A recent article in the Wall Street Journal (WSJ) reported:

The U.S. is overtaking Russia as the world’s largest producer of oil and natural gas, a startling shift that is reshaping markets and eroding the clout of traditional energy-rich nations.

There are many recent similar claims along with others more critical of any notion of increased clout for the US. Much has been made of a technological revolution in extraction methods (non-conventional petroleum or NCP) as a source of resurgent US global power.

But these opportunities have also opened up grave concerns about safety and ecological impacts of new techniques, including horizontal drilling, new techniques of hydraulic fracturing (‘fracking’), heavy oil from Canadian tar sands and deep ocean drilling (blithely regarded as safe before BP’s Deep Horizon catastrophe of April 2010).

Clearly, there are major concerns about under-regulation, strongly expressed in the “golden rules” of the IEA itself.

And the NCP boom is conditional on a high international price for crude oil that still exceeds its year-average 2008 peak of US$100/barrel. This price is maintained despite expanded US production, the demand-depressing effects of global economic stagnation and (welcome) improvements in US end-use vehicle fuel efficiency standards in place for around five years.

Given space constraints, rather than on crude oil, the focus of the present comment is mainly on natural gas, conventional and non-conventional. As the IEA points out, the importance of gas is rapidly growing internationally (see Figure 1). The IEA also notes the multiple forms of non-conventional gas.

Longer run petroleum production trends

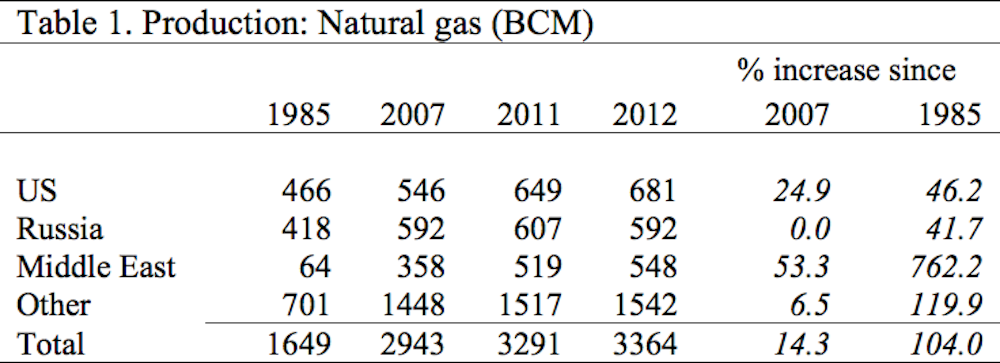

Expansion in oil and especially in gas is widely distributed internationally. According to annual data published by BP, the production level of Middle East as a whole (including Iran) has increased from only 15 BCM (billion cubic metres) in 1985 to 358 BCM in 2007 and as much as 548 BCM in 2012, a comparable level with that of the US and Russia.

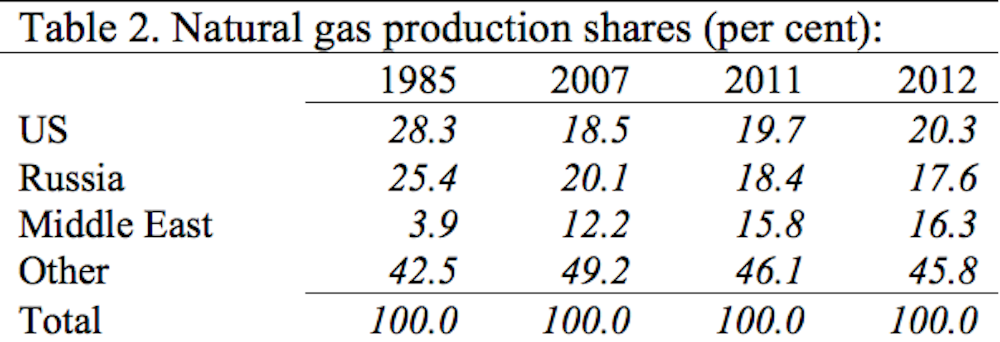

The Middle East’s share of global gas production has expanded from 4% to 16% over the same period, due mainly to activity in Qatar (exported) and Iran (mainly consumed domestically but with major exported potential hitherto thwarted by US policy) (see Tables 1 & 2).

