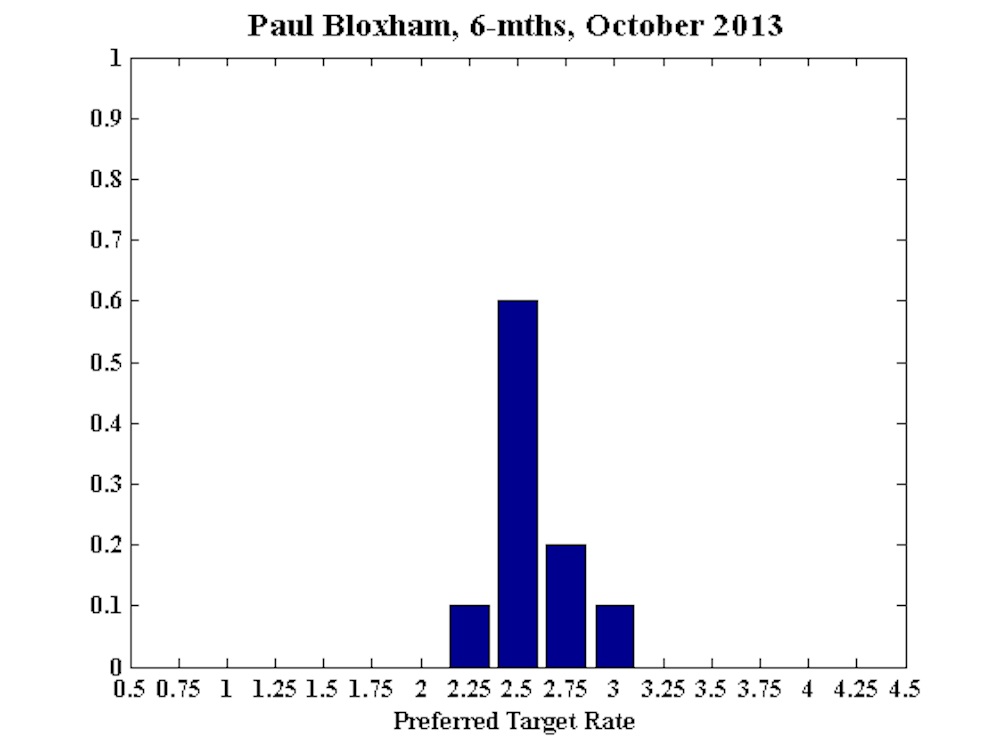

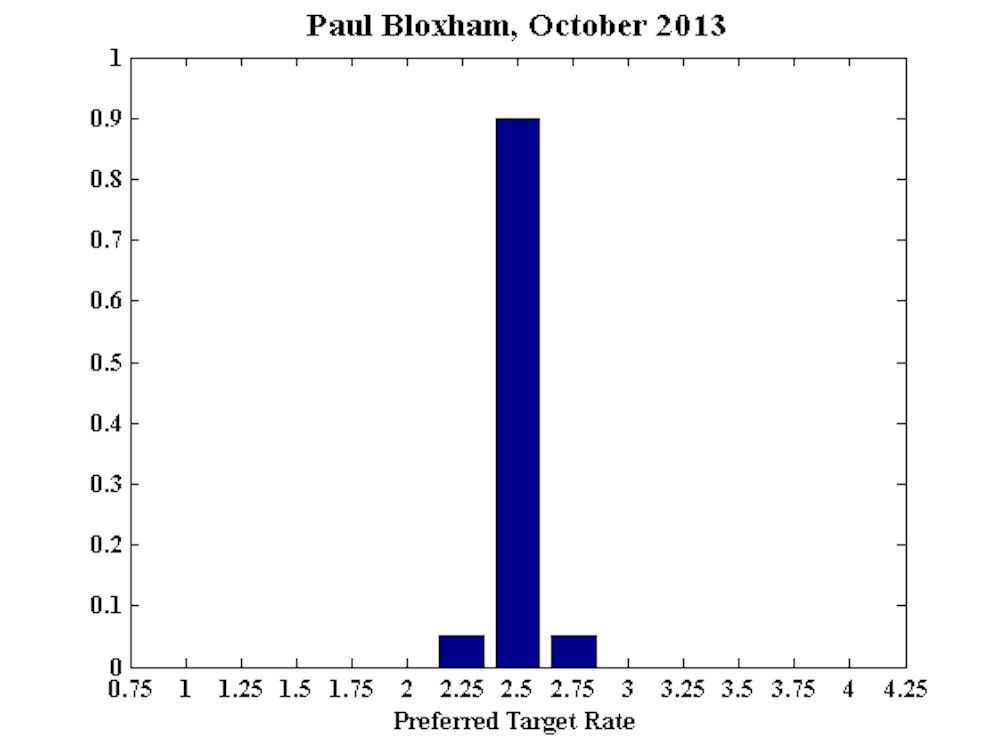

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

This month brought more signs that monetary policy is getting traction, with the local housing market continuing to lift and sentiment improving. There are also signs that growth in the Asian economies is picking up, led by Australia’s two largest trading partners, China and Japan. An improvement in conditions in Asia has also been part of the reason why the Australian dollar has risen in the past month.

While local growth remains below trend at the moment and inflation is near the lower bound of the target band, the risks to the growth and inflation outlook have shifted further to the upside in the past month. Rising housing prices and a pick up in new lending also mean that financial stability concerns should start to play a bigger role when considering whether the cash rate should be cut any further.

As I noted last month, cutting rates further from here may entail increased risks of asset price misalignments and while in the short run rising asset prices are likely to support growth, they may cause other problems in the medium term. Despite the recent rise in the Australian dollar, I recommend that the cash rate is left unchanged this month.

