Latest economic news shows some promising signs for the Australian economy. However, the new government’s first budget next Tuesday is a big unknown.

The unemployment rate fell to 5.8% in March while full time employment fell by 22,000 and the participation rate edged down to 64.72%. Monthly job vacancies remained strong, only 1% below the long-run average.

Core inflation lies a little above the middle of the RBA’s target band of 2-3%. The Australian dollar has held up during the past month, now valued at 93 US cents. Asset markets, in particular housing, remain buoyant. Domestic consumption and production indicators are continuing on their modest upward trend.

Internationally, the clouds appear to be lifting ever so slightly. US economic data is improving and the US Federal Reserve Board announced a further reduction of its asset purchasing program. Several European crisis countries, foremost Greece, are finally showing signs of rebounding. In particular, their increased access to international credit markets at favourable conditions has surprised many analysts. China’s growth is slowing, and the possibility of a credit crunch remains real, but a growth rate of 7% is considered by many to be a lower bound.

The big unknown for Australia is the forthcoming federal government budget. It will likely be contractionary for the economy overall as the Coalition government seeks to reduce spending in a long-term effort at balancing the budget. Moreover, there is much speculation about the distributive implications of the budget. If the budget turns out to be tight and regressive, it will reduce aggregate demand and increase the likelihood that interest rates remain low.

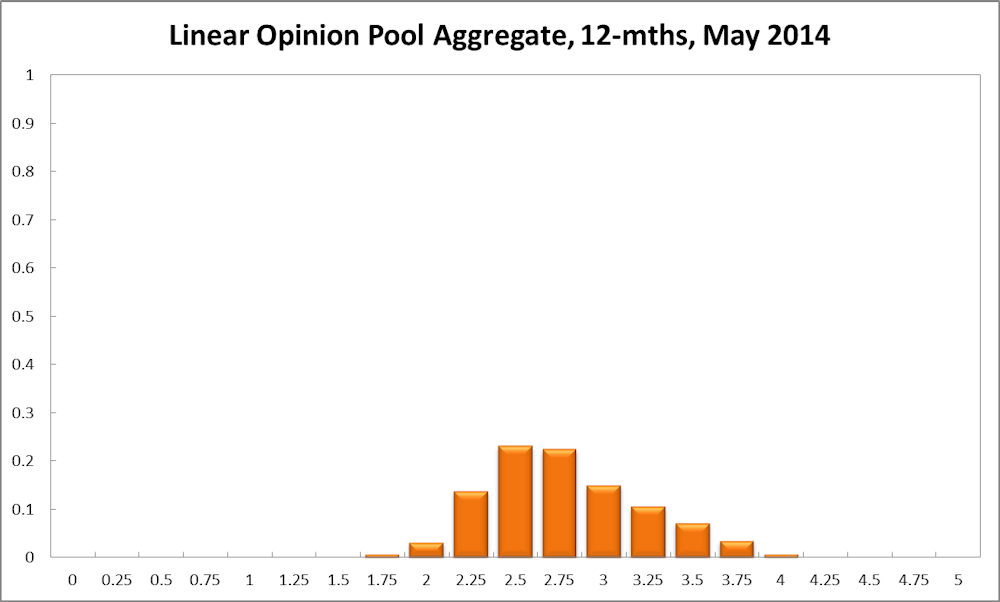

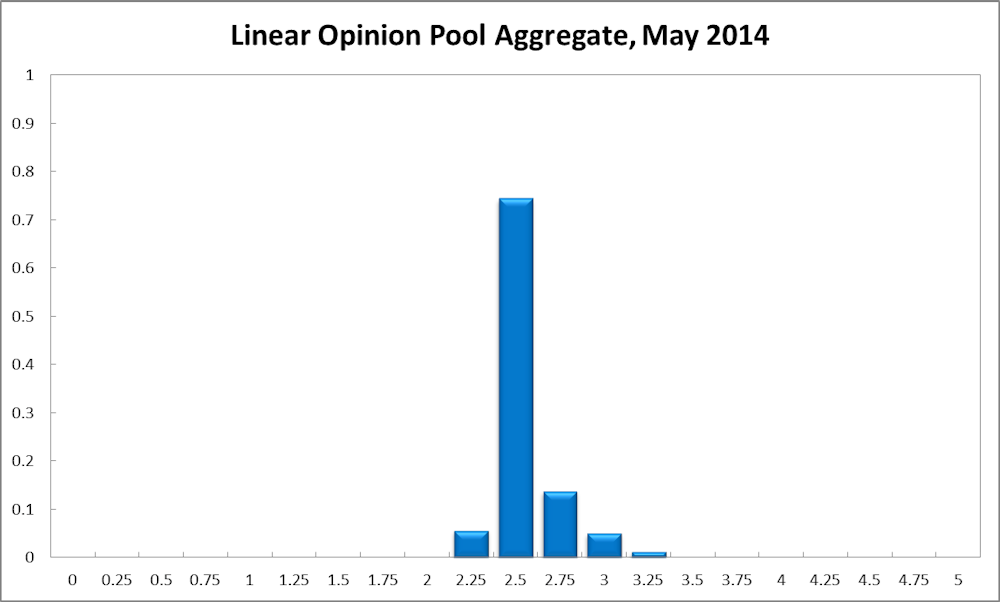

The Centre for Applied Macroeconomic Analysis (CAMA) Shadow Board is 74% confident that the cash rate should remain steady at 2.5%, strengthening slightly from a confidence rating of 71% in April. The probability attached to a required rate cut equals 6% - up from 4% in April - while the probability of a required rate hike has fallen to 20%, from 25% in April.

