A lack of news around the domestic and international economies has prompted CAMA’s Reserve Bank of Australia Shadow Board to maintain its consensus to keep the cash rate at its current level of 2.5%.

The interest rate sensitive sectors of the Australian economy - in particular the housing market - are reacting to Australia’s historically low cash rate, with signs the export sector is benefiting from an Aussie dollar below parity with the US dollar.

At the same time inflation is comfortably within the RBA’s target range of 2-3%, there remains some slack in the labour market and the Aussie dollar is relatively high. On balance the RBA can afford to maintain its accommodative policy in the near term.

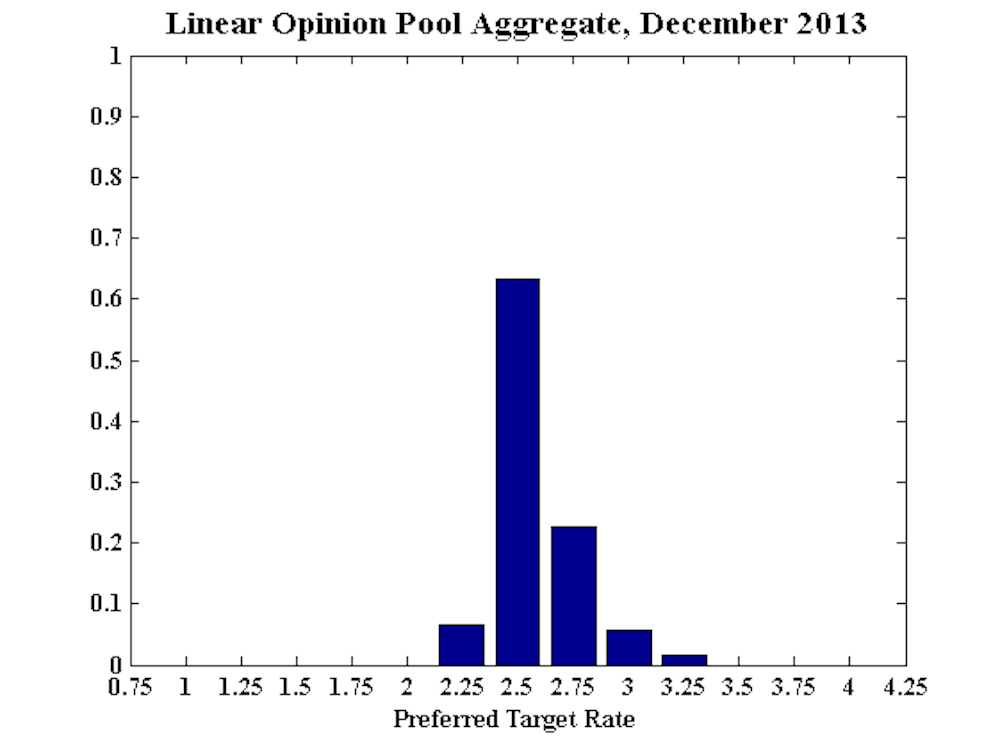

The Shadow Board’s confidence in keeping the cash rate steady equals 63% (down from 66% in November). The probability attached to a required rate cut now equals 7% while the probability of a required rate hike equals 30%.

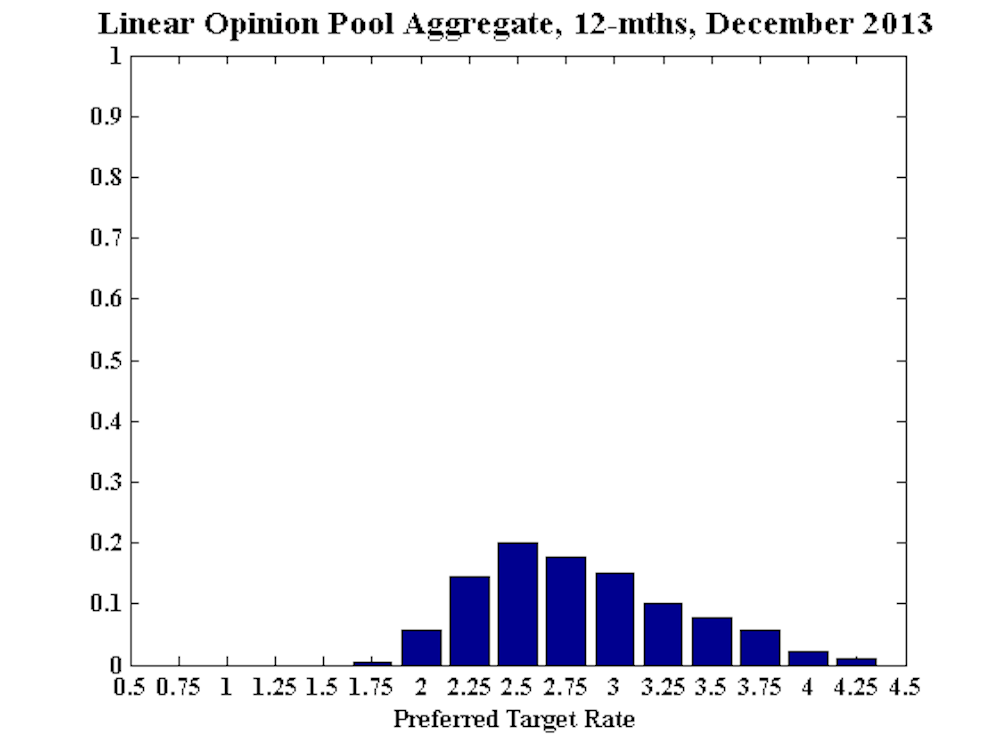

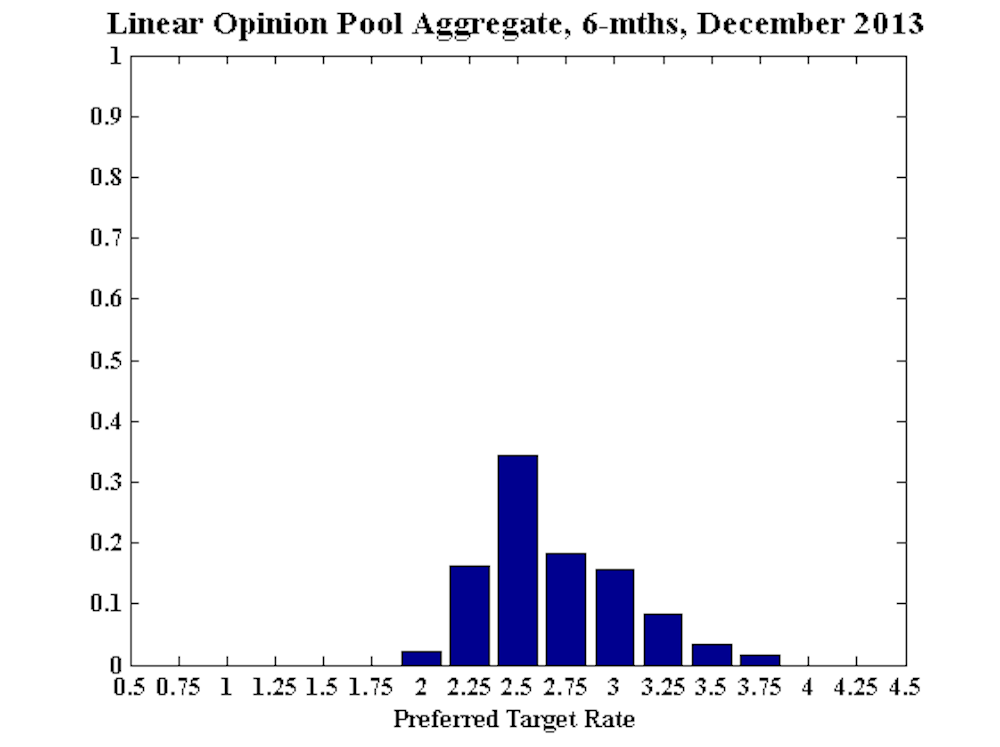

For the six month outlook, the probability that the cash rate should remain at 2.5% is unchanged at 34%. The estimated need for an interest rate increase has edged up to 47% (46% in November), while the need for a decrease has fallen to 18% (20% in October). A year out, the Shadow Board members’ confidence in a required cash rate increase has strengthened to 59% (up from 56% in November); the need for a decrease is now estimated at 21% (down from 23% in November).

The Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

The project is designed to test and improve transparency of central bank deliberations by revealing the opinions of individual members, emphasising the underlying macroeconomic uncertainties.

This is the final Shadow Board deliberation for 2013. It will return in February 2014, coinciding with the next RBA meeting for the year.

