A boom, like beauty, is in the eye of the beholder. A boom occurs when people rush to claim something that seems to have out-sized value. The value can arise from scarcity in the face of demand or from abundance made possible by recovering something in demand with greater ease.

For natural resources, like 19th-century gold in California, a boom is often triggered by the latter. Not all the participants find the easy gold. Often, the first to arrive see rewards, while later arrivals go home hungry.

Organic-rich black shale in Pennsylvania and North Dakota is the source of the most recent natural resources boom. Today’s “gold diggers” are finding huge quantities of natural gas in Pennsylvania’s Marcellus Formation and oil in North Dakota’s Bakken. These two formations contain the largest US reservoirs of recoverable gas and oil, though other black shale sources across the country offer significant resource potential.

The ability to economically extract gas and more recently oil from shale is one of the greatest paradigm shifts in the global energy system. I played a role in that shift when my nearly 40 years of research on gas shale in Pennsylvania contributed over the past decade to a better understanding of unconventional gas fields.

Since then, production of gas and oil has surged, making the US the world’s top producer of oil and gas. But already, just a few years after my reserve calculations in 2008 identified the Appalachian Basin as the world’s largest unconventional gas field, the Organization of the Petroleum Exporting Countries – a cartel of 12 oil-exporting countries led by Saudi Arabia – is arguing the boom is about to go bust.

A report released by OPEC in April asserted that US oil supplies would grow to 13.65 million barrels a day in the second quarter and then level off before beginning a steady decline by the end of the year. While there has been an inevitable decline in production as a result of the sharp drop in oil prices last year, is OPEC correct to predict US suppliers will never recover their peak levels of production?

The boom’s first ‘bust’

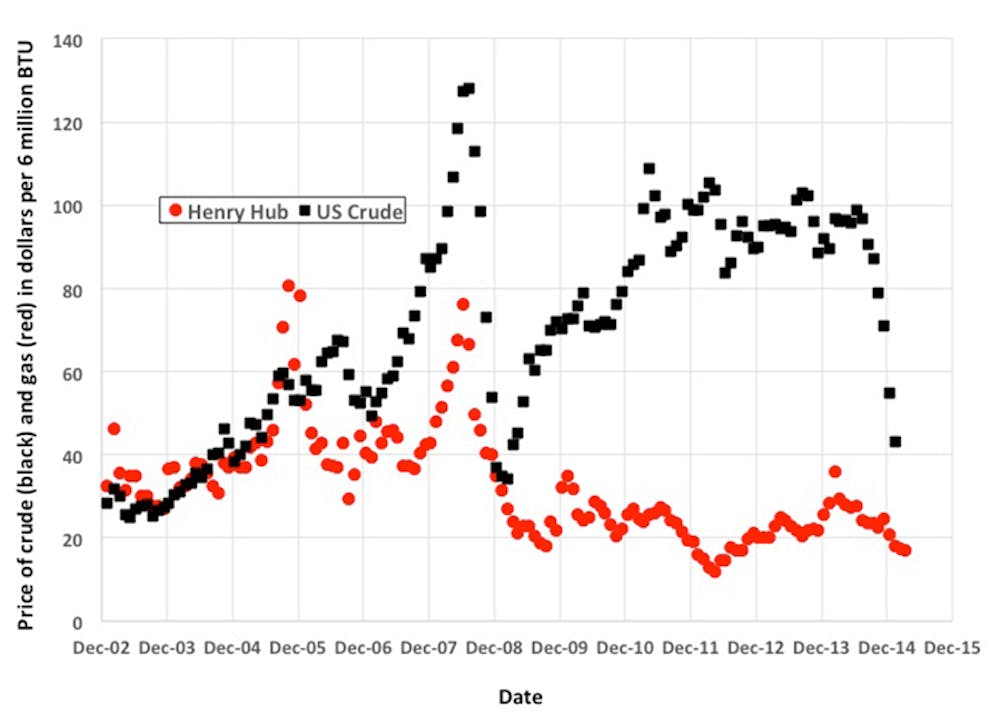

It may be argued that the boom in both Pennsylvania and North Dakota was triggered by a combination of higher prices and easier access. During the 2000s, the prices of oil and gas were coupled in an upward drift culminating in the 2007-2008 price spike that ended with the collapse of the economy in 2008, when both plunged.