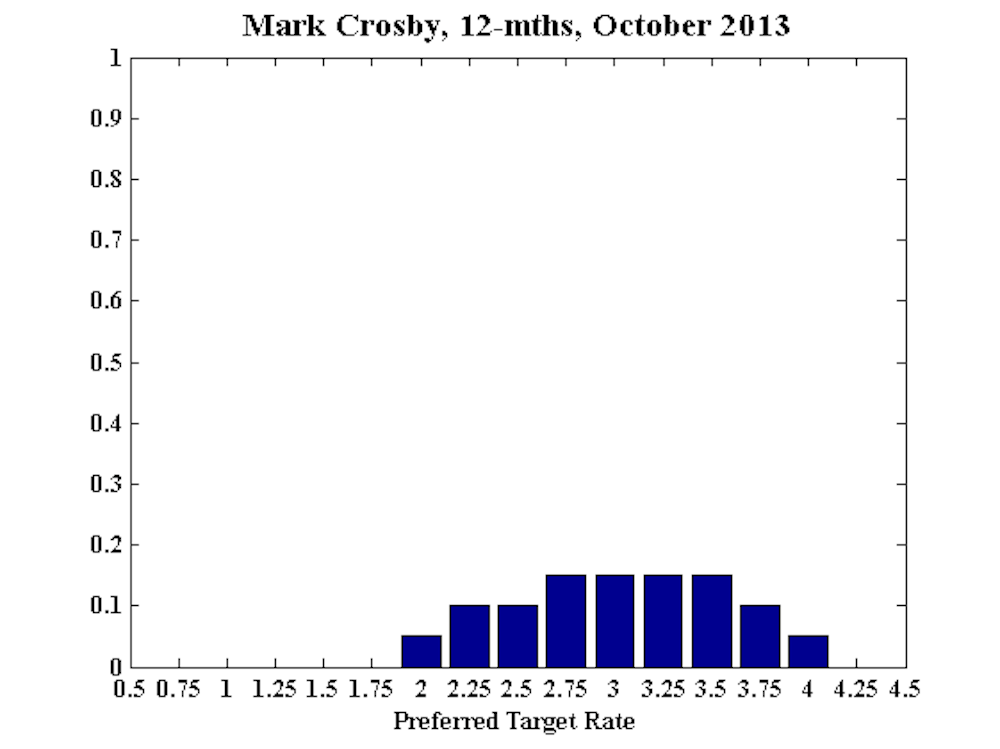

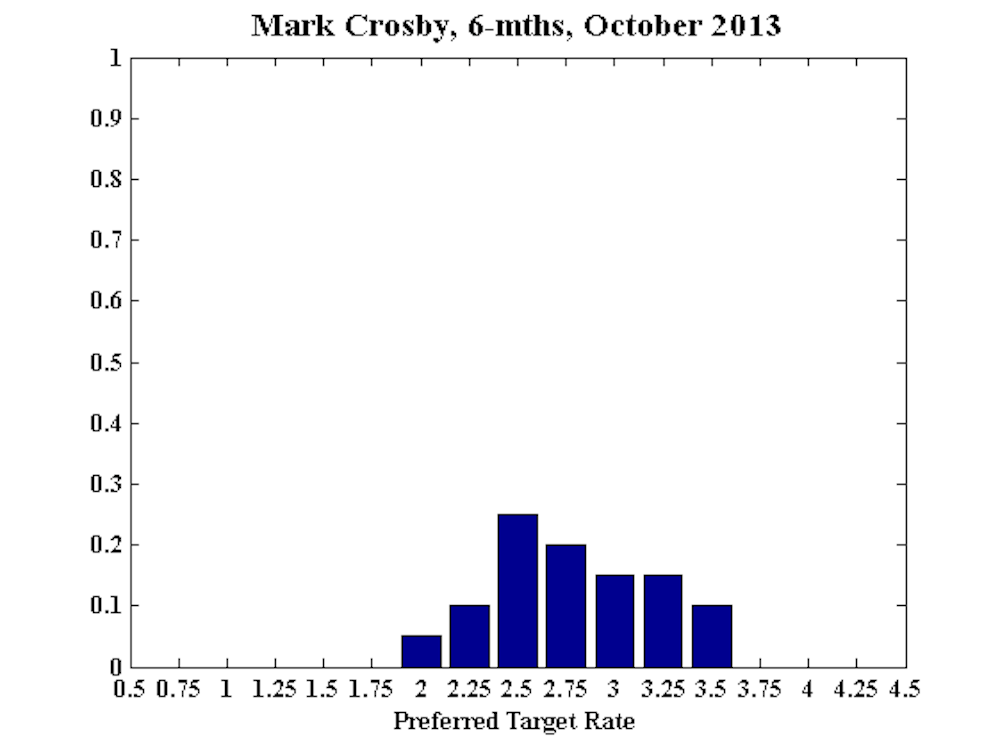

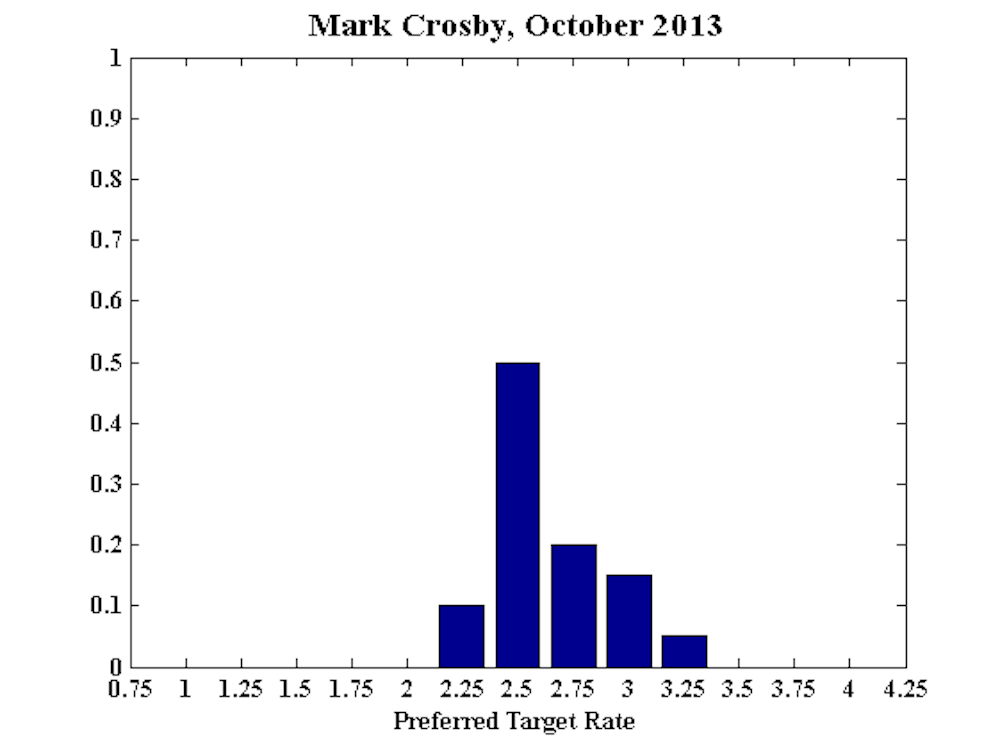

Mark Crosby, Associate Professor, Melbourne Business School:

Ongoing uncertainty is not helped by the US Federal Reserve’s decision not to taper (its quantitative easing program), though in general international conditions continue to surprise on the upside. It is surprising that the RBA is hosing down talk of a housing bubble when experience of the early 2000s suggests that the RBA can be wise to jawbone down the housing market, while Greenspan’s claims of “localised froth” proved to be folly.