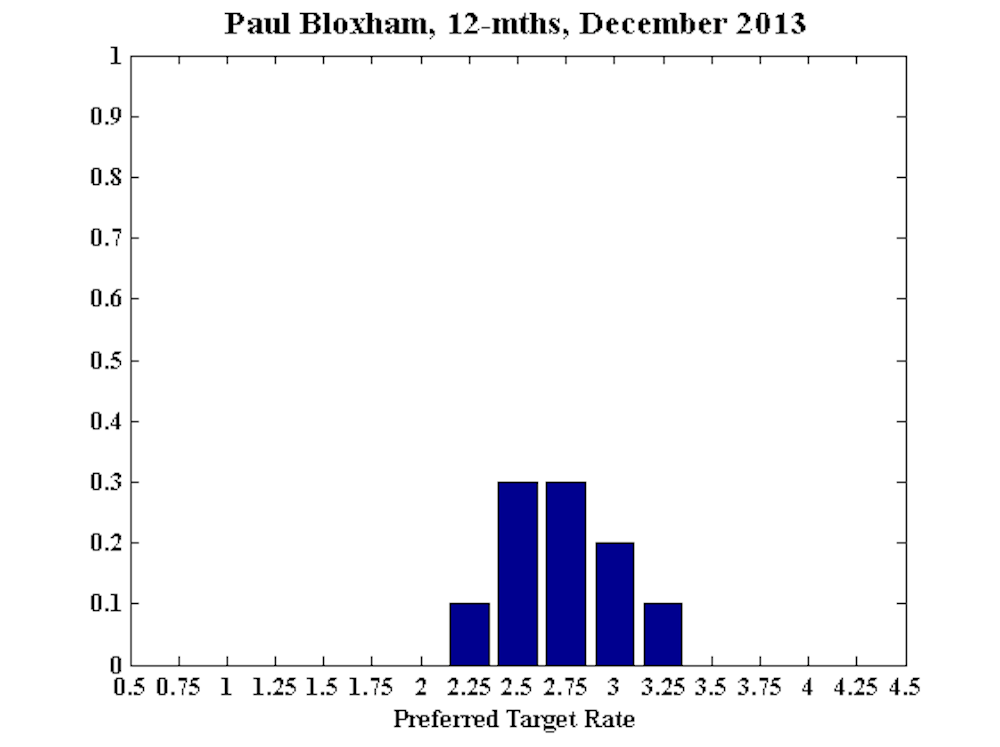

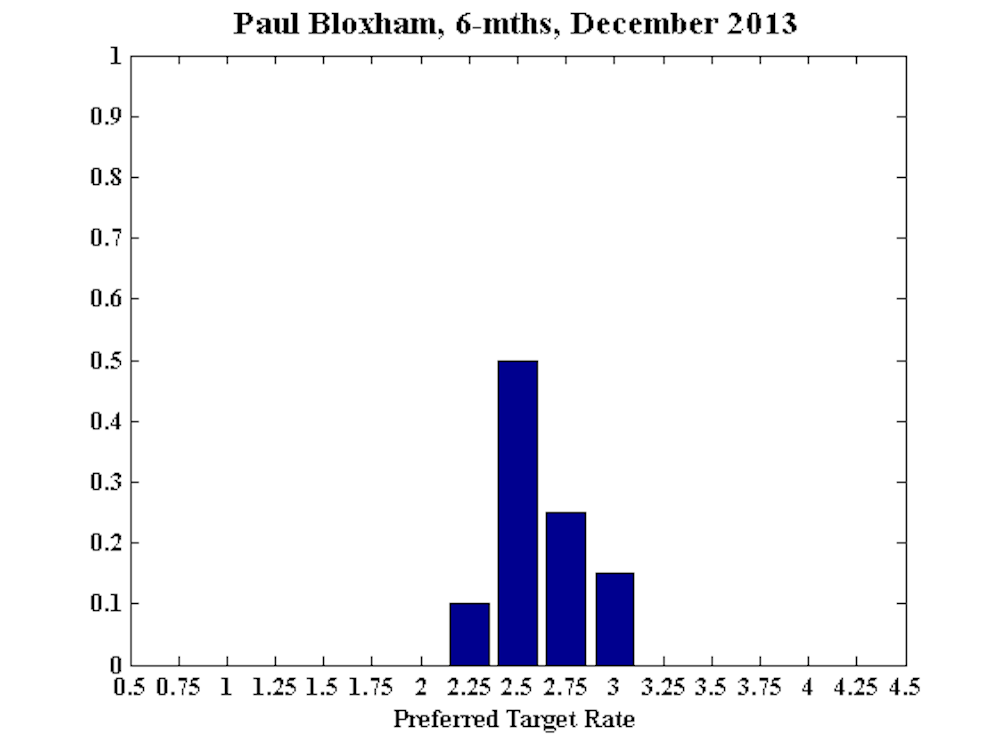

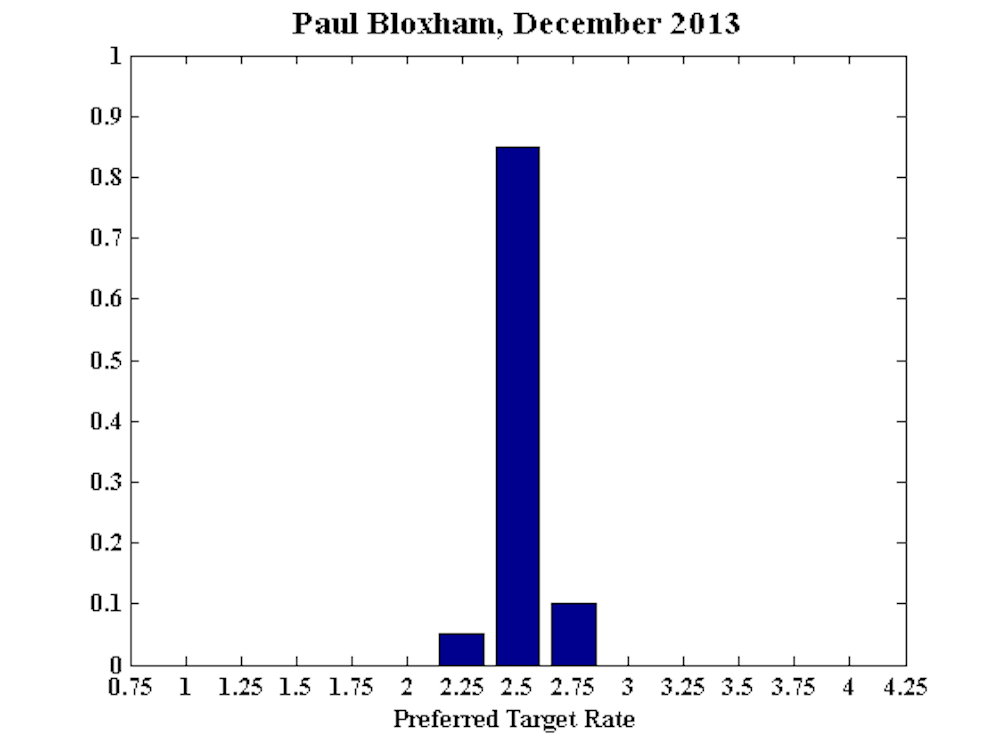

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

The interest rate sensitive sectors of the economy continue to pick up, in response to the current cash rate setting, with the housing market leading the way. There are also tentative signs that conditions are starting to improve across a broader range of industries, including the manufacturing and services sectors. As monetary policy is already getting significant traction, there would be little purpose in cutting the cash rate further, with lower rates likely to increase the risk of asset price misalignments.

However, the case for lifting rates any time soon is also fairly weak at this stage, as inflation remains contained, the labour market remains loose and the Australian dollar is still high. I recommend that the cash rate is left unchanged and see it as more likely than not that the cash rate will need to be higher than its current level in 12 months time.