The WSJ piece fails to capture this major trend in global gas markets.

Growth in production of oil and gas combined has not been in the US or Russia but in the Middle East and ‘other’ categories (see Figure 2).

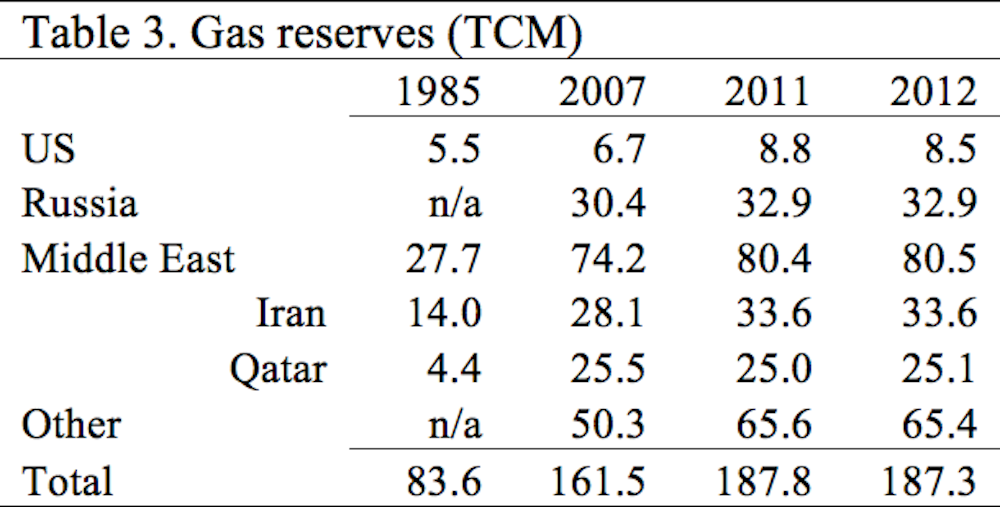

Another key indicator is reserves of gas, where Russia, followed by Iran, remain clear leaders (see Table 3).