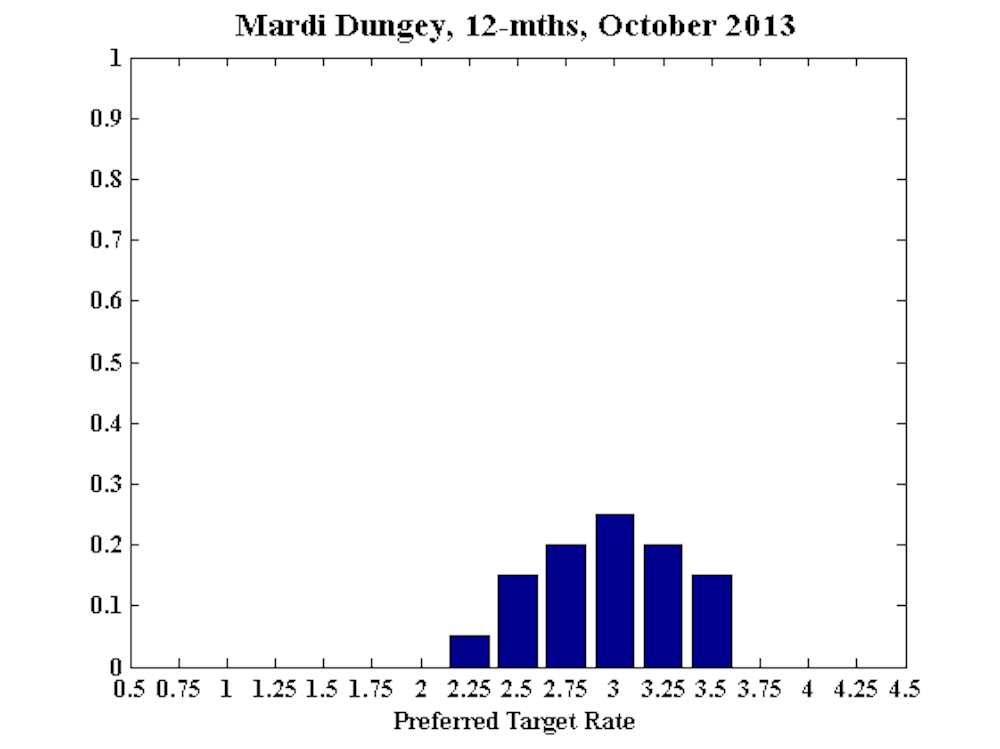

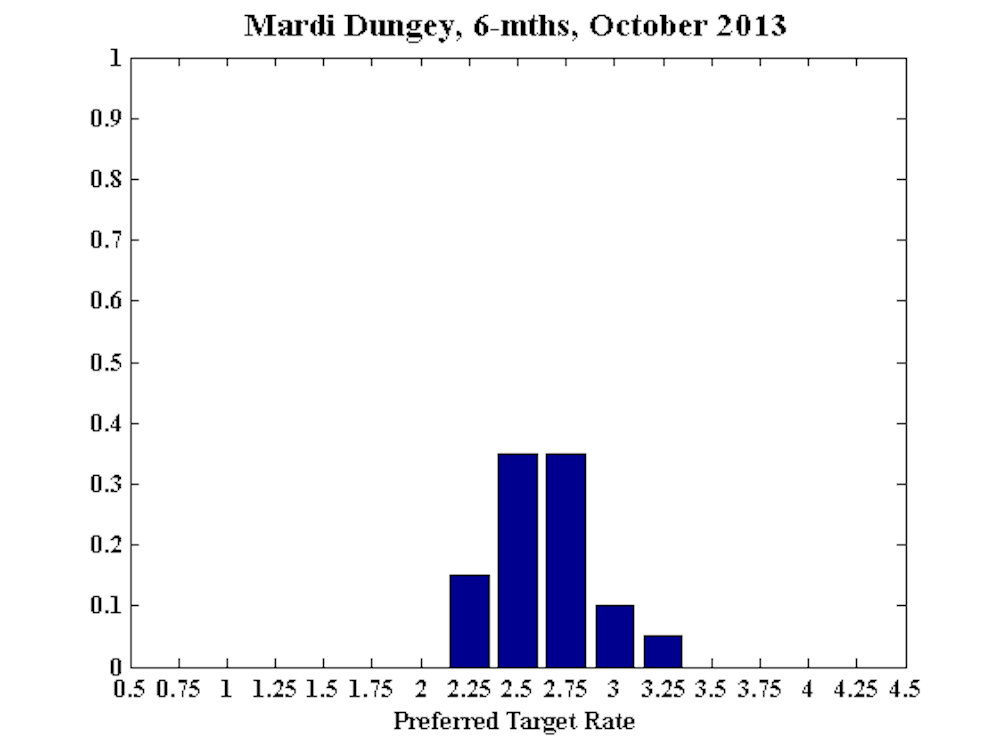

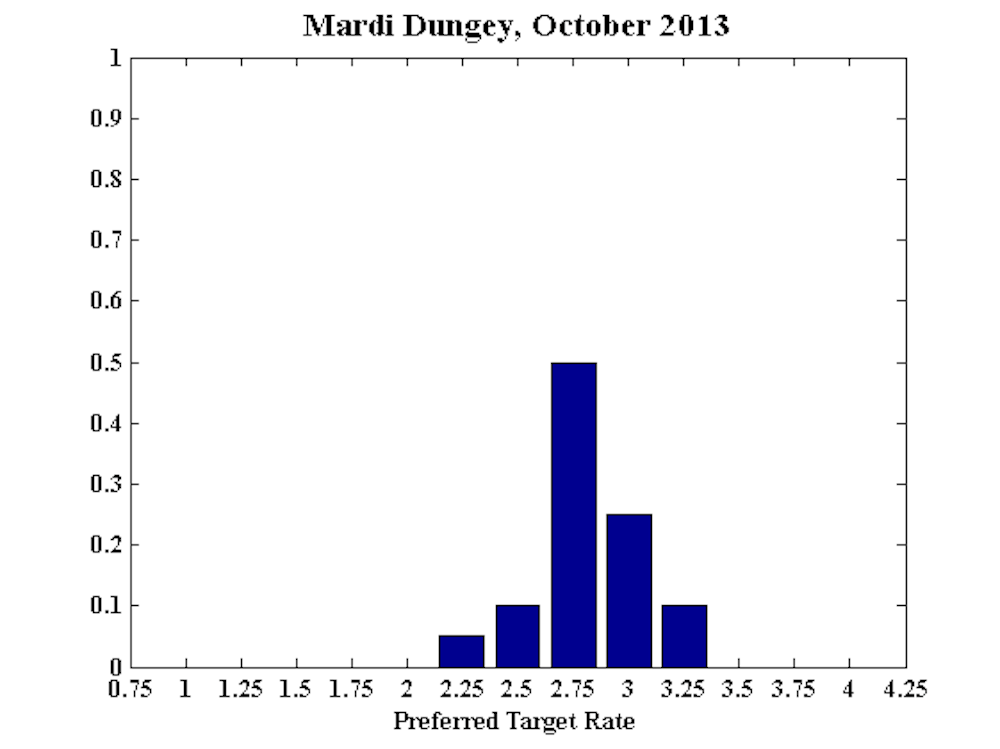

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA:

No comment.