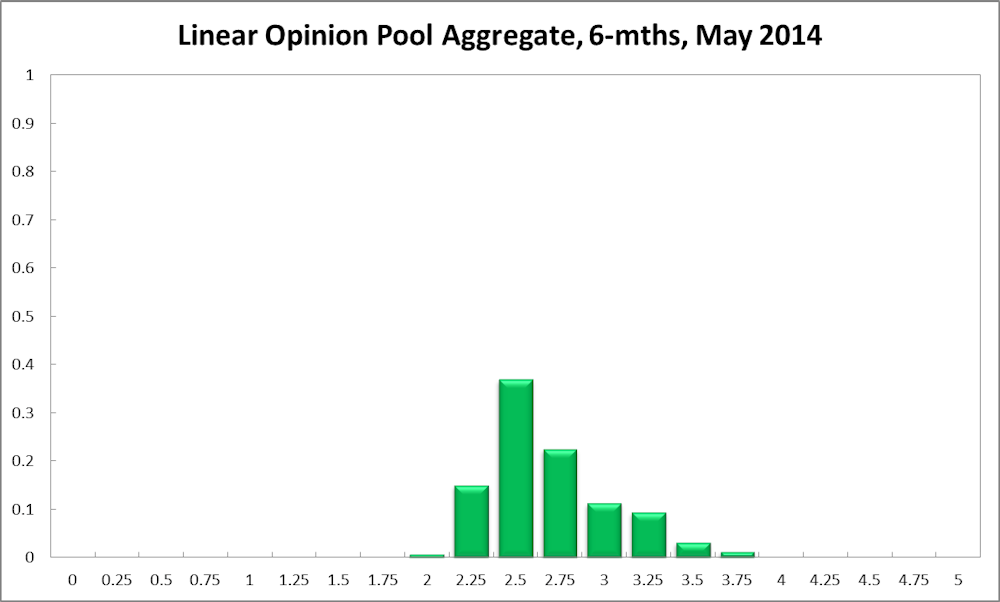

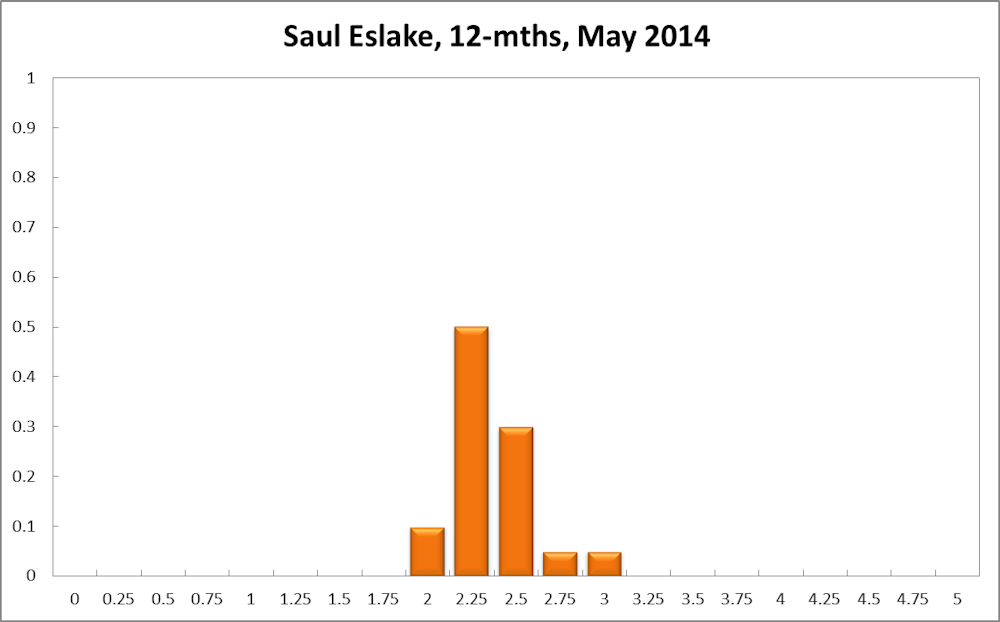

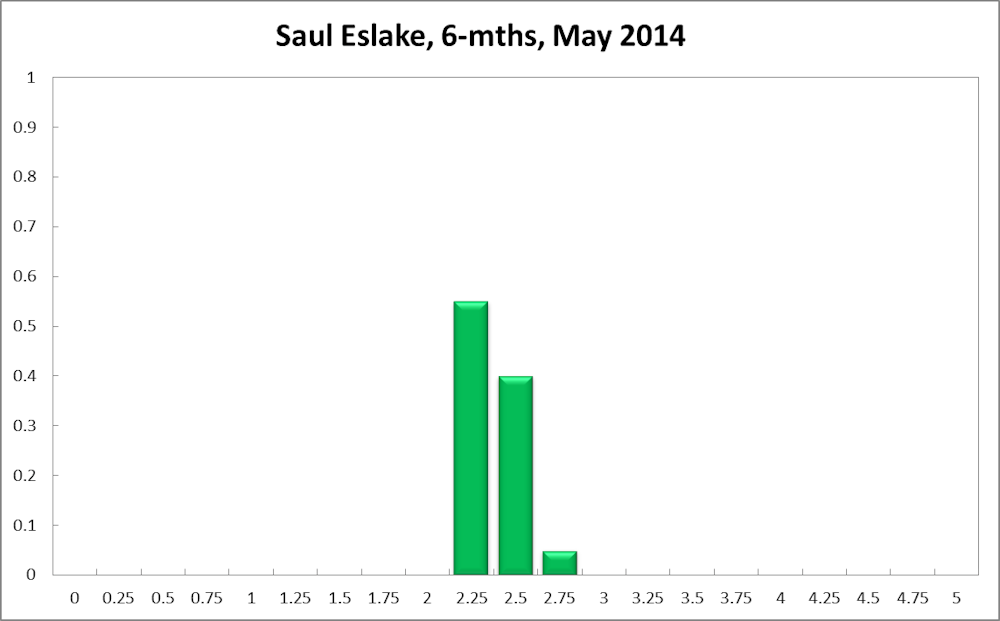

The six month probability that the cash rate should remain at 2.5% edged down to 37% (39% in April). The estimated need for an interest rate increase is virtually unchanged at 48%, while the need for a decrease has risen slightly to 16% (12% in April). A year out, the Shadow Board members’ confidence in a required cash rate increase has dropped 8 percentage points to 59%, the need for a decrease rose to 18% (down from 14% in April), while the probability for a rate hold has increased to 23% (down from 19% in April).

Note: Mardi Dungey was unable to vote in this round.