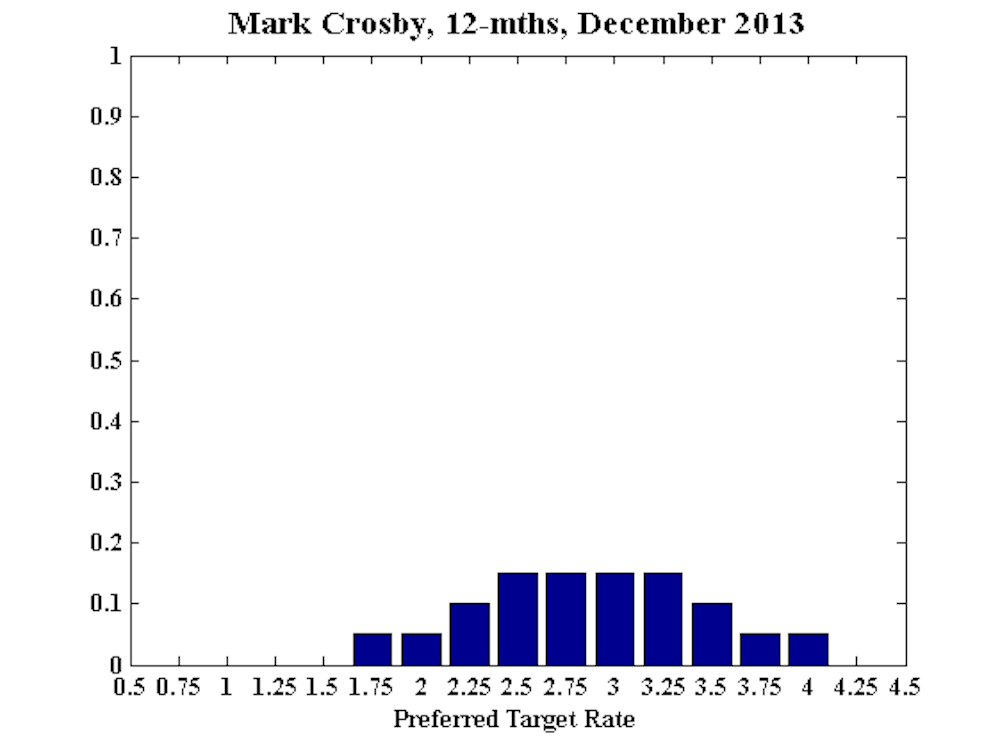

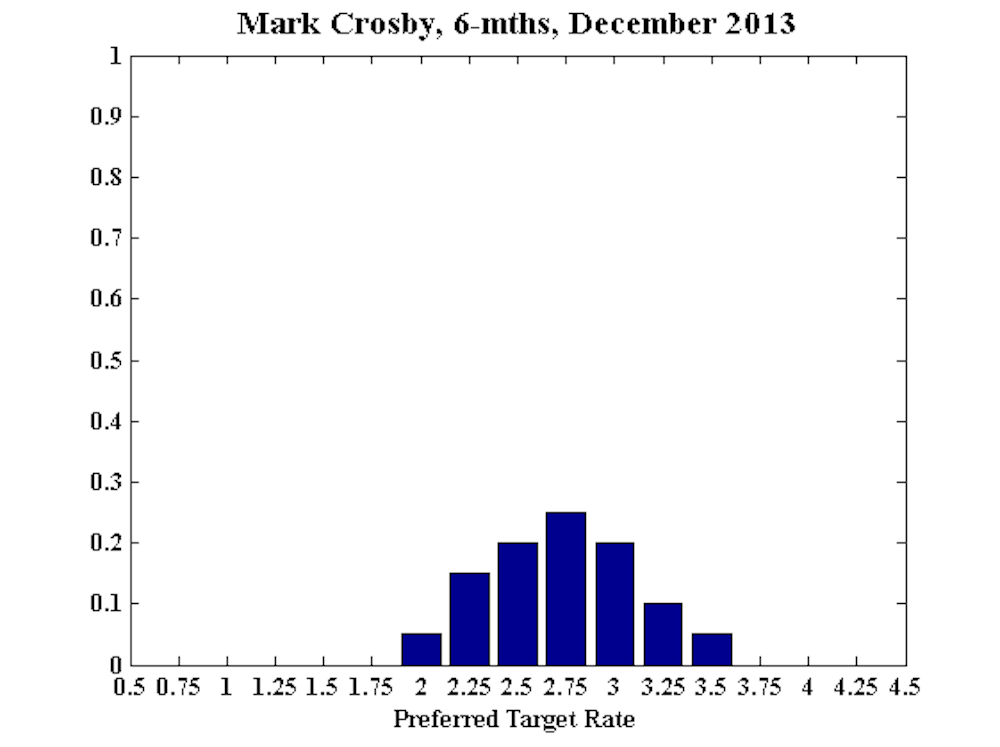

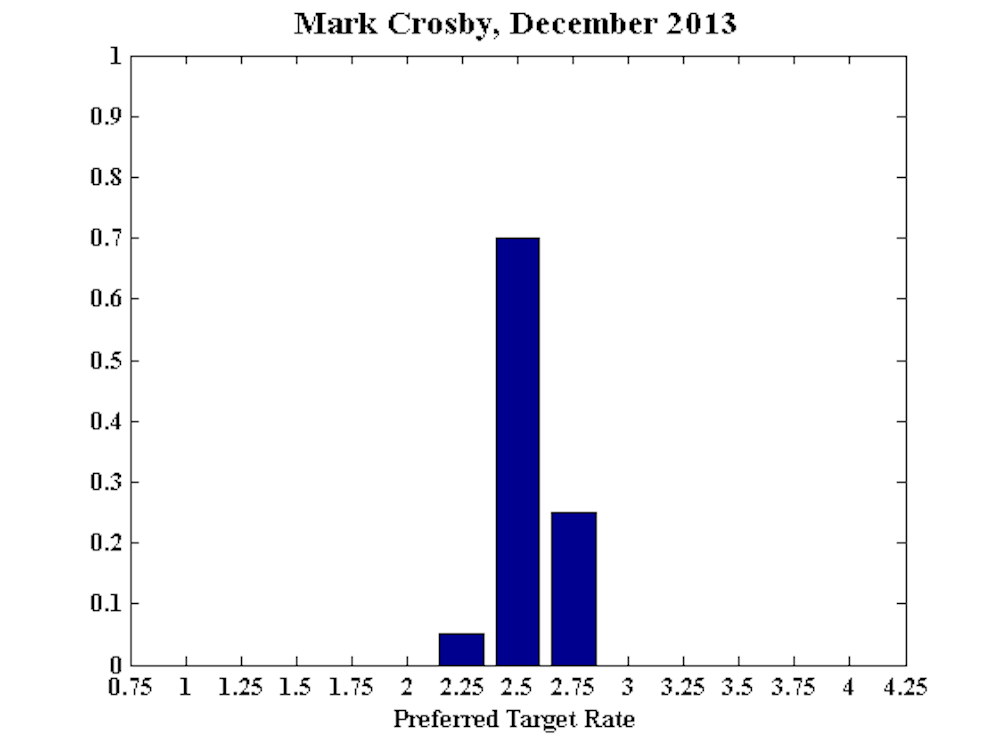

Mark Crosby, Associate Professor, Melbourne Business School:

No comment.