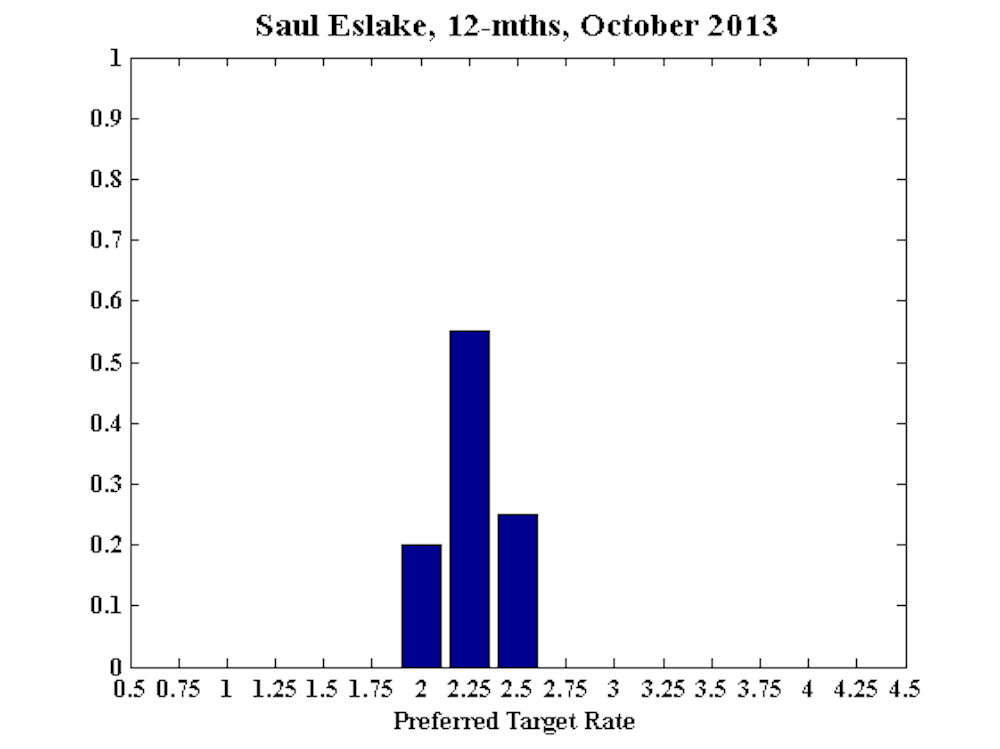

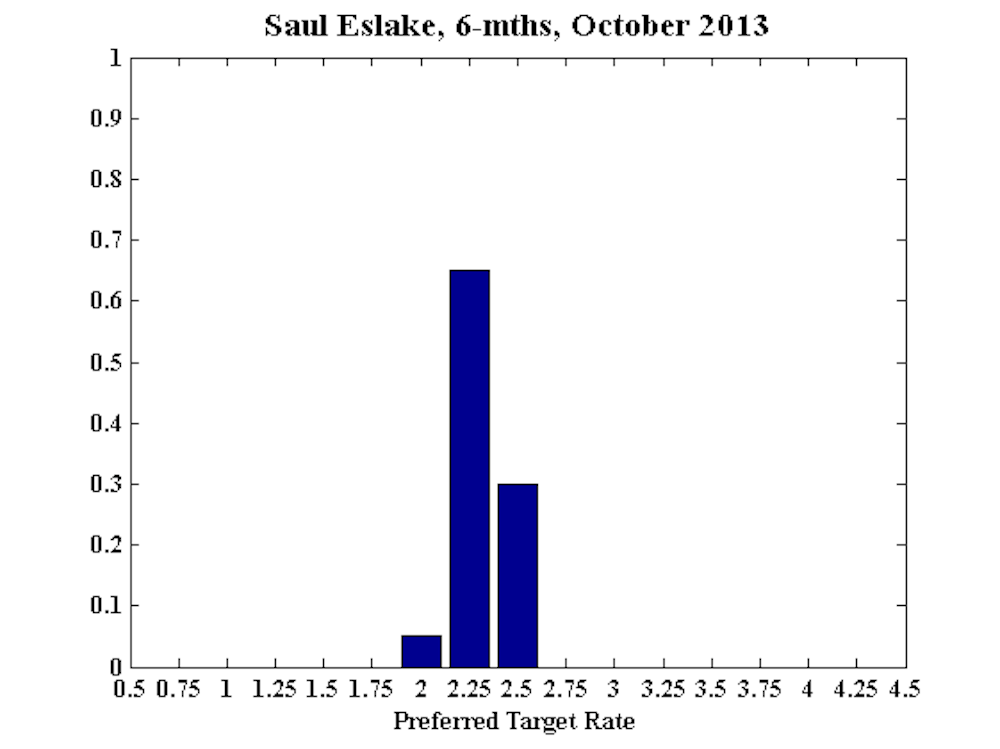

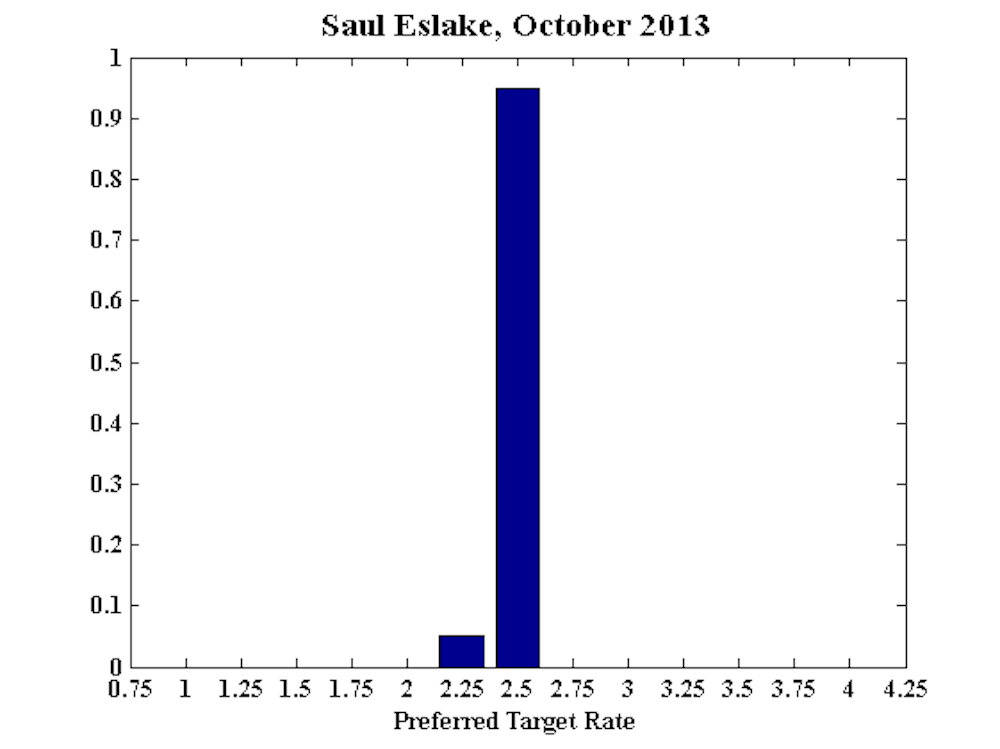

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

No comment.