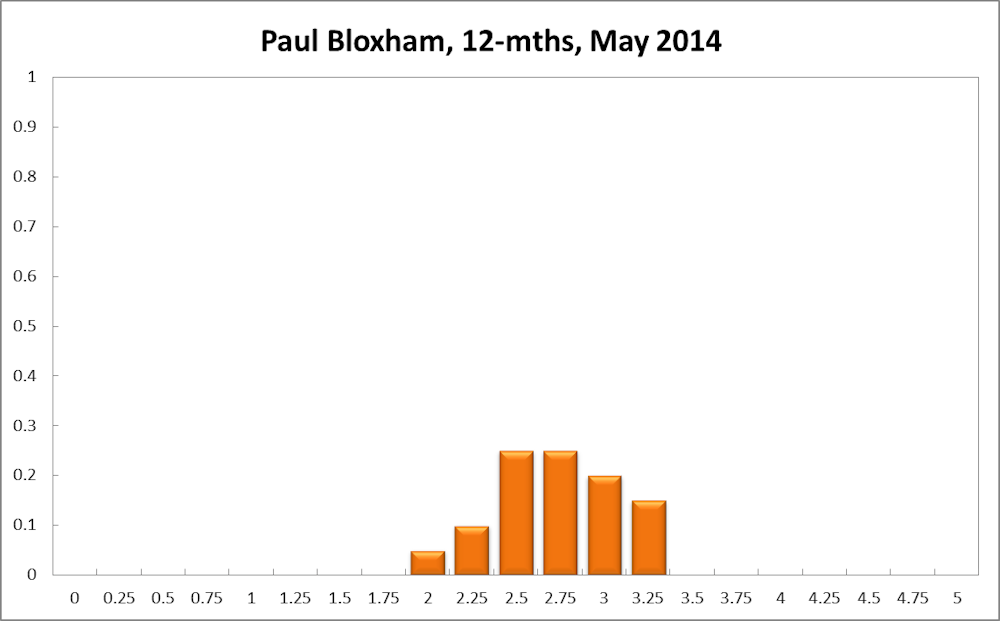

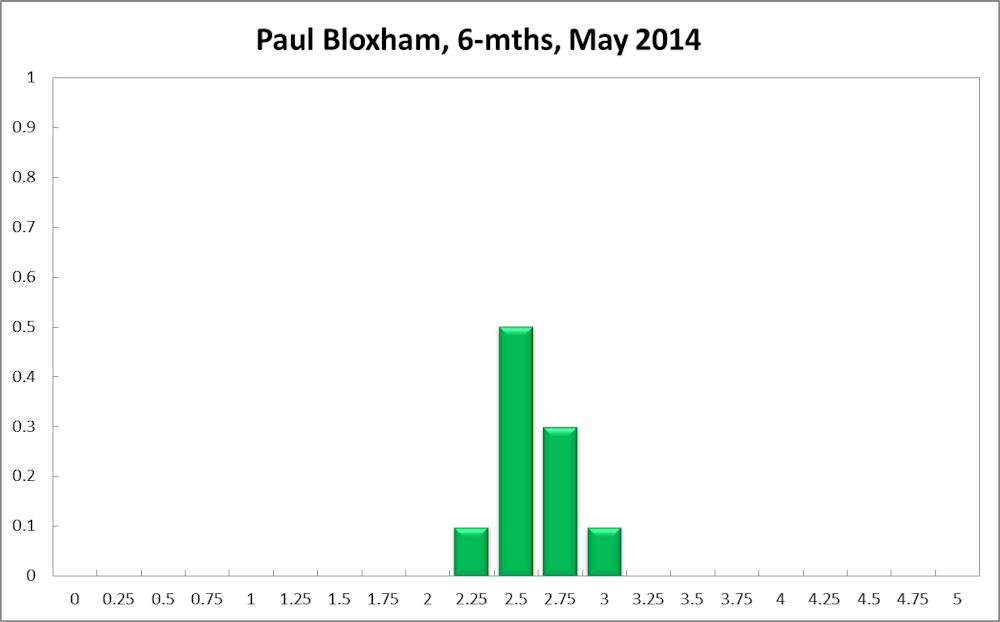

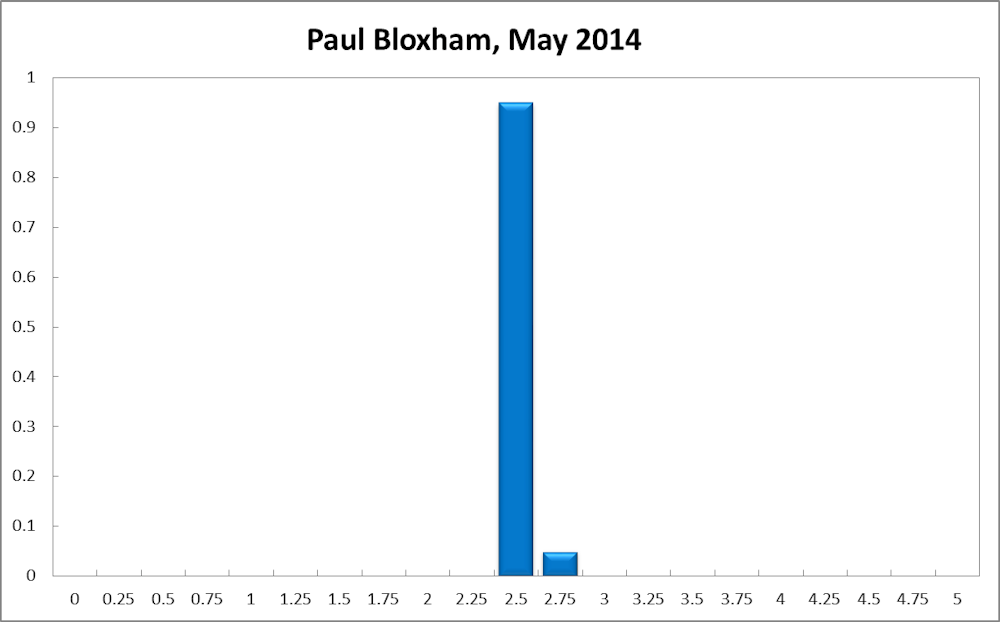

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

The Q1 CPI numbers showed that underlying inflation is just a touch above the middle of the RBA’s target band. To a large degree, this vindicates previous interest rate settings, given the lags involved in the transmission of monetary policy to the economy. It also helps to support the case for the RBA to leave its interest rate setting unchanged for the moment.

However, monetary policy needs to be forward looking, and recent timely indicators continue to suggest that economic activity is lifting, led by the housing sector and largely in response to the current very stimulatory setting of the cash rate. This month also saw further evidence that the lift in activity is beginning to translate into job creation, with the unemployment rate ticking down to a four-month low.

As yet, there are limited tangible signs that businesses are considering an increase in their capital expenditure, although this tends to occur in tandem with an increase in hiring. Should the current improving trends in activity and the labour market persist, the risks to inflation should be expected to shift to the upside, at which point, the RBA would need to consider starting to move its cash rate back towards a neutral setting. A very tight budget is a downside risk to this outlook and could be a consideration for monetary policy in coming months. I recommend that the cash rate is left unchanged this month at 2.5%, but still see it as more likely than not that the cash rate will need to be higher than its current level in 12 months time.