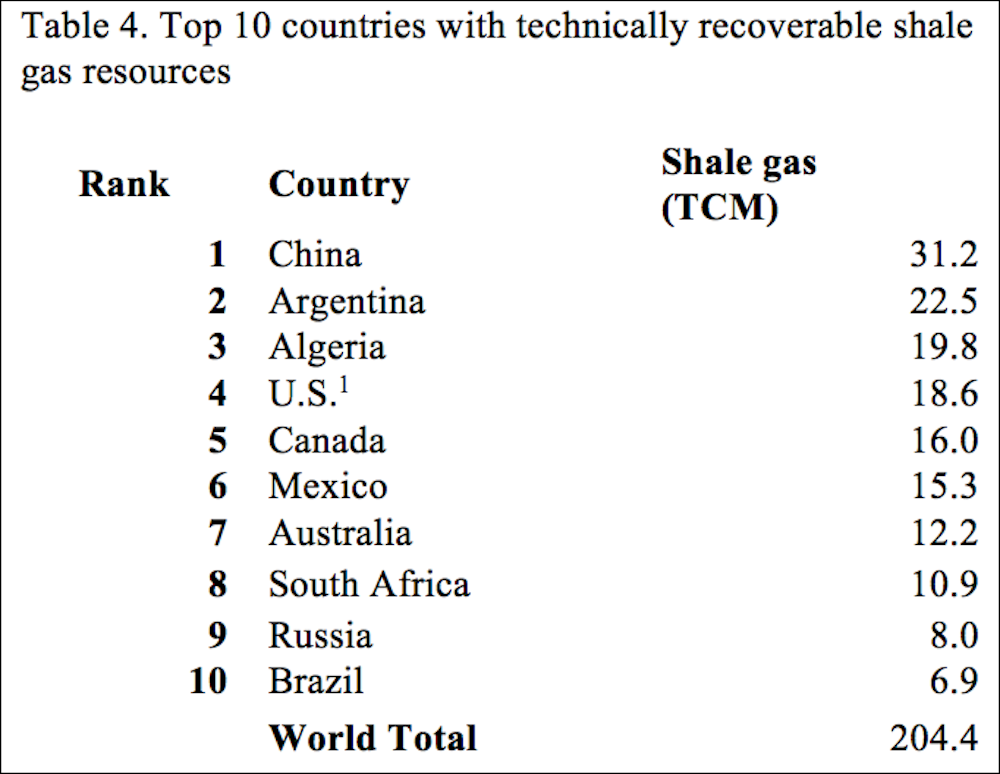

Data from the US Department of Energy’s Energy Information Administration indicates the international distribution of shale gas (see Table 4).

Iran (hitherto a pariah-state for the US) is the largest single holder of conventional oil and gas combined, despite its export prospects being thwarted by existing economic sanctions.

Political Economy

European gas prices ($15/GJ) far exceed those in the US ($3-6/GJ), but a lack of relevant processing and transport infrastructure will for some years prevent expanded US gas production for that market.

Iran’s and Russia’s ability to form a gas-export cartel is limited by a sustained global shift to non-conventional gas in the EU, China, as well as the US.

Substantial net revenue from oil and gas production also depends on low costs of production. These low extraction costs continue to exist in the Middle East, whereas viability of high cost shale oil production in the US still depends significantly on the same continued high oil prices that augment the revenue flows to the ruling elites of Middle East ‘rentier states’.

As in Saudi Arabia domestically and its intervention in support of the ruling elite in Bahrain (2011-12) oil-rich regimes have sought to ‘buy off’ (co-opt) or otherwise resist potentially restive subject populations open to political mobilisation in a renewed ‘Arab Awakening’.

The latter development has put into serious question dubious posited relationships between oil prices and Middle East ‘stability’ and democratisation.

Ecological impacts and mitigating climate change

One inadvertent but desirable effect of low gas prices and the expansion of production in the US has been to reduce its domestic CO2 emissions. The mechanism has been displacement of dirty and CO2 emissions-intensive coal – though some displaced coal is being diverted to the EU, where its low price is inhibiting CO2 abatement there. There remain some concerns about ‘fugitive’ methane as a potent greenhouse gas from NCP development.

Low prices for US gas also raise the possibility of substituting LNG or CNG for (imported) diesel fuel in heavy vehicles.

Geopolitics: rising global multipolarity and US relative decline

The US is trying to contain potential regional rivals such as oil and gas-dependent China, as well as oil and gas-rich Iran and Russia. But policies that seek to reverse a multipolarising trend in global politics can be self-defeating for an over-extended US.

If the US strategy were about promoting peace in the Asia-Pacific it would be acting to ease concerns about energy supplies available to economies in the region. It would not be seeking (as it currently is) to use these regional rivalries in a destabilising way to ‘balance’ against and ‘contain’ China.

Several foreign policy realists, including Patrick Porter, have argued that the US should instead adopt a more cooperative and inclusive grand strategy in key regions of a multipolarising world. The US could implement such an approach (in part) by promoting climate-friendly energy security policies internationally.

These might include: international transfer of new extractive technologies to the extent these allow safe and ecologically sound access to indigenous sources of non-conventional gas; and a rapprochement with Iran to achieve multiple mutual benefits, not least enhanced Iranian gas exports to coal-dependent India and China, pipelined or as LNG, thereby assisting in the global CO2 mitigation effort.

Implications of NCP are broad-ranging, complex and uncertain. But the technical revolution in NCP, internationally and in the US, is not a particular source of comfort to advocates of a still entrenched but over-extended and unsustainable US global hegemonism.