The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

When the Reserve Bank of Australia meets tomorrow to decide whether to change Australia’s cash rate, it will have to assess an economy that remains in limbo.

While non-mining businesses appear to strengthen and the labour market is holding up, consumer confidence has taken a hit after the Coalition government’s first budget a fortnight ago. Meanwhile, revisions to US and Chinese GDP growth are giving cause for concern.

The unemployment rate is stuck at 5.8%, with only minimal movements in full time employment, the participation rate and monthly job vacancies. There is no new information about inflation until the release of second quarter inflation measures. The Australian dollar, currently experiencing lower than average volatility, is hovering around 93 US cents. Asset markets, housing and stocks, remain buoyant.

The global economy does not present a clear picture. Recent revisions to US first quarter GDP growth reveal that the world’s largest economy shrank by a whole percentage point, considerably more than expected. Policy makers and analysts are quick to point out that this was due to the severe winter but it may offer the Federal Reserve additional wriggle room to extend its asset purchasing program. There has been no news out of China to hint at an acceleration of its economy; credit conditions and the fragile real estate market there remain a concern.

The biggest change in statistics is the sharp drop in consumer confidence, measured by the Westpac consumer sentiment index, following this month’s budget. While the budget’s overall stance was not as contractionary as feared, the public and many analysts considered it to be overly regressive.

The index fell to 92.9, down nearly seven points from April. This fall may turn out to be temporary as the disapproval of the budget subsides. However, it actually continues a downward trend, after the index hit a high of 110.63 in September 2013. As a leading indicator, this is a number to watch closely in the coming months.

What the CAMA Shadow Board believes