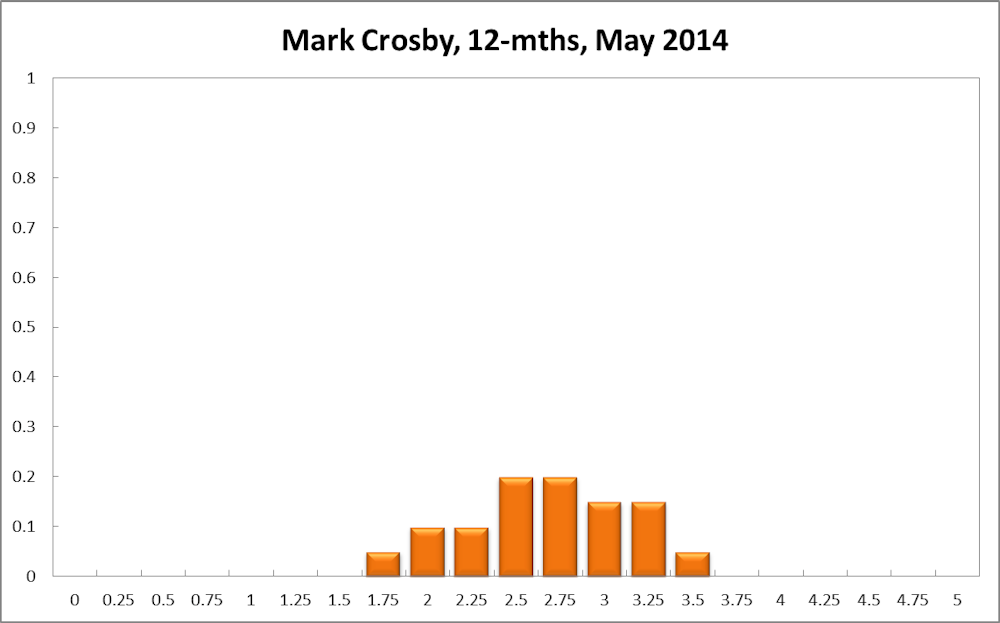

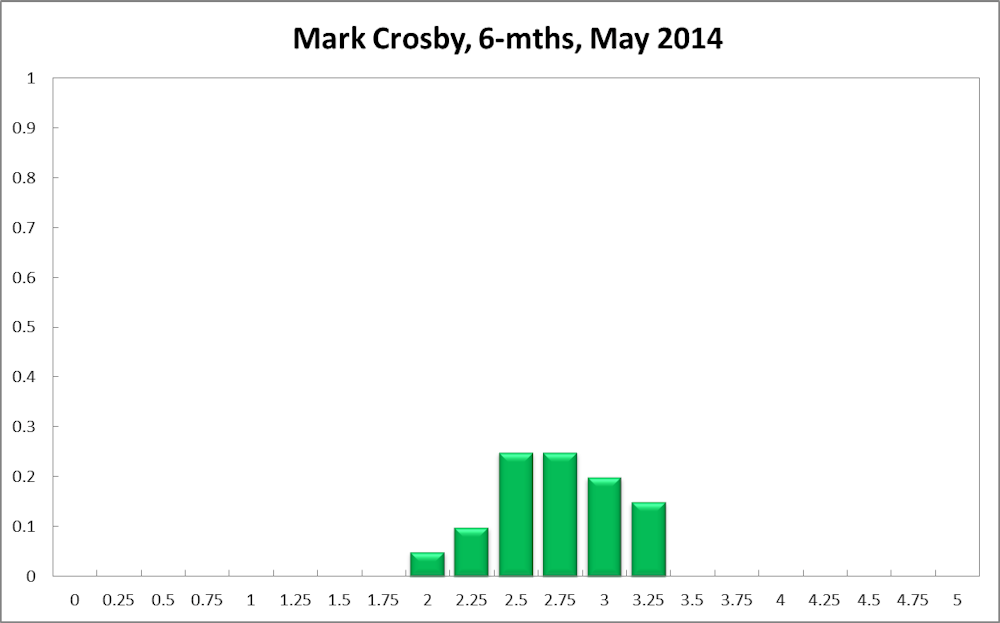

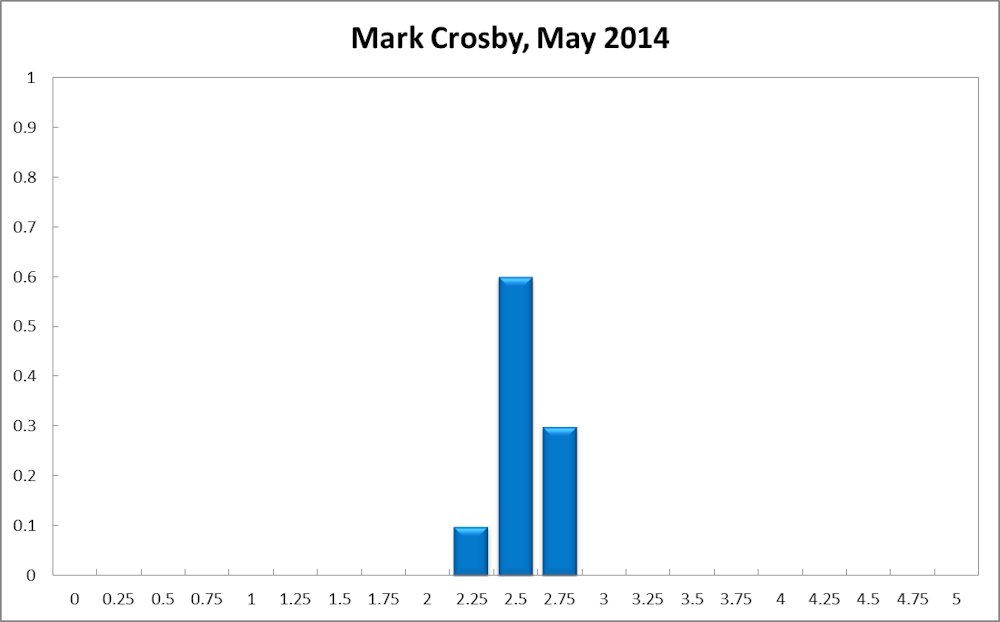

Mark Crosby, Associate Professor, Melbourne Business School:

While indicators for both the domestic economy and the international economy continue to be mixed, ongoing asset price increases should lead to a tightening bias in coming months. My expectation is that China will achieve growth around the 7% range in 2014, underpinning net exports and near trend GDP growth in Australia for the calendar year.

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

No comment.