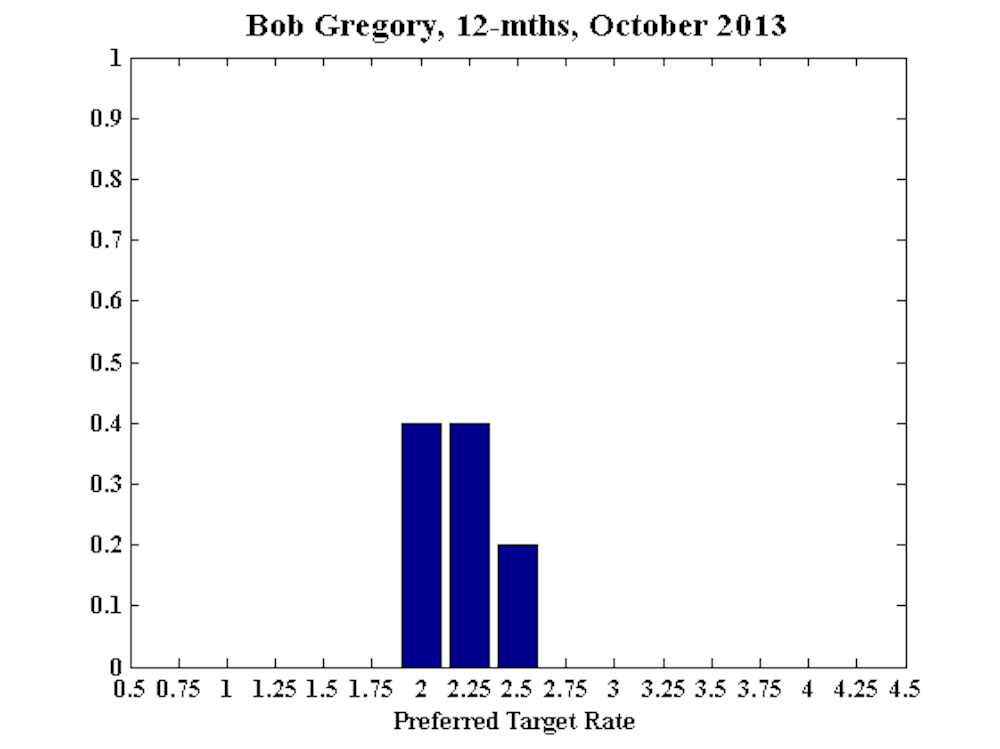

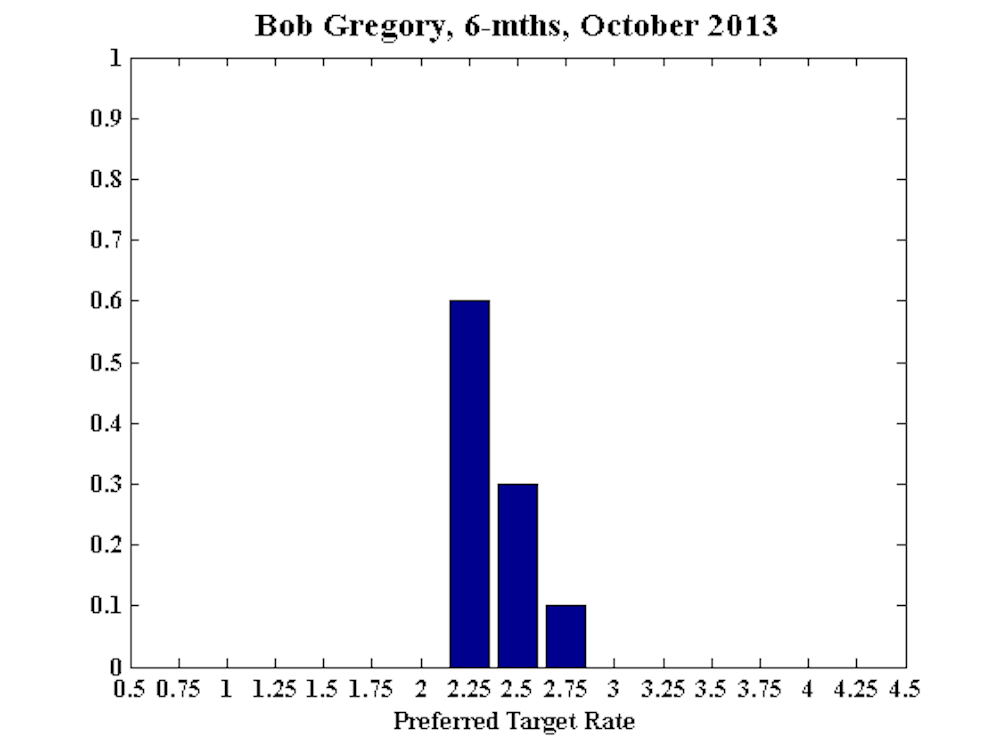

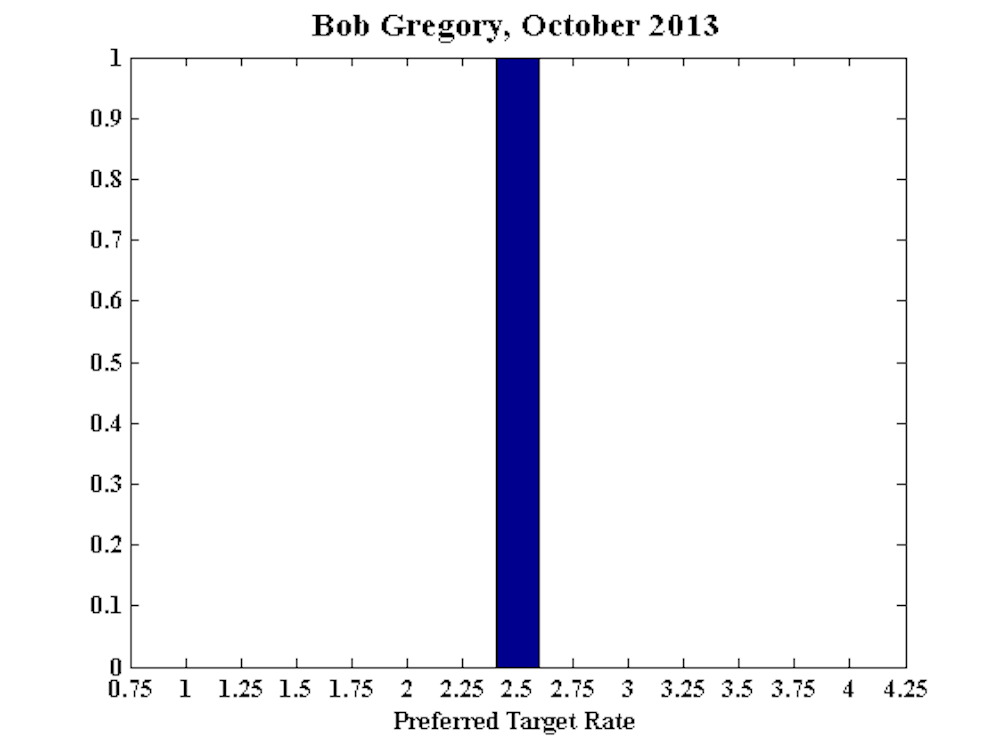

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology:

No comment.