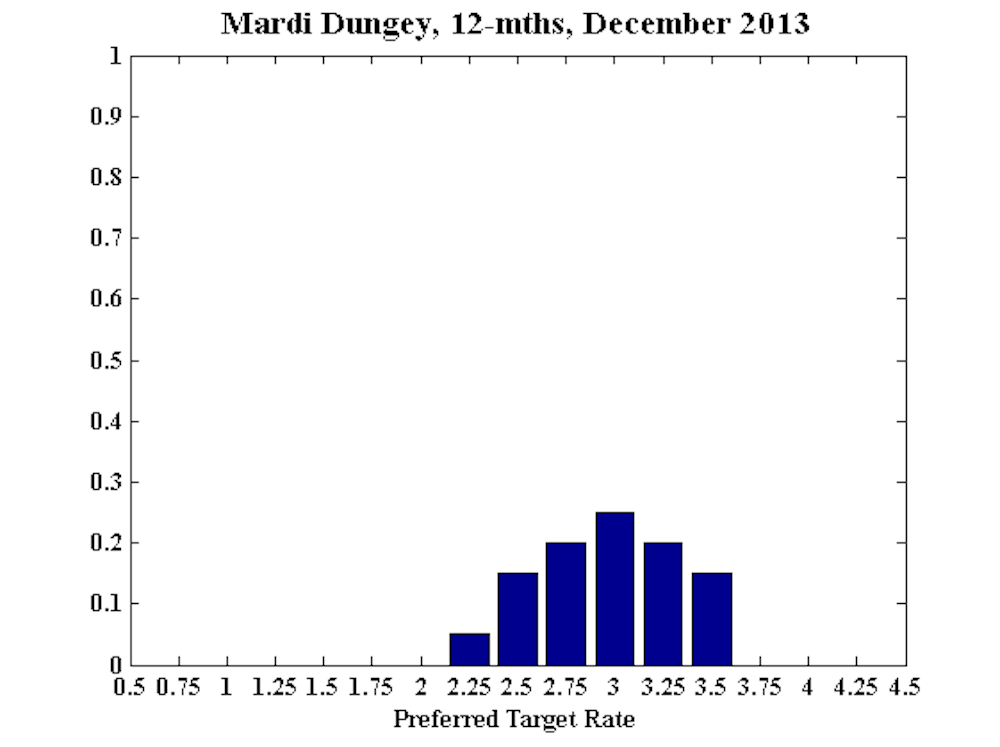

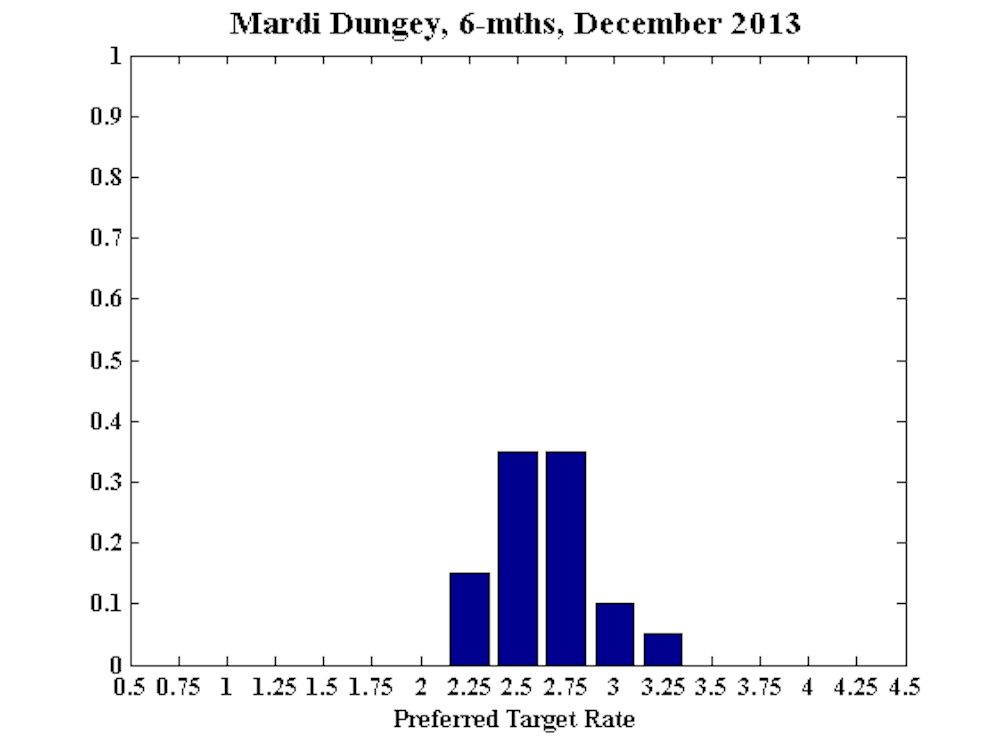

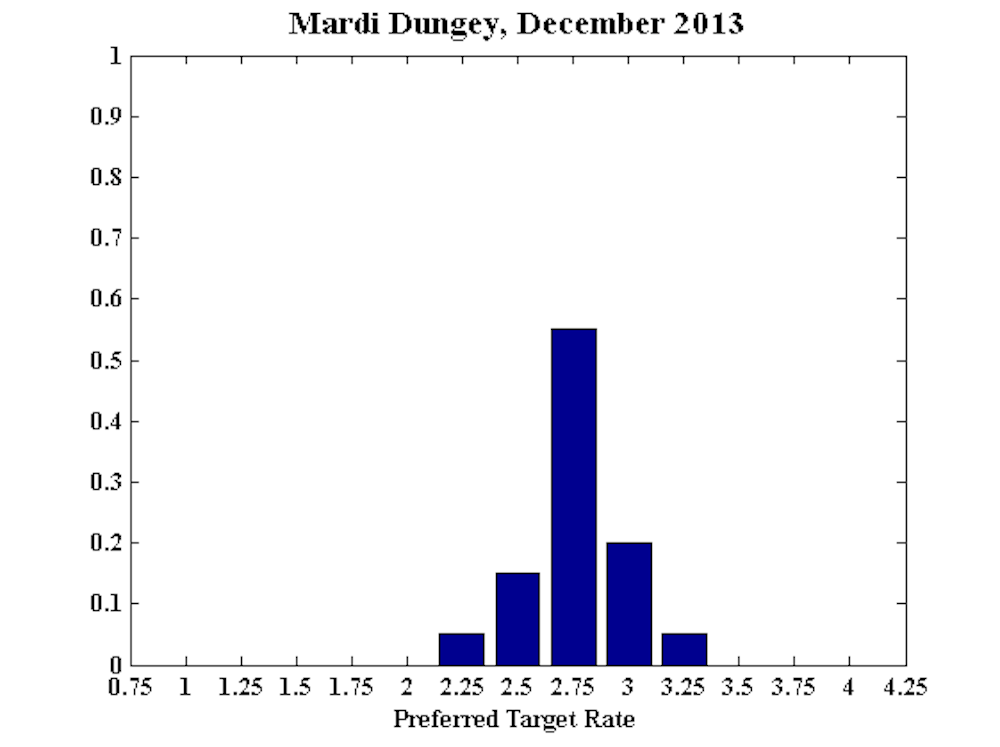

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA:

No comment.