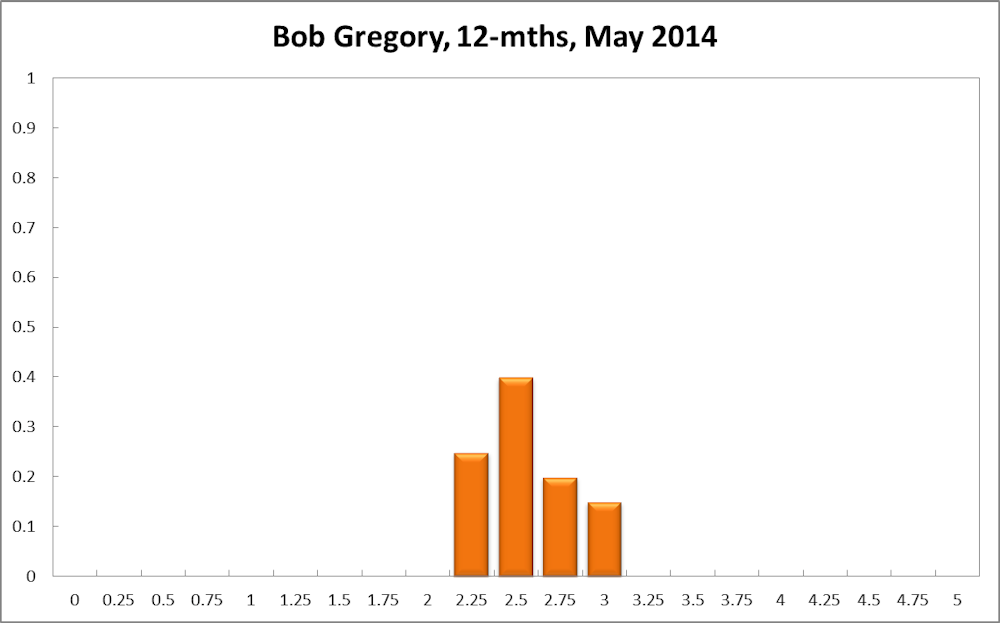

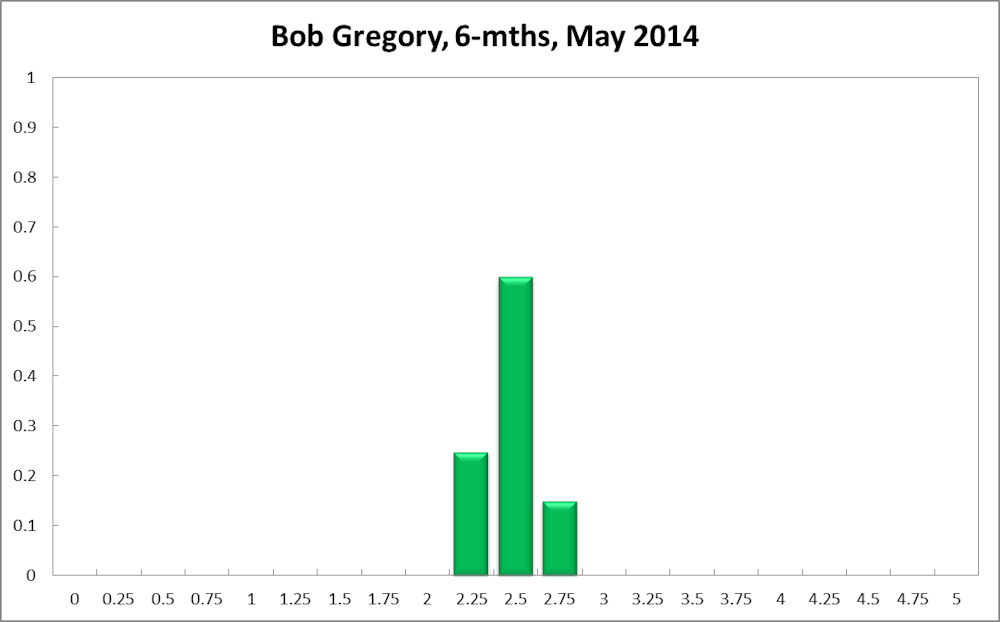

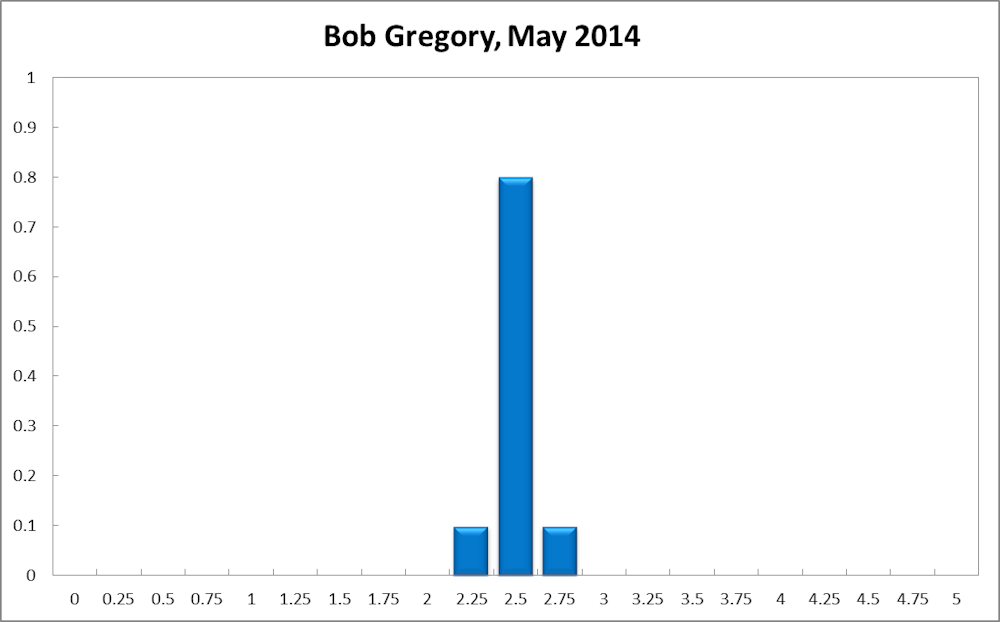

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology:

No comment.