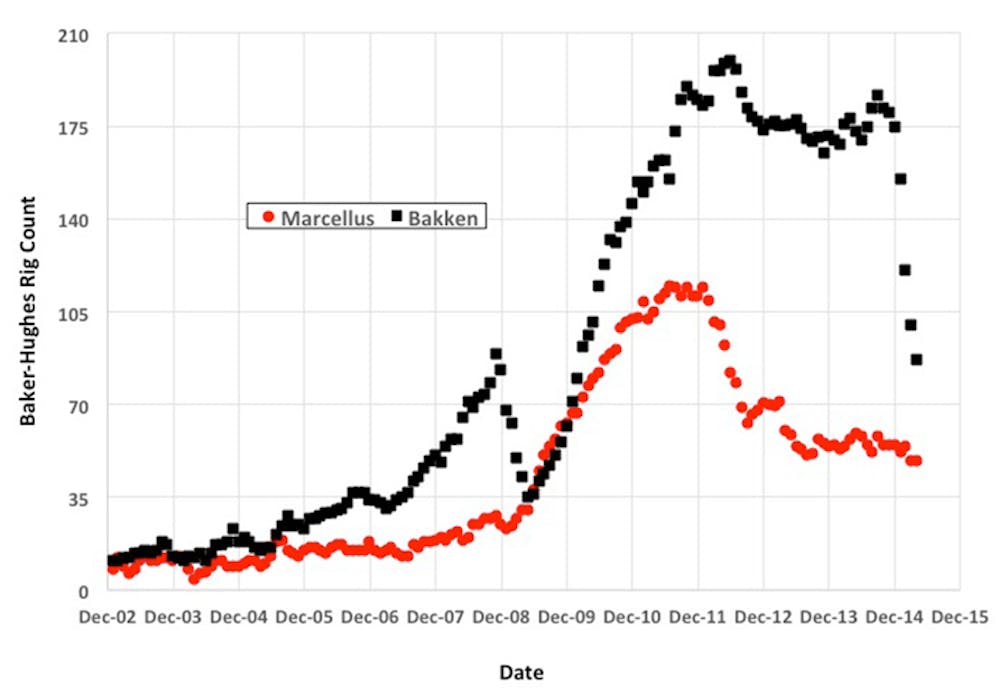

Drill rigs are the modern gold miners in places like Pennsylvania and North Dakota, where the rig count is as sure a measure of a boom as any. This spike and collapse of prices was mirrored by the rig count in both places, which lags price declines by several months because rigs can’t be demobilized instantaneously. But the boom was far from over despite the collapse in prices – as improvements in technology ensured that access kept getting easier and plenty of oil and gas remained under the Earth, ready to be tapped.

By 2009 a huge amount of money had been spent on oil and gas leases, especially in Pennsylvania. To protect this billion-dollar investment, the shale gas boom continued independently of falling prices. The effect was that gas prices decoupled from oil in January 2009 and stabilized at about $3.5 per thousand cubic feet – compared with a peak of just under $13 – whereas oil started to recover and returned to the $80 a barrel range in 2010, within 12 months of its crisis low of under $40.

By then, the oil and gas rush was back on. The Marcellus surpassed its pre-collapse peak rig count by April 2009, while the Bakken surged beyond its previous peak a year later. Both plays arrived at their maximum rig counts, the peak of the boom, about a year apart in 2011 and 2012, respectively.

At that point, however, the market realities finally caught up with energy producers. For the Marcellus gas boom, the rig count slipped downward by about 50% by the end of 2012 because of lower prices. The same downward adjustment of rigs in the Bakken is presently taking place, driven by last year’s sharp drop in oil prices. As measured by rig counts, both booms ended without any help from OPEC.

Wishful thinking?

A boom, like beauty, is only skin deep. OPEC hopes that the recent downturn in rigs reflects the amount of oil in the ground. If the Bakken goes dry, the argument goes, the US will again compete with the international community to buy OPEC oil at, say, $90 to $100 a barrel. This is wishful thinking.

There are American analysts who also see a return to the pre-shale, business-with-OPEC days largely based on steep production decline rates and poorer average well performances. Industry players and investors have already planned drilling and production programs that account for the former. It is the latter that would inevitably lead the charge back to OPEC.

Any substantial increase in oil prices will bring rigs, and hence production back. Rigs are becoming more efficient so that the break-even price for rigs is getting lower and lower, which will stabilize production and slow the decline even with low prices.

In this regard, Pennsylvania gas serves as a model for North Dakota oil production. Despite the cutback in rigs starting back in January 2012, gas production in Pennsylvania continued to increase for 12 straight quarters to reach total annual production of more than 4 trillion cubic feet by the end of 2014.

Pennsylvania’s boom ends but payments continue

The boom in Pennsylvania, as measured by the number of roustabouts (the people who run the drill rigs) or the length of drill rod or any other measure, came to an end three years ago. Because of the stable price of gas since the summer of 2009, however, royalty payments, to take one example, have continued to have an impact on the economy of Pennsylvania.

Royalty payments are based on production that has continued to increase even after the boom ended. It’s very clear that fewer rigs can sustain production, at least until the sweet spots are drilled up. In Pennsylvania, that is sometime in the future.

Although somewhat less elastic, oil production can be held within the limits of profitability as well even when the rig count drops. During the first two months of 2015, the Bakken rig count dropped 31%, while production only dipped 4%.

In 2014, the Bakken rig count was steady at about 170, while production increased 34%. For a while in these shale plays, adding production from new wells more than compensates for decline in production from older wells. Of course, this is not sustainable forever, but OPEC is jumping the gun with its predictions of a dramatic decline anytime soon.

A production-sustaining rig count might be on the order of 140 for the Bakken. There is little doubt that the Bakken rig count will respond to current low prices by adjusting downward. If OPEC can live on a stable price of $50 per barrel – at which many members of the organization can no longer balance their budgets but sizable cash reserves can keep them going – then US oil production might sag.

But this does not mean that US oil production cannot return to its December 2014 peak – and then some – once prices rise once again. A price of $100 a barrel, for example, a desirable OPEC outcome, would do wonders for production from the Bakken, even if the price climb doesn’t happen for a while.

Not going away

Despite a production slowdown in early 2015, oil in the Bakken is not going away. To date, the Bakken has yielded 1.2 billion barrels, and the US Geological Survey estimates there is another 7.4 billion barrels of recoverable oil.

To keep US oil in the ground and out of markets, OPEC has to produce and sell its commodity at bargain basement prices. One wonders if this is the wisest long-term policy for OPEC.

The boom as measured by rig count may be over for both US gas and oil but the resource is still there. The abundance of US gas and oil will continue to be a threat to OPEC at all but rock bottom prices and OPEC, countries with an economy based on one commodity, would suffer as much or more from lower prices than the US industry.