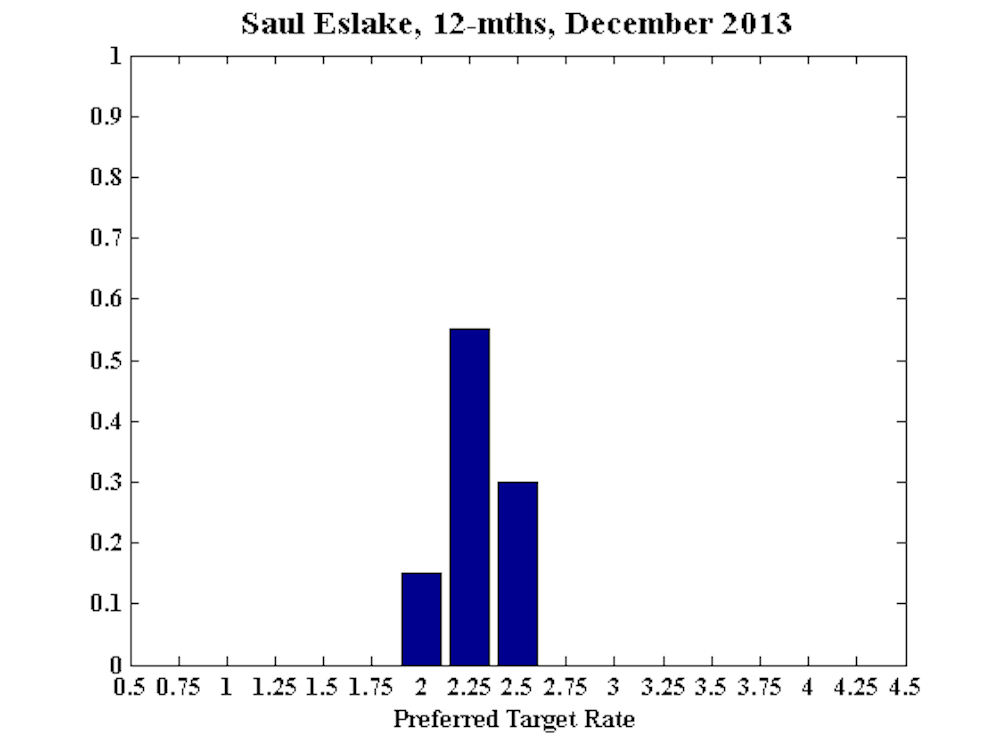

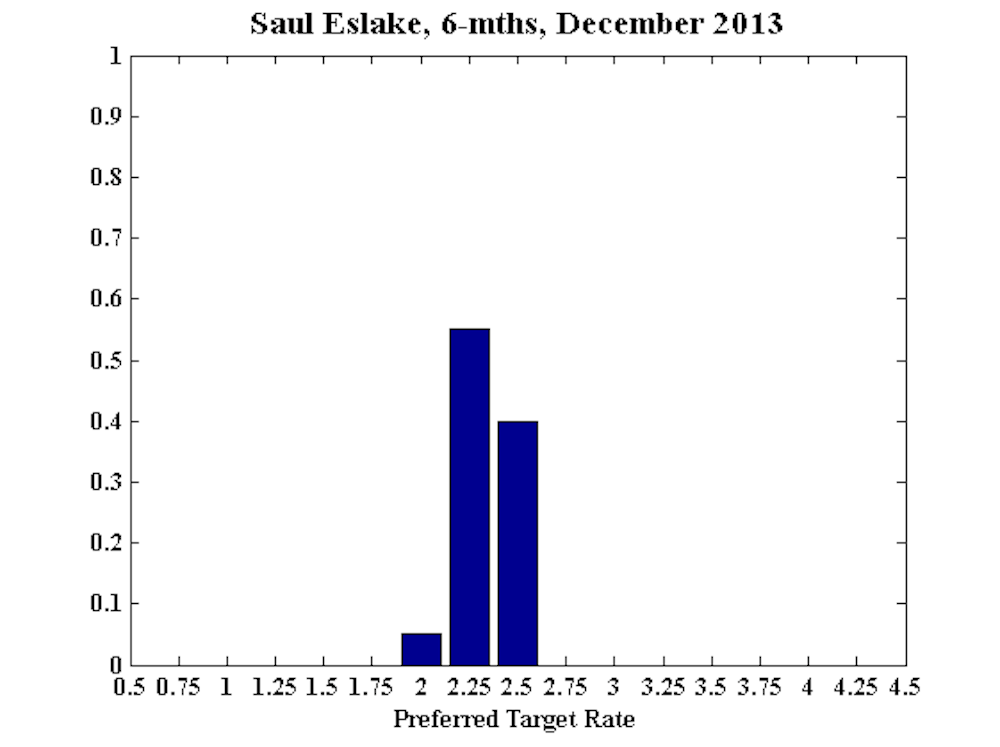

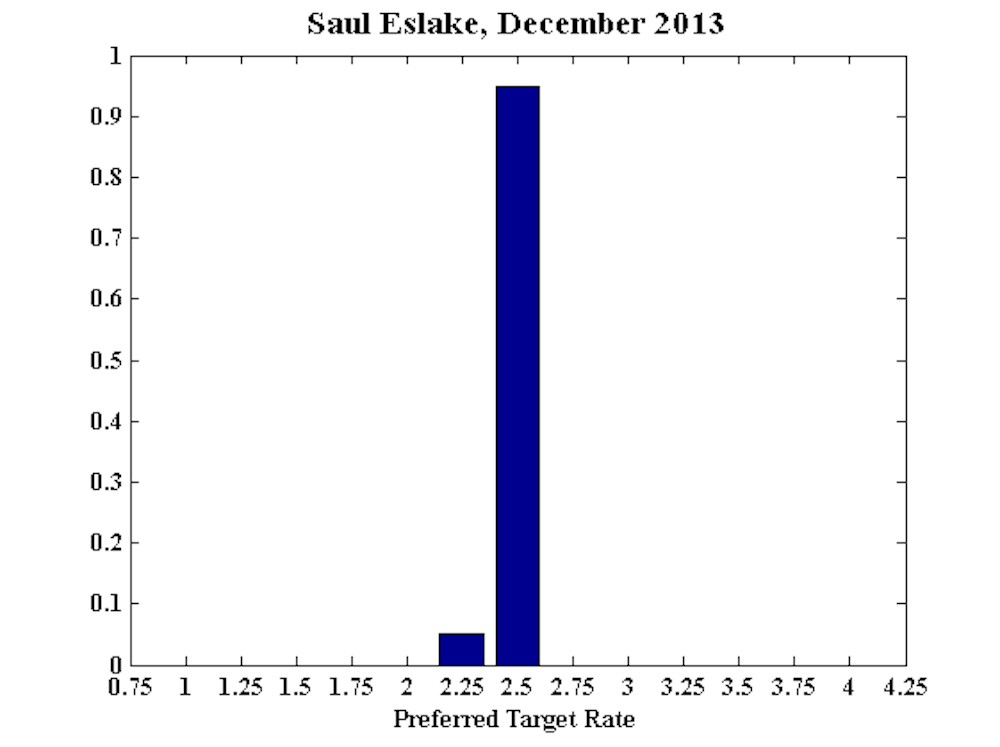

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

The RBA has made it pretty clear it is reluctant to cut rates again, and would prefer that further easing in financial conditions come via a depreciation of the exchange rate. Yesterday’s capex numbers didn’t provide any reason for them to change that view.

For the six month outlook, notwithstanding the RBA’s preference as noted above for further easing in financial conditions to come via exchange rate depreciation, unless the Australian dollar reacts sharply to the likely start to “tapering” of the US Federal Reserve’s quantitative easing program within this six‐month time frame, the dollar is likely still to be uncomfortably high, signs of a tangible revival in non‐mining investment hard to detect, consumer spending still soft, and unemployment still trending upwards – making a much stronger case for a further cut in rates.

My 12 month outlook is similar to the six month view.