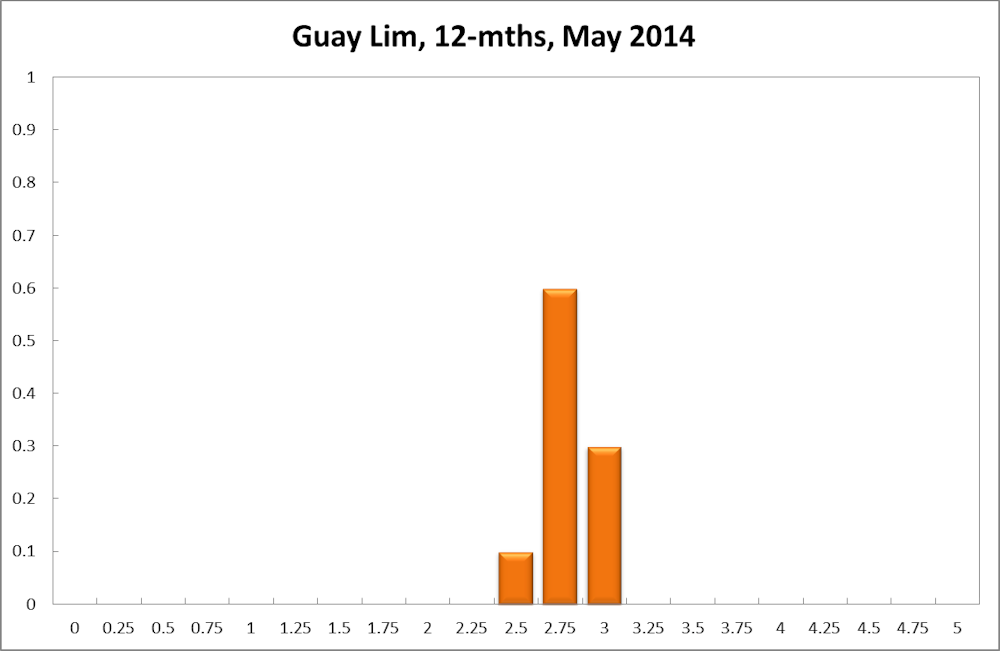

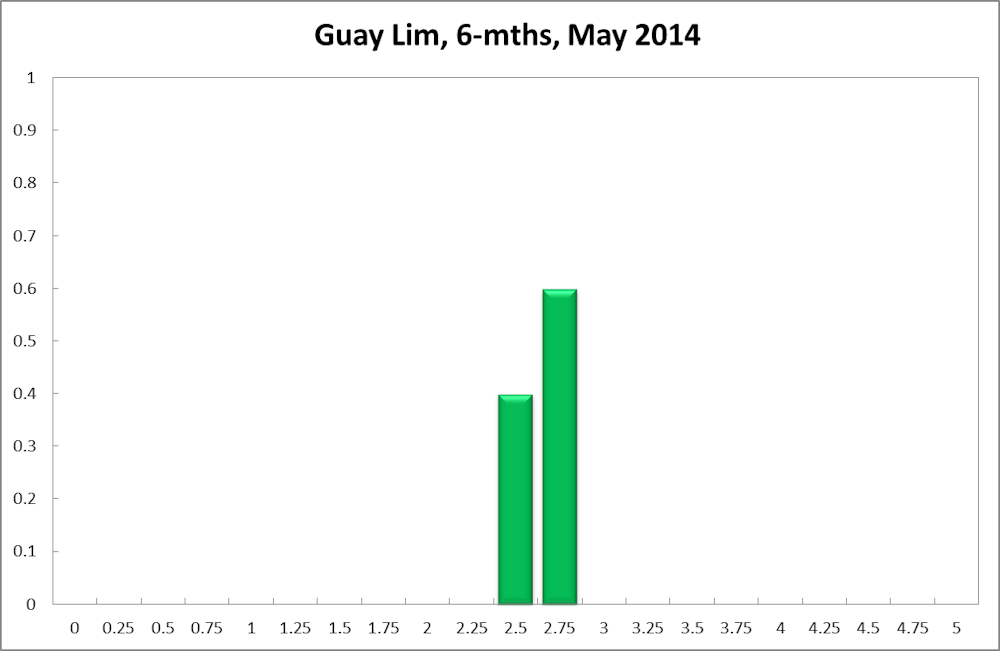

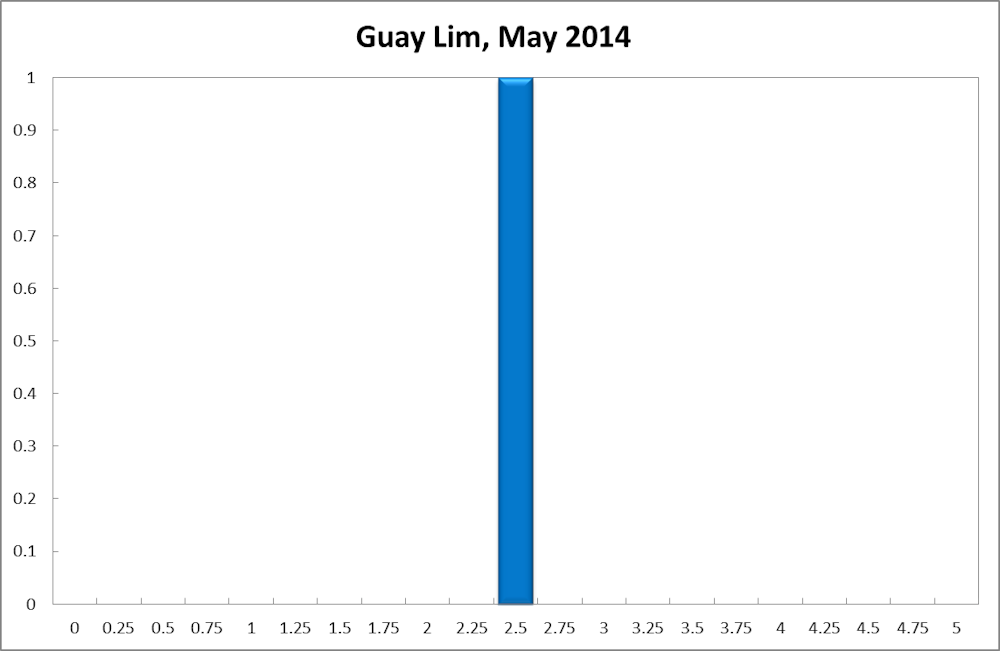

Guay Lim, Professorial Research Fellow and Deputy Director, at the Melbourne Institute of Applied Economic and Social Research, Melbourne University:

It is difficult to argue for a change in the current stance of monetary policy. Yes, leading indicators are signalling improvements, but they are not strong enough to warrant an increase in the cash rate now. On balance, I still think it would be prudent to keep the cash rate at 2.5%, for now.