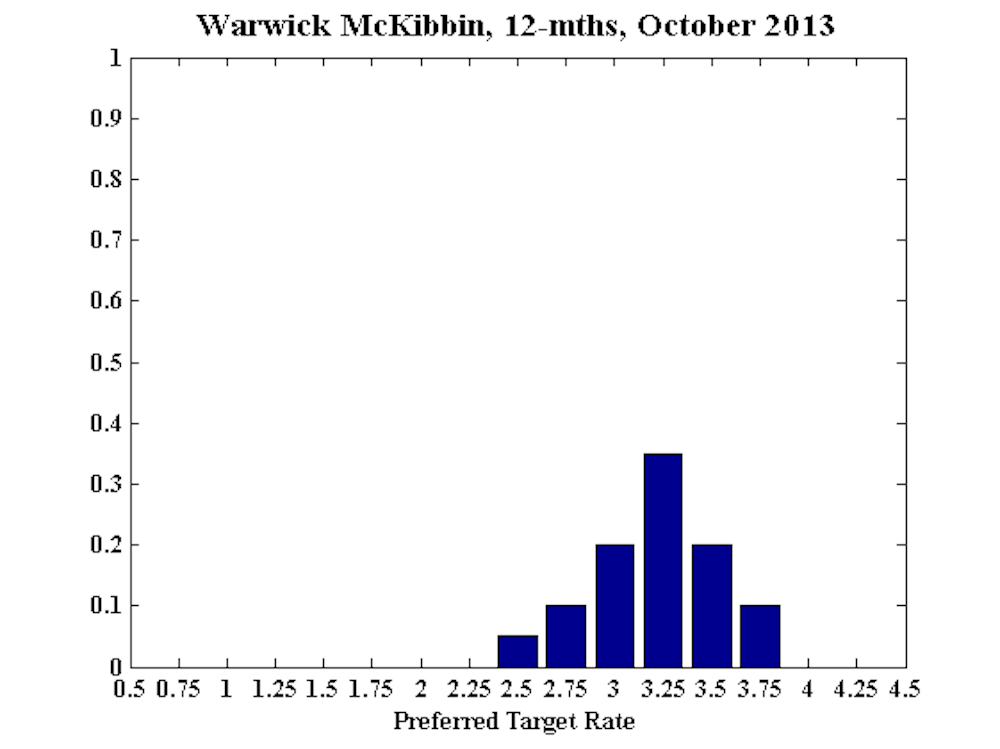

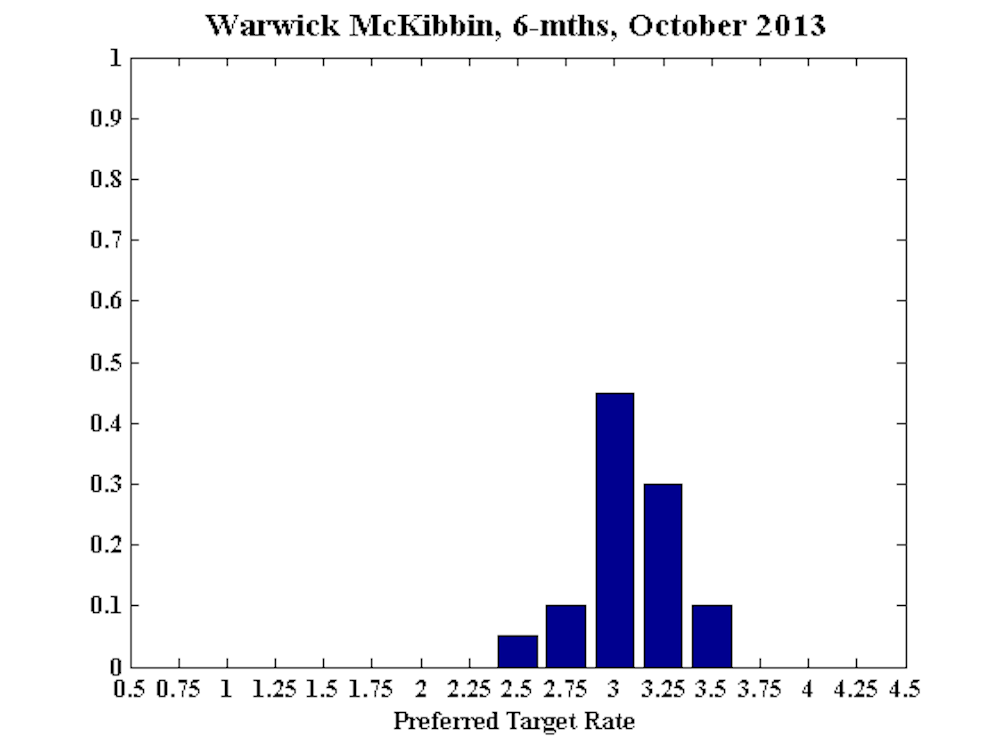

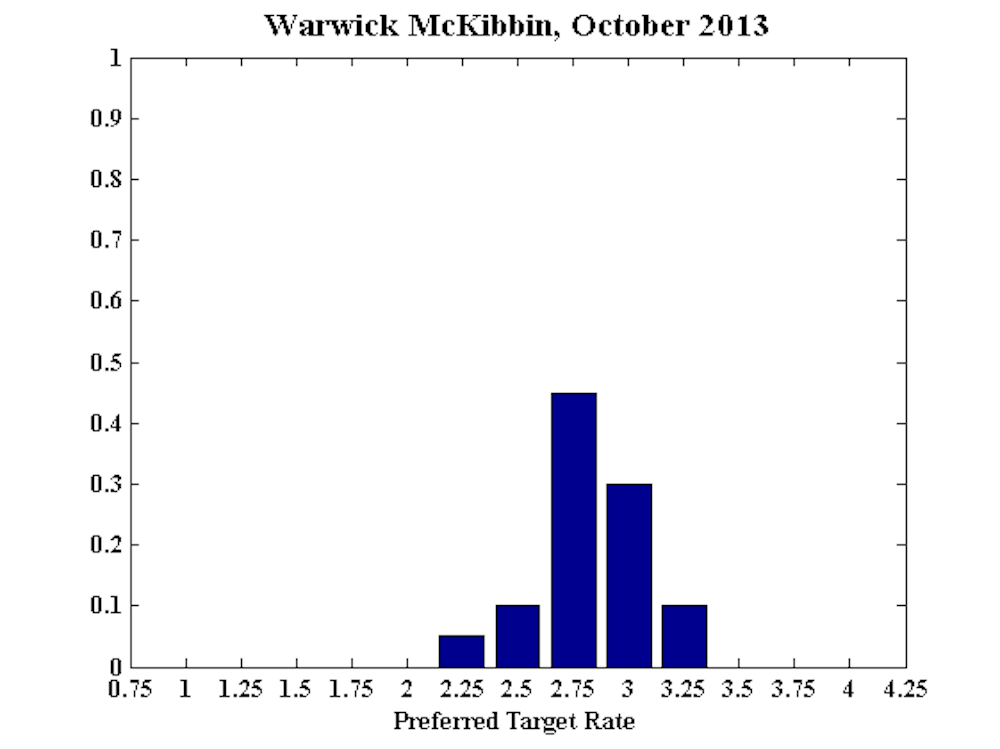

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

There is clear evidence that loose monetary policy in Australia is driving the demand for assets (especially housing) suggesting that that asset prices are inflating relative to fundamentals. The resolution of political uncertainty will likely improve confidence in the economic outlook and thus stimulate the economy. A stronger outlook for China will also reduce concerns over the outlook for the Australian economy.

Low interest rates are likely to be misallocating capital in the Australian economy and to avoid the US experience during 2001 to 2004 when rates were too low for too long a move to more normal interest rates would be advisable. A greater burden on structural adjustment should be borne by fiscal policy, particularly infrastructure spending.

Globally emerging markets are being stressed through a reallocation of global capital flows as the Fed edges closer to the end of quantitative easing. The recent surprise announcement of a continuation of bond purchases by the Fed was unwelcome news in many economies. The growing gap in the US between the data and the forward guidance by the Fed is becoming a problem for the global economy.