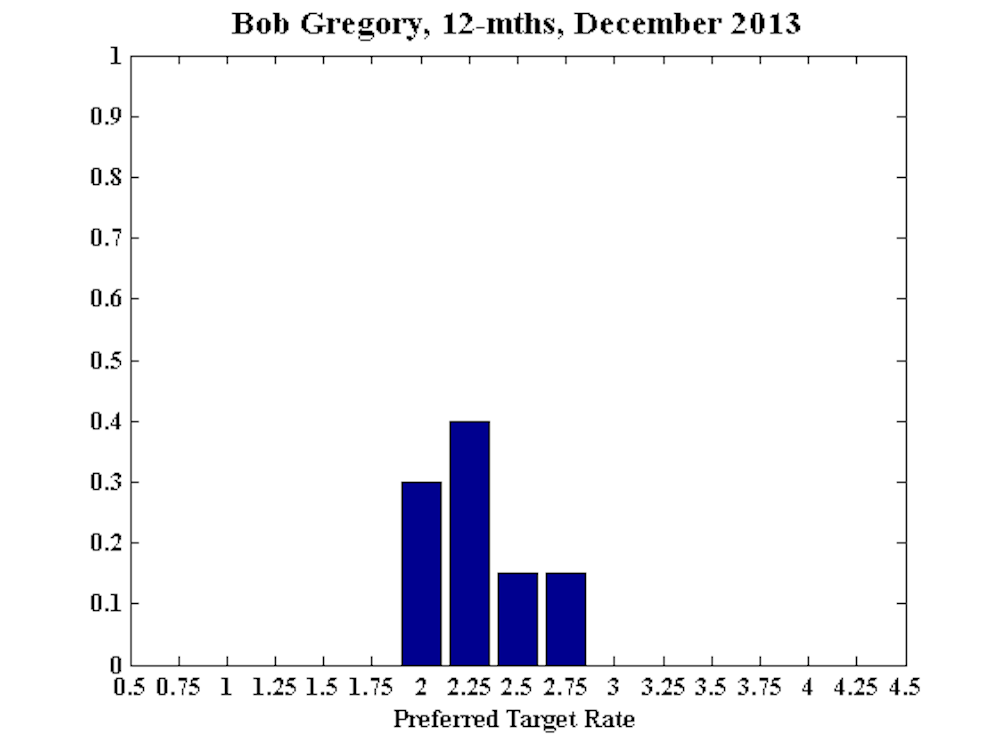

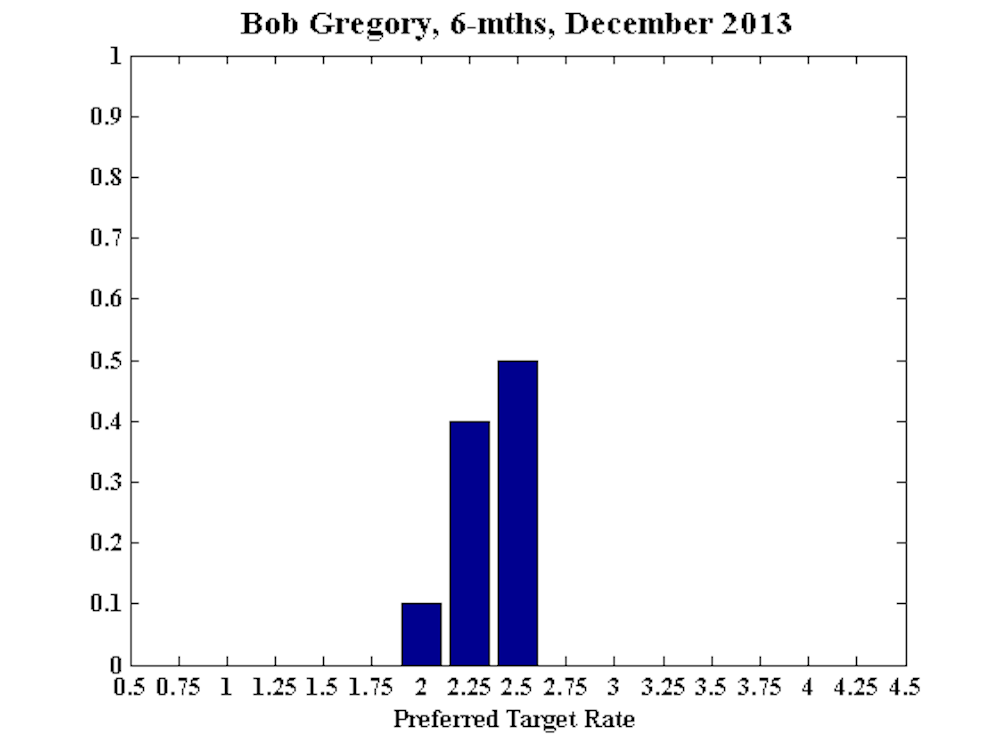

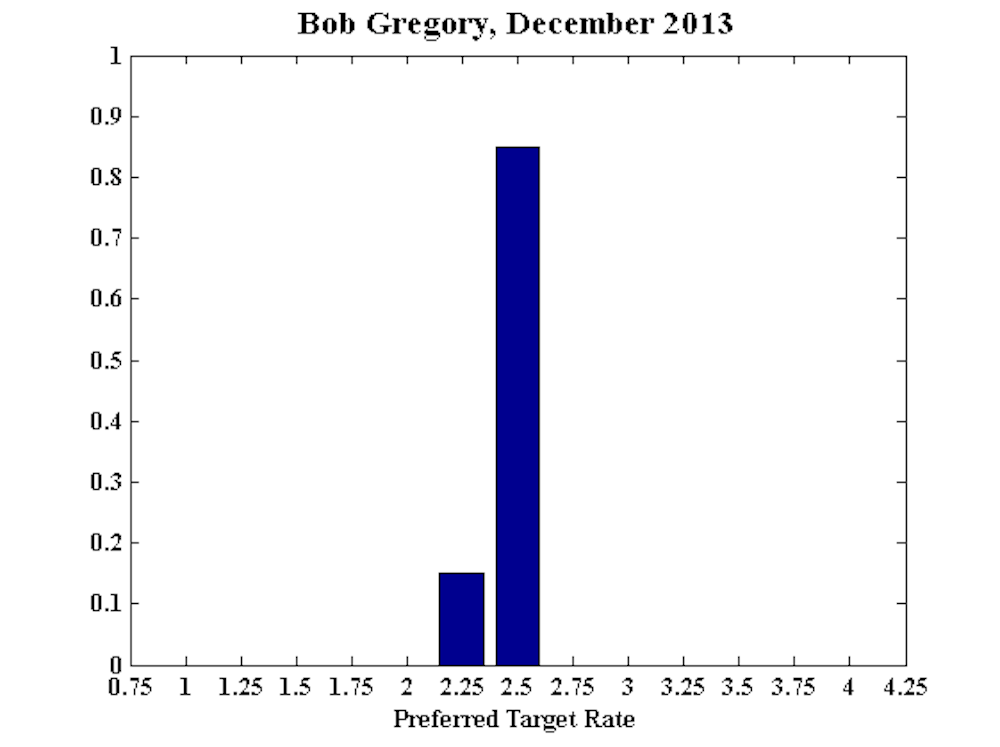

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology:

No comment.

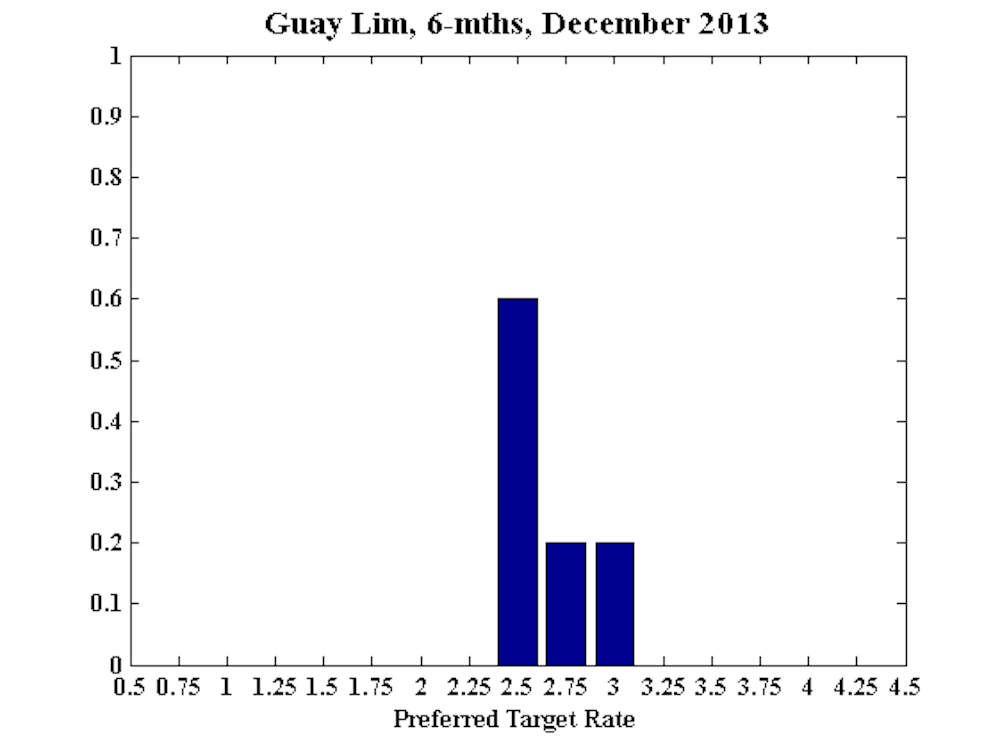

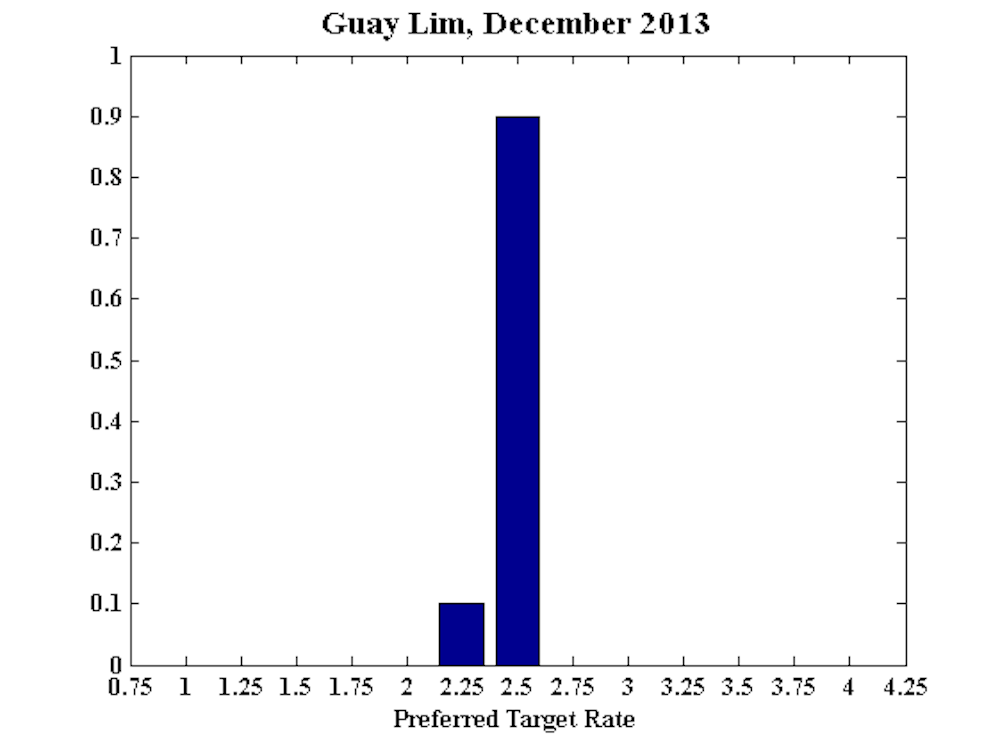

Guay Lim, Professorial Research Fellow and Deputy Director, at the Melbourne Institute of Applied Economic and Social Research, Melbourne University

Keeping the cash rate at 2.5% seems appropriate for now, and the RBA has already signalled that it is monitoring house prices and the exchange rate. Both the TD Securities‐Melbourne Institute Monthly Inflation Gauge and the Melbourne Institute Survey of Consumer Inflationary Expectations consumer expected inflation rate are within the target band of 2‐3%. There is, moreover, no clear evidence that the economy has changed gear recently, although there are encouraging signs of a pick‐up in private capital expenditure.