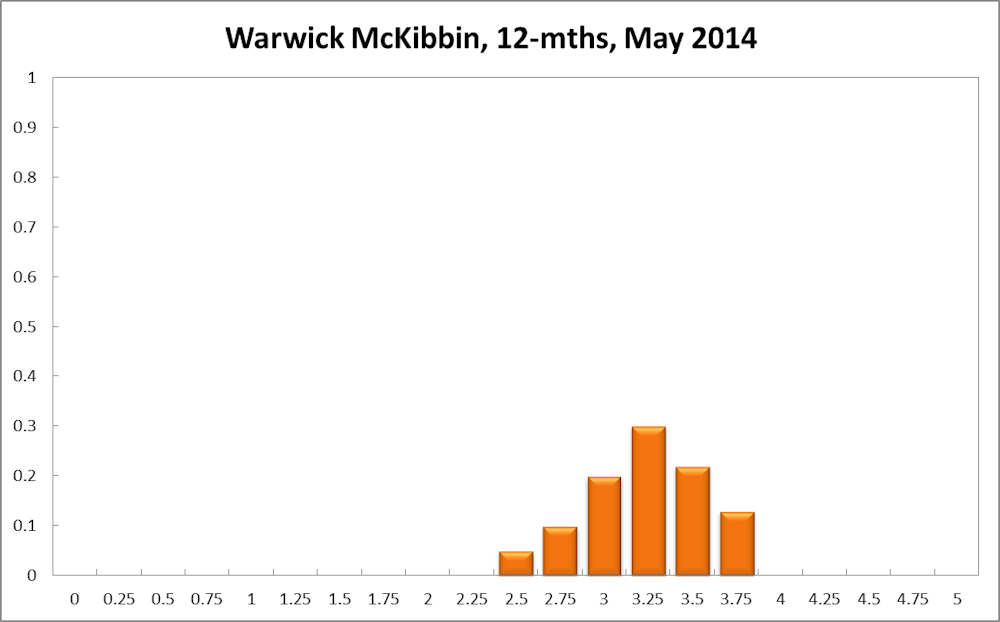

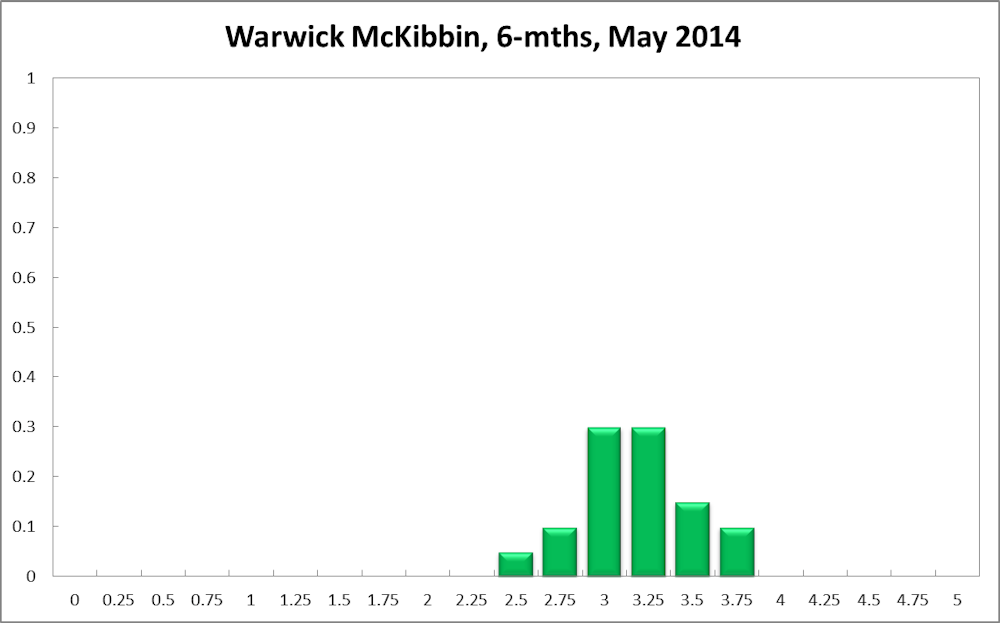

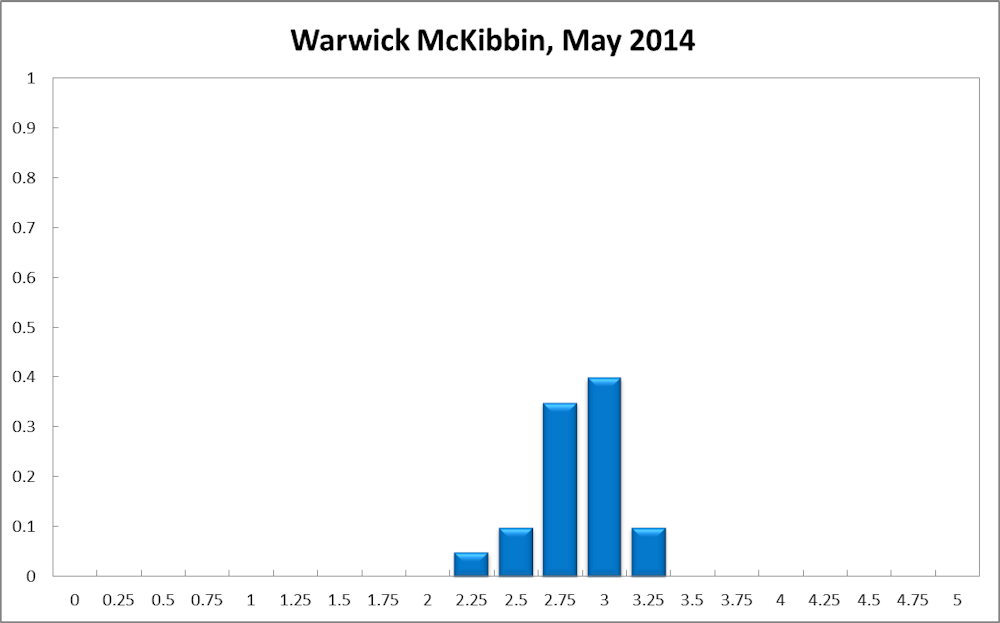

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

No comment.

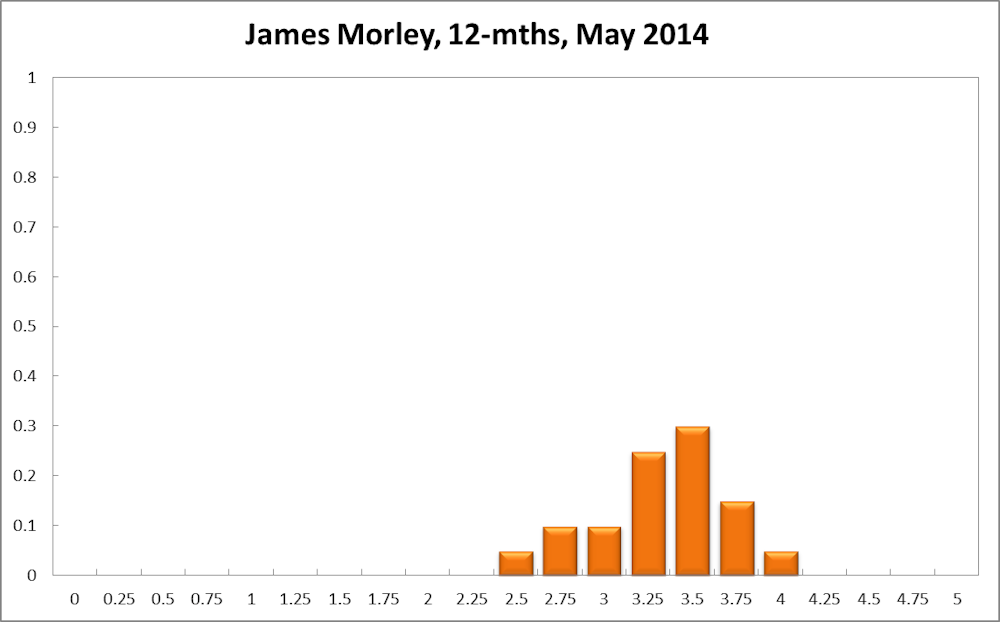

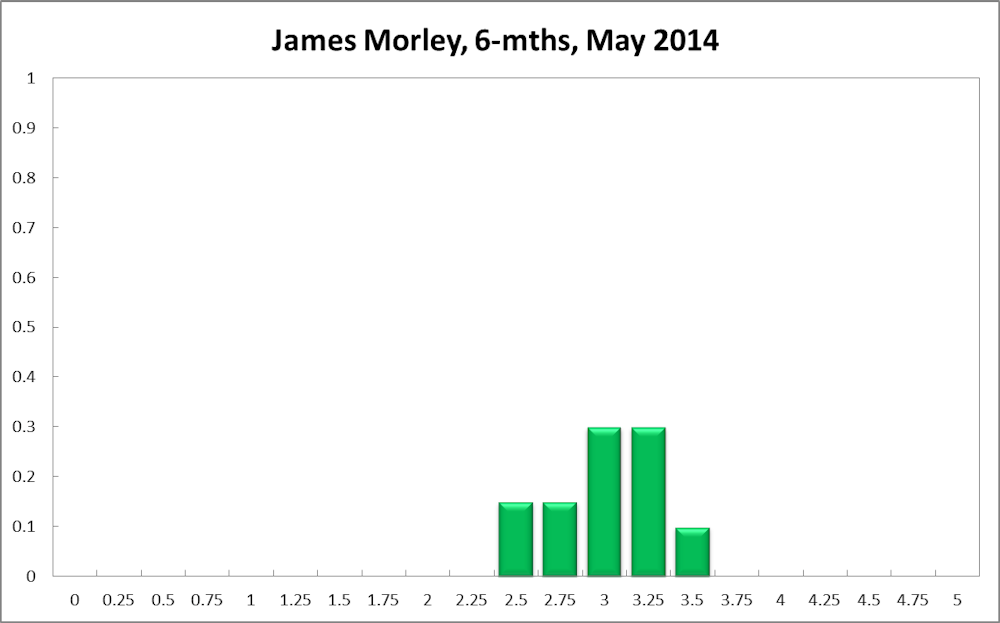

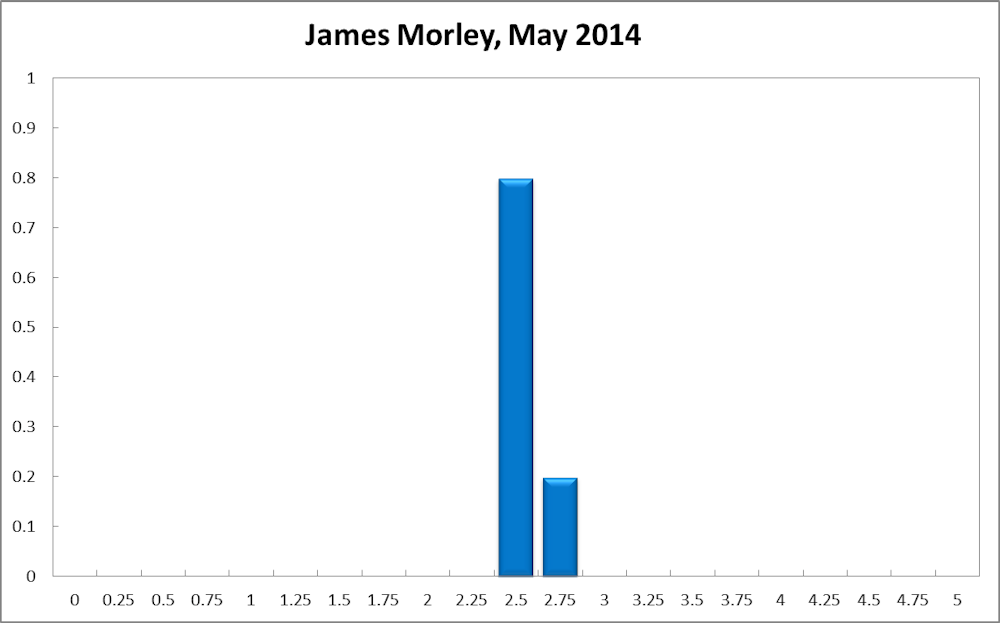

James Morley, Professor, University of New South Wales, CAMA:

Inflation remains stable. But the economy is fragile, especially given a likely fiscal contraction. In light of this, the RBA should keep the policy rate low for longer than previously planned, despite the risks of financial imbalances arising from interest rates remaining below more neutral levels.