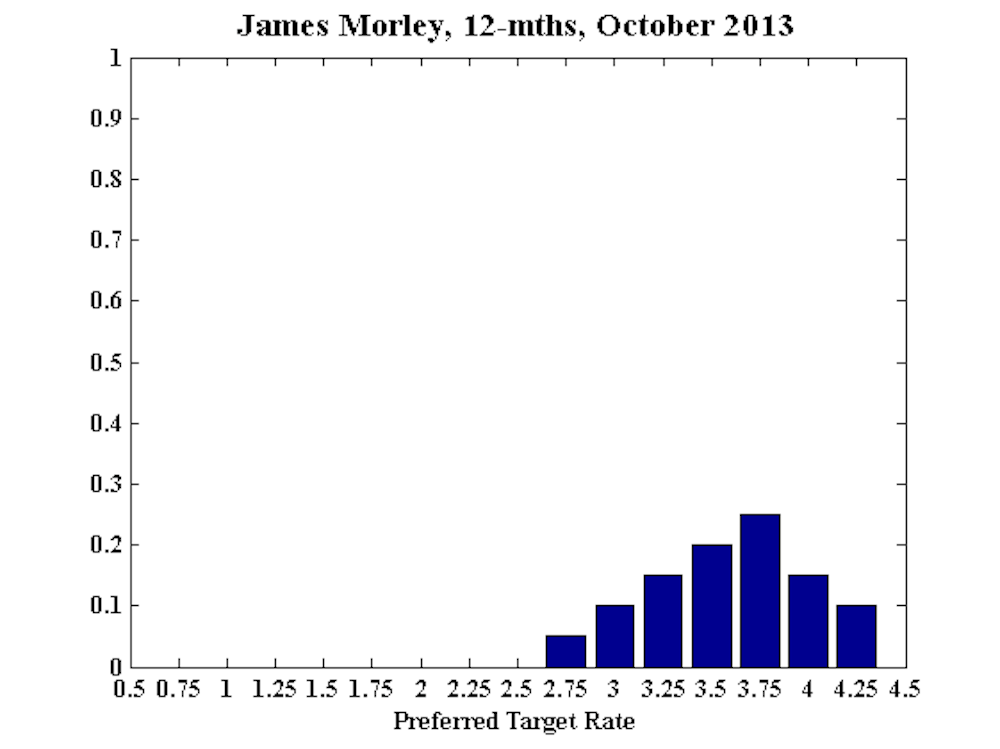

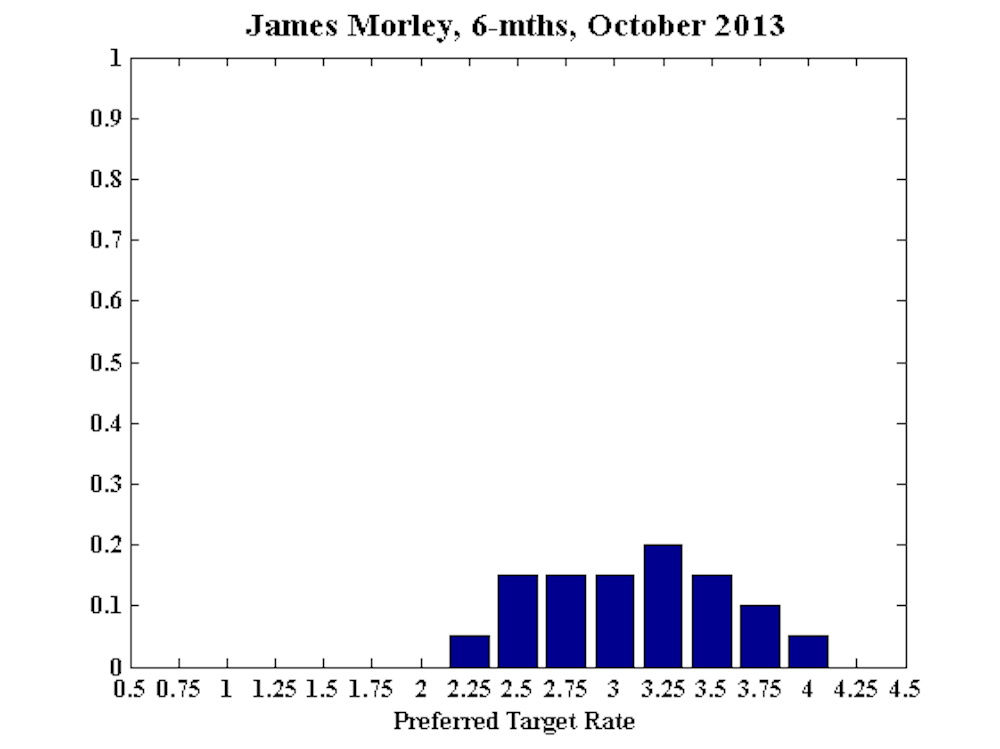

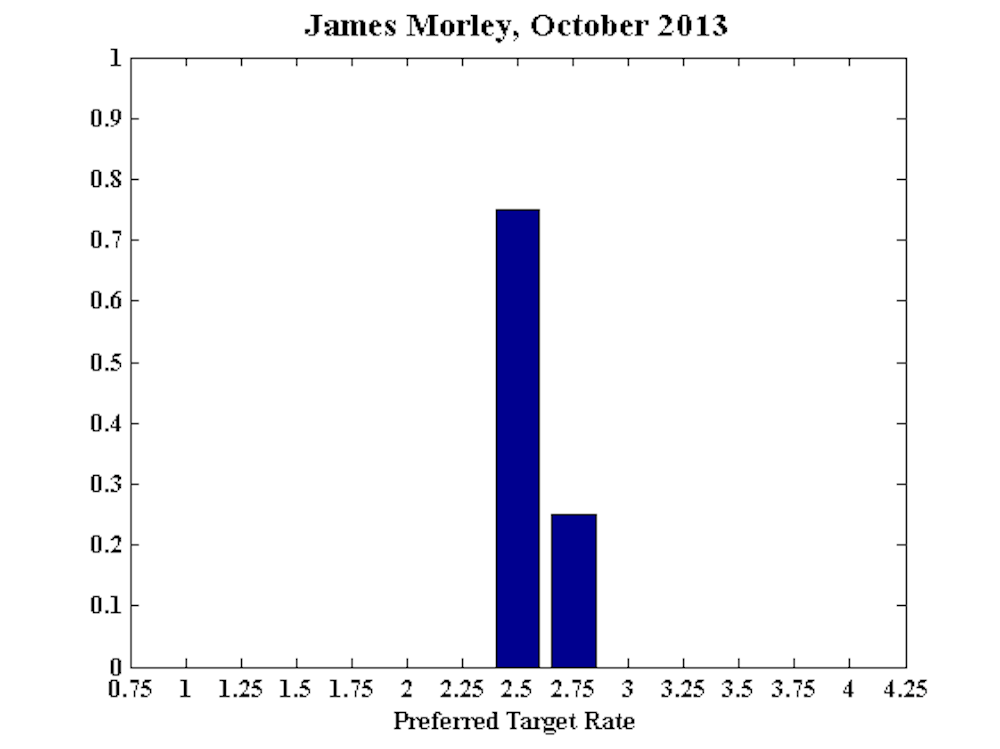

James Morley, Professor, University of New South Wales, CAMA:

The unemployment rate has continued to creep up, reaching 5.8% in August. This reflects economic growth being somewhat below potential. However, monetary policy is already quite accommodative, with the ability of policymakers to fine tune the economy to the extent of hitting a particular growth rate being very limited at best. Thus, any future decrease in the policy rate would only be appropriate if there were clear signs of a significant deterioration in the level of overall economic activity.

The RBA should continue to monitor conditions in the housing market and be ready to “take away the punch bowl” if it continues to boom in the midst of a somewhat weak economy. In particular, households should not assume that such low real interest rates will persist over the long term when making decisions about debt‐financed purchases.