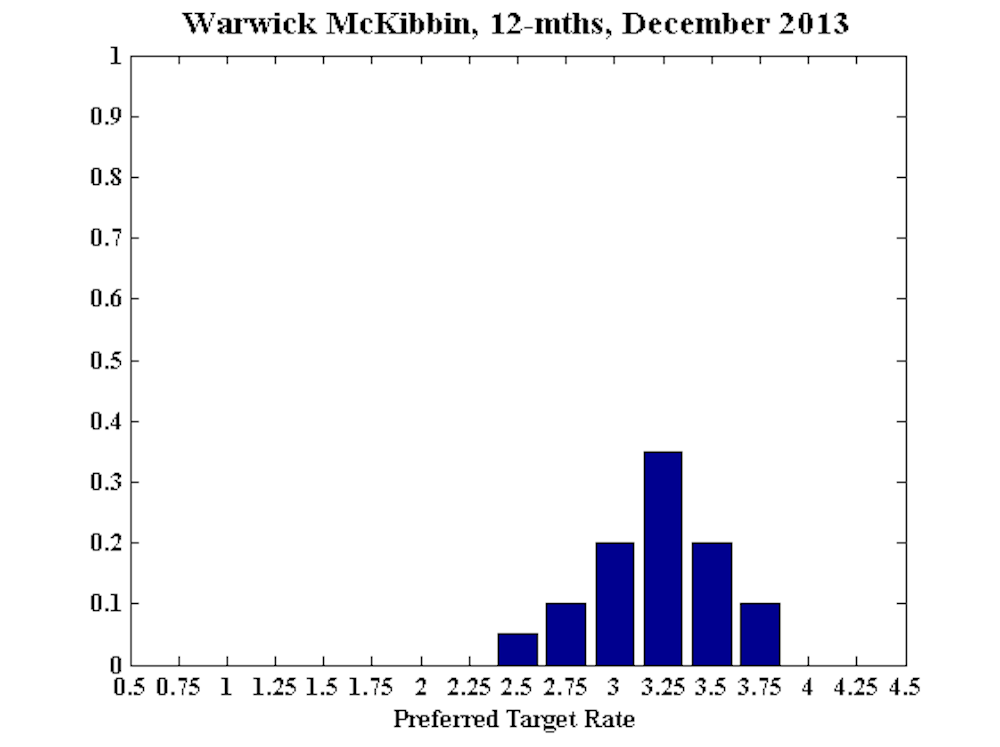

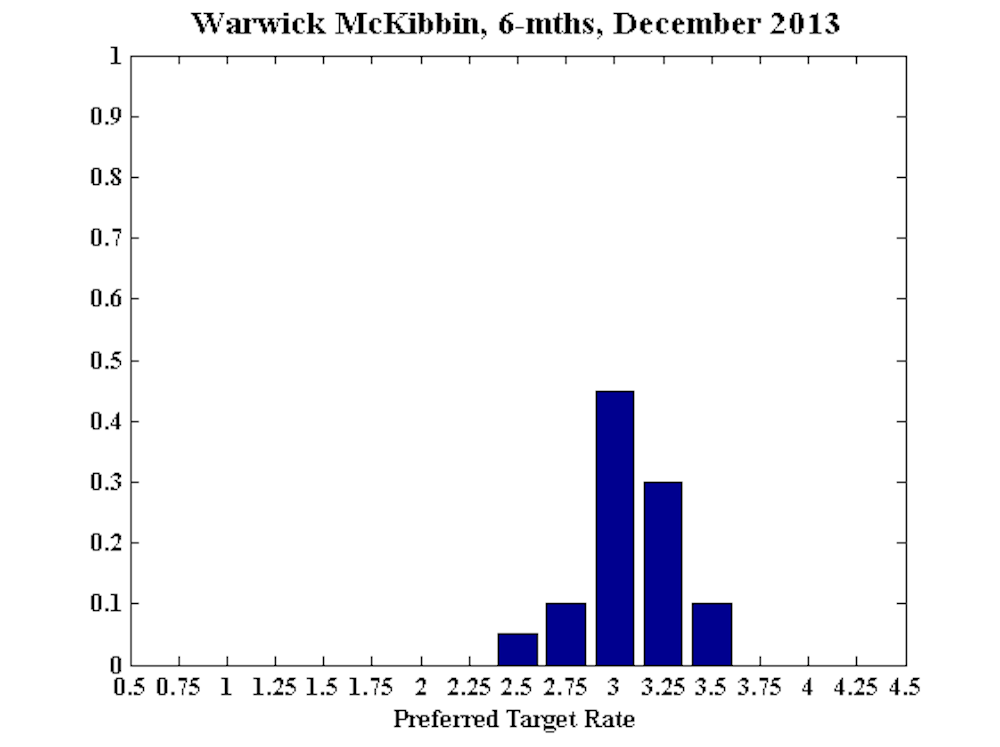

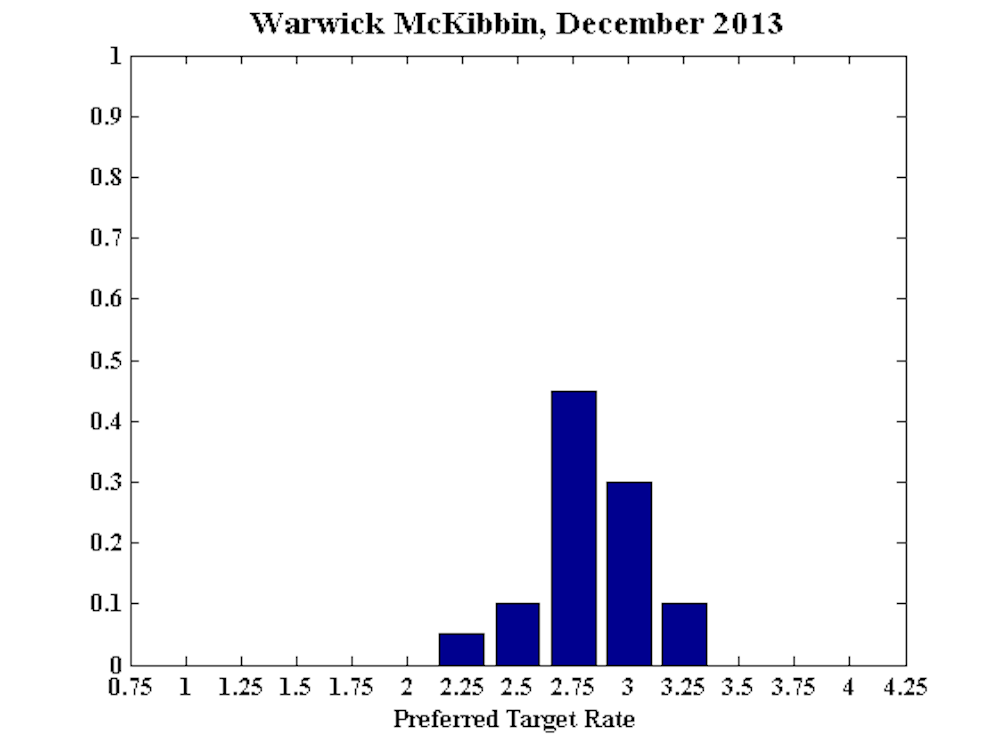

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

No comment.