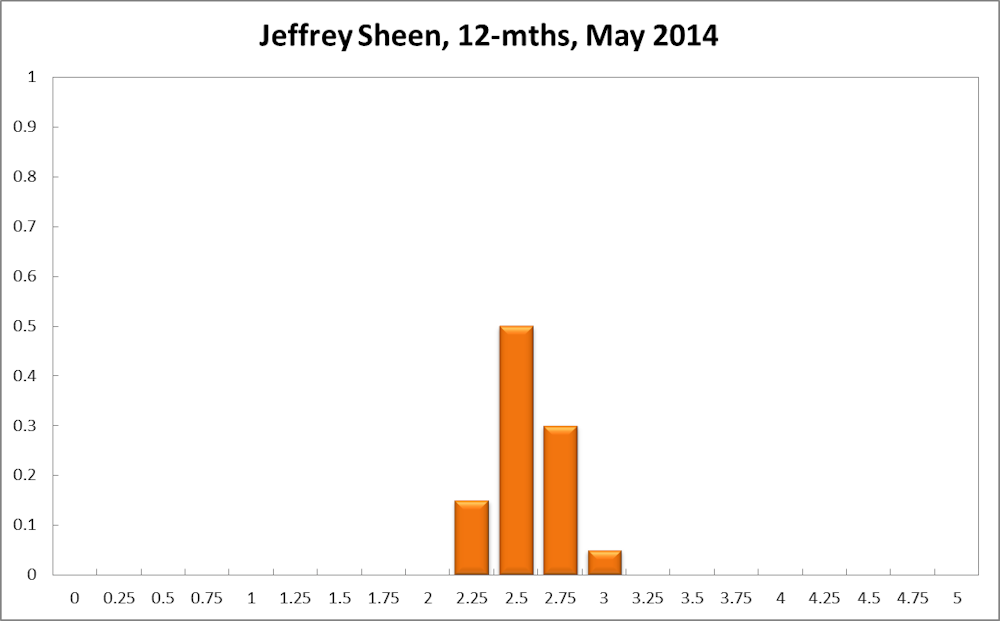

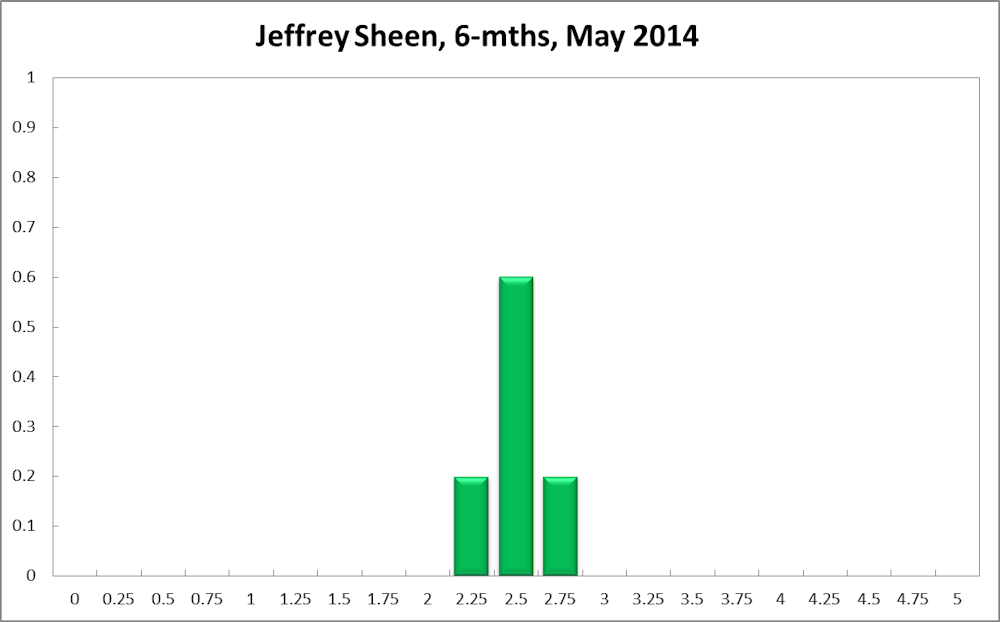

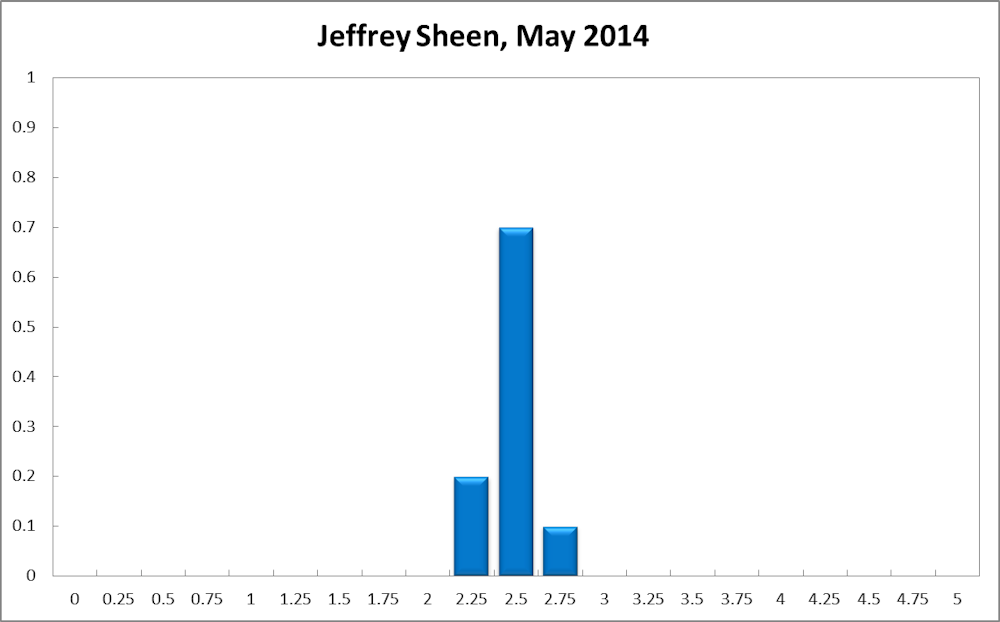

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

My recommendations for monetary policy in May 2014 have become marginally more accommodative. The government has been revealing that the federal budget is likely to significantly consolidate current and future government expenditure and tax revenues. Many of the measures will aim to address important longer run issues, but they will all have the shorter term consequence of delaying the slow recovery of the Australian economy. The global recovery, which is becoming broader and stronger, is unlikely to be enough to counteract the fiscal consolidation. Therefore, monetary policy will need to remain accommodative for somewhat longer, thus postponing its normalisation.