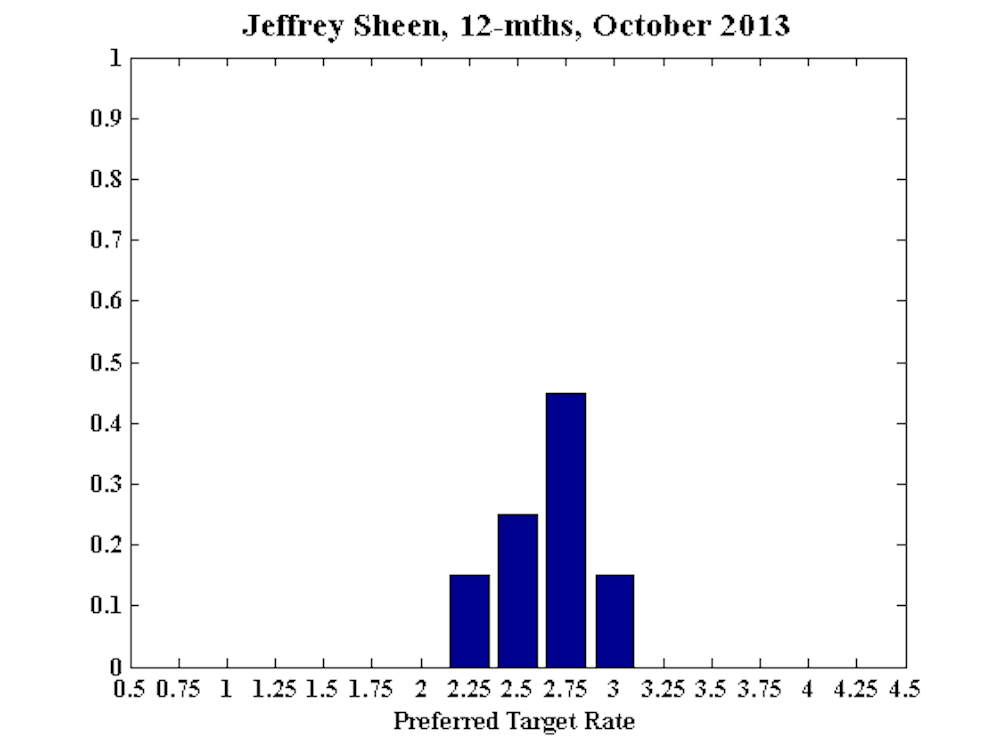

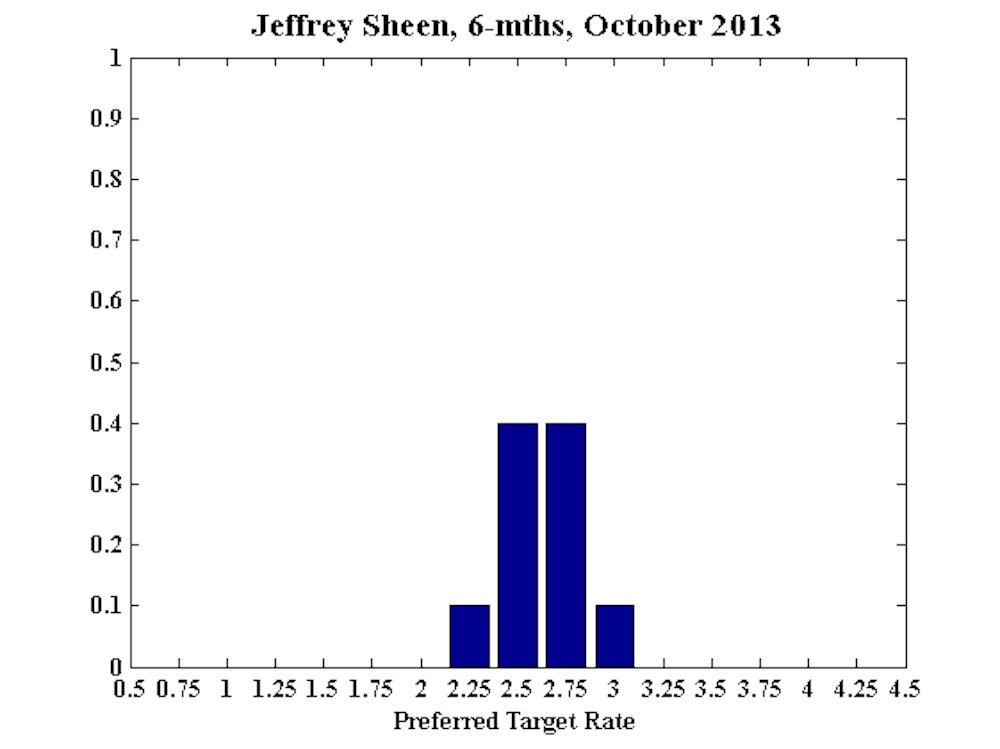

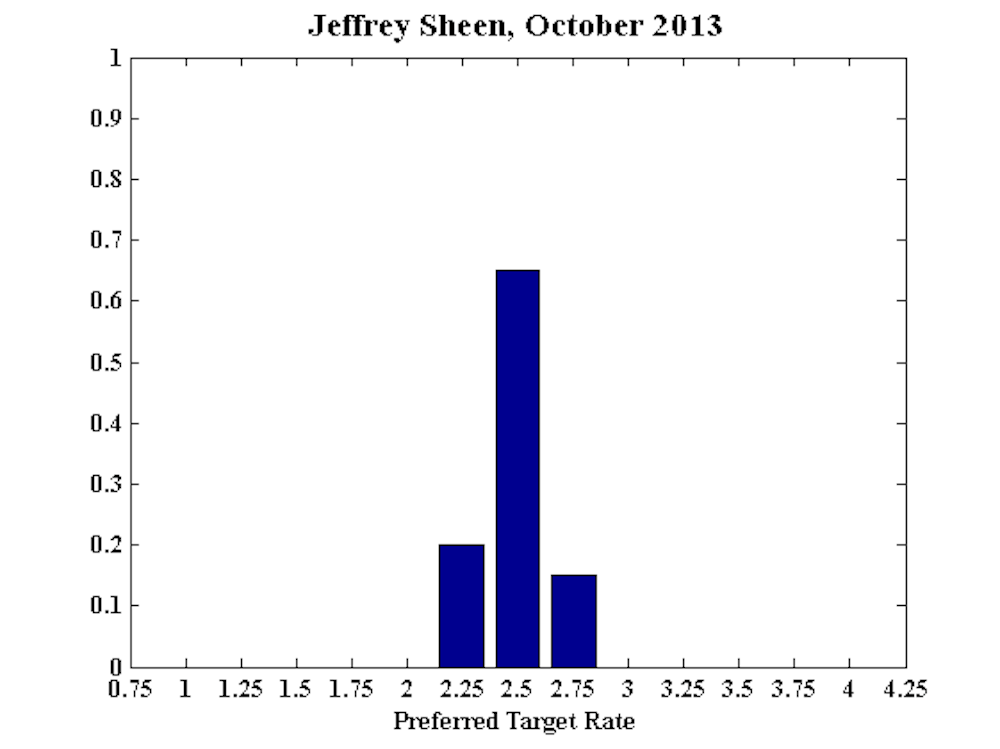

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

No comment.

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy:

Mark has resigned as a member of the Shadow Board.