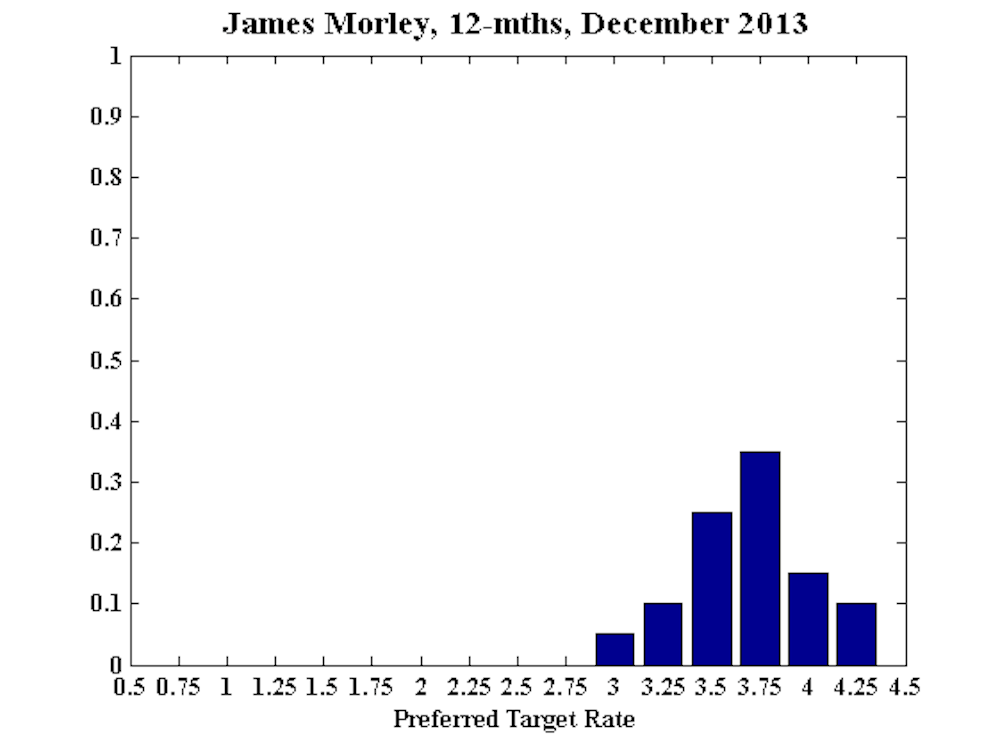

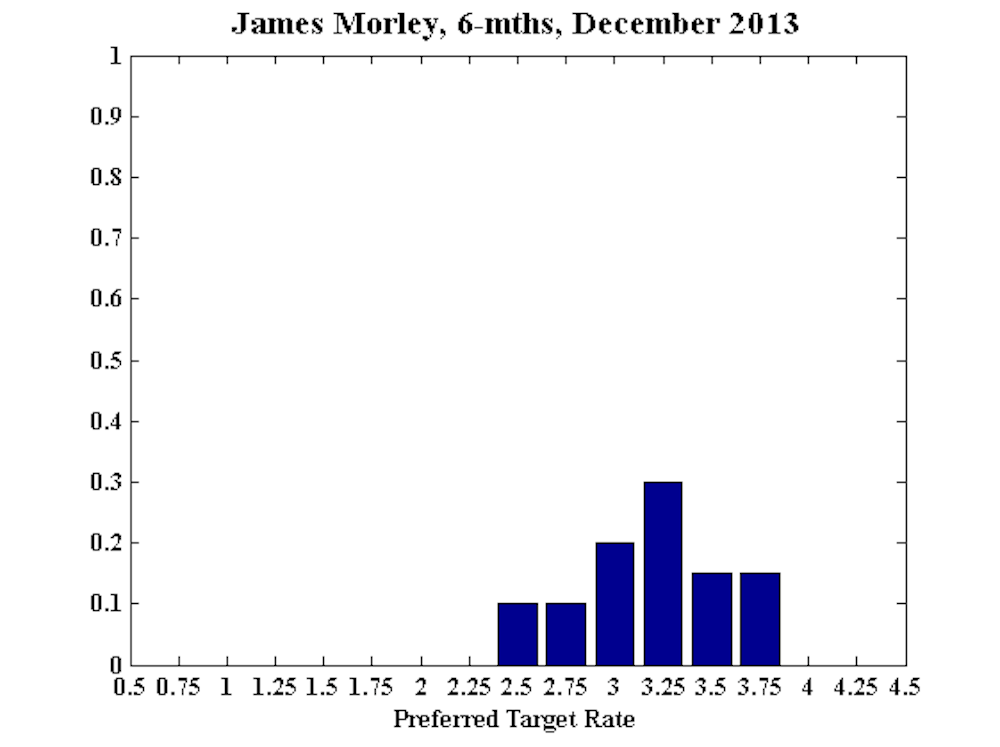

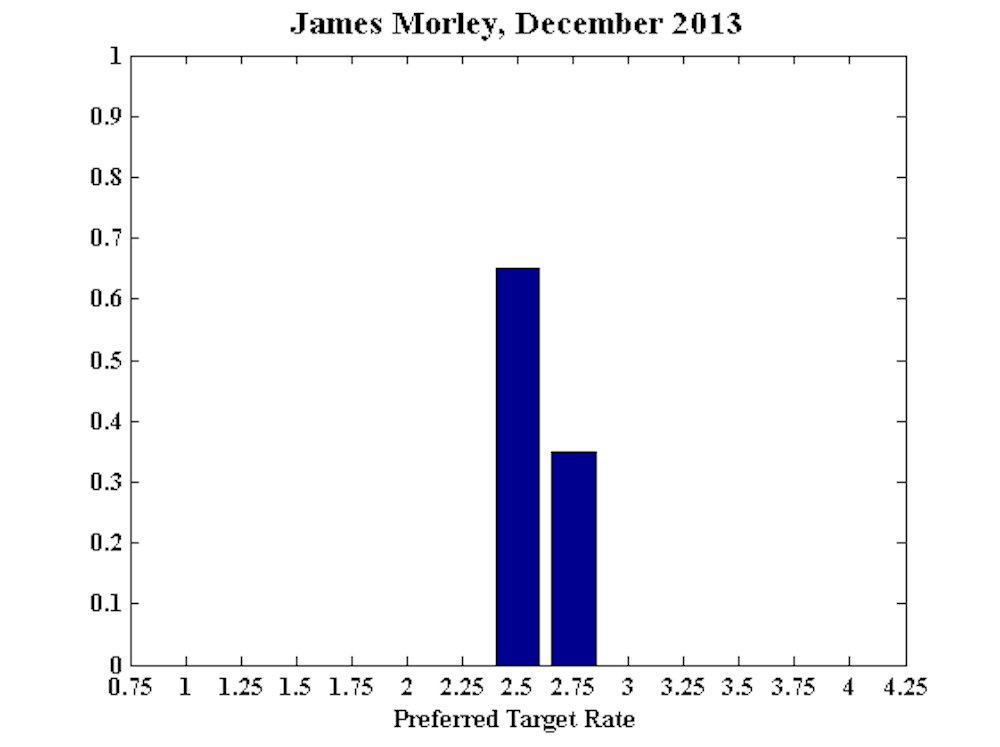

James Morley, Professor, University of New South Wales, CAMA:

The policy rate should be returned to its neutral level over the medium term. However, the current benign conditions for inflation combined with a mixed outlook for economic activity across different sectors suggests that the RBA can continue a “wait and see” approach before embarking on a tightening cycle.

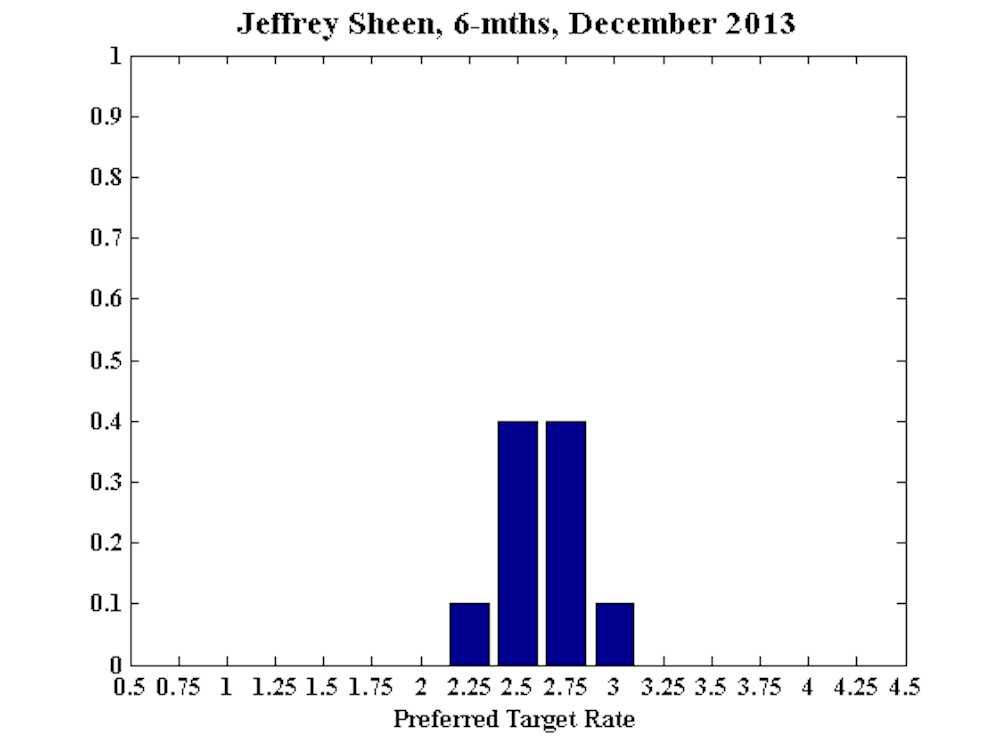

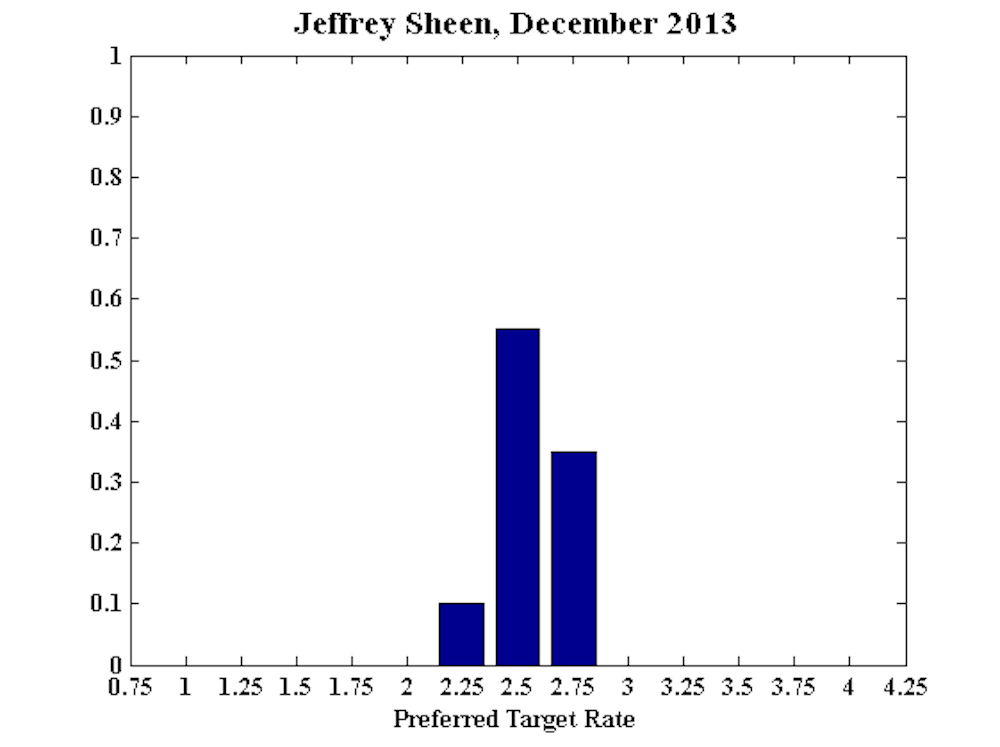

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

No comment.