Federal, state and territory energy ministers are gathering today in Brisbane for the tenth meeting of the COAG Energy Council. In the wake of the Finkel Review, and against a backdrop of rising electricity and gas prices, they have much to discuss.

Some of the focus will certainly be on gas policy and prices. Earlier this week, the federal energy minister, Josh Frydenberg, argued that state governments should develop their onshore gas reserves to relieve pressure on the gas market.

Victoria and the Northern Territory both have bans on onshore gas development, introduced partly to protect prime farming land.

Controversially, federal Liberal MP Craig Kelly suggested on Thursday that pressure from renewable resources on energy prices meant that “people will die” this winter if they’re afraid to turn on their heating.

Yet it is gas generation, not renewables, that typically sets the price in the electricity market. As Fairfax reported yesterday, electricity prices move up and down with the gas price, almost exactly in tandem.

What’s more, the reality is that Australia has enough existing gas reserves to keep producing at current rates, including exports to the international LNG market, for at least the next 25 years. Developing extra onshore gas potentially risks harming valuable agricultural land for little gain – and certainly won’t bring energy prices down by the end of this winter.

How much gas does Australia have?

In March this year, the Australian Energy Market Operator (AEMO) published its Gas Statement of Opportunities. This reports forecasts, among other things, maximum demand and annual consumption over a 20-year period, and the ability of the eastern Australian gas market to supply this demand.

The report also highlights locations where new infrastructure or developments may be needed. Gas resources are categorised into levels, according to how difficult and expensive it will be to access and process.

It’s worth taking a moment to define what’s meant by reserves and resources, as this makes a big difference to the cost and feasibility of development.

Reserves. These are volumes of gas that are expected to be commercially viable. The category of proved and probable reserves is considered the best estimate of commercially recoverable reserves. These are often used as the basis for economic assessments, or in reports to the share market.

Resources. These are broken down into “contingent” and “prospective” resources, depending on how much is known about them. Contingent resources are one step down from proved and probable reserves, and are upgraded once any uncertainty about their development has been resolved. Prospective resources are estimates of gas volumes from reservoirs that have not been drilled. These estimates are based on much less direct evidence than the other categories and, as the name suggests, are more dubious.

So how much gas reserves and resources did this year’s Gas Statement of Opportunities report? A lot.

Gas extraction is forecast to be about 2,000 petajoules (PJ) per year for the next 20 years, to meet both domestic and export demand. The table below, which shows the reserves and resources as published in the latest Gas Statement of Opportunity, shows we are in no danger of running short any time soon.

The proved and probable reserves alone are large enough to support another two-and-a-half decades of gas production. Notably, those reserves do not include gas from the Northern Territory, onshore gas from Victoria, or the controversial Narrabri onshore gas project in New South Wales.

Prices

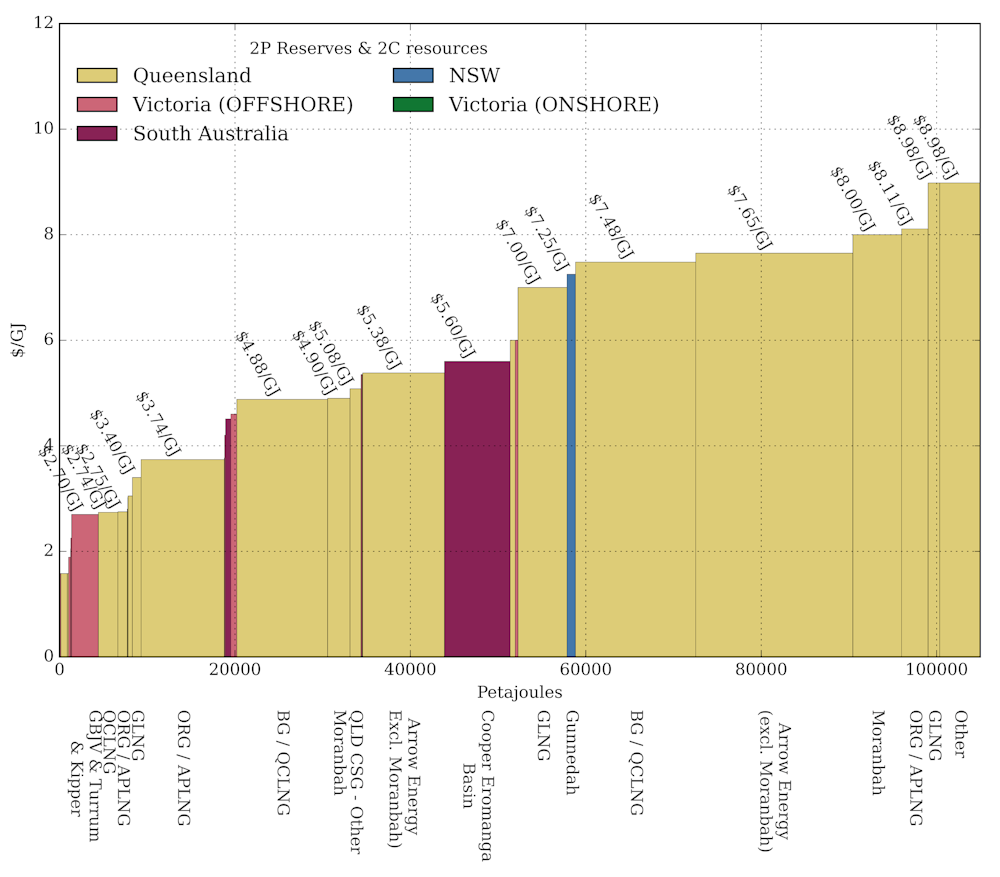

Developing new sources of gas in eastern Australian is not cheap, particularly when compared to historical prices of A$3-4 per gigajoule (GJ). The Gas Statement of Opportunities includes the development costs of proved and probable reserves and contingent resources. (Prospective resources are not published, but are assumed to be above A$10 per GJ.)

The figure below, derived from the report, shows the cost curve of development. It indicates that at the low-cost end, some proved and probable coal seam gas and conventional gas reserves have development costs around A$2 per GJ.

It also shows that about 40,000 petajoules (40 billion GJ) of gas – enough to supply 20 years of domestic and LNG export demand – is available at production costs of less than A$5.50 per GJ.

That gas prices are currently well above this points to the impact of the LNG export industry and internationally linked pricing in a sellers’ market.

As can be seen in the cost curve, Narrabri is the only onshore resource in NSW and Victoria that scores above the somewhat dubious prospective category. The Narrabri coal seam gas project is listed as a contingent resource, and is estimated by AEMO to cost A$7.25 per GJ to produce.

To put it another way, this gas is estimated to be more expensive to produce than 58,000PJ of other gas reserves and resources in eastern Australia.

Lifting the ban?

Given the volume of cheaper gas available offshore and in states without bans, it is unclear how lifting bans or placing additional pressure on states to develop onshore resources will have a material effect on gas prices.

This sentiment was reflected by the NSW energy minister, Don Harwin, who recently pointed out that “the idea that NSW’s gas sector was supposed to save the nation from the way the LNG sector grew is curious”.

Given the availability of other reserves, the potential impacts on agricultural land and the need to dramatically reduce our emissions, the expansion of the onshore gas sector is indeed a curious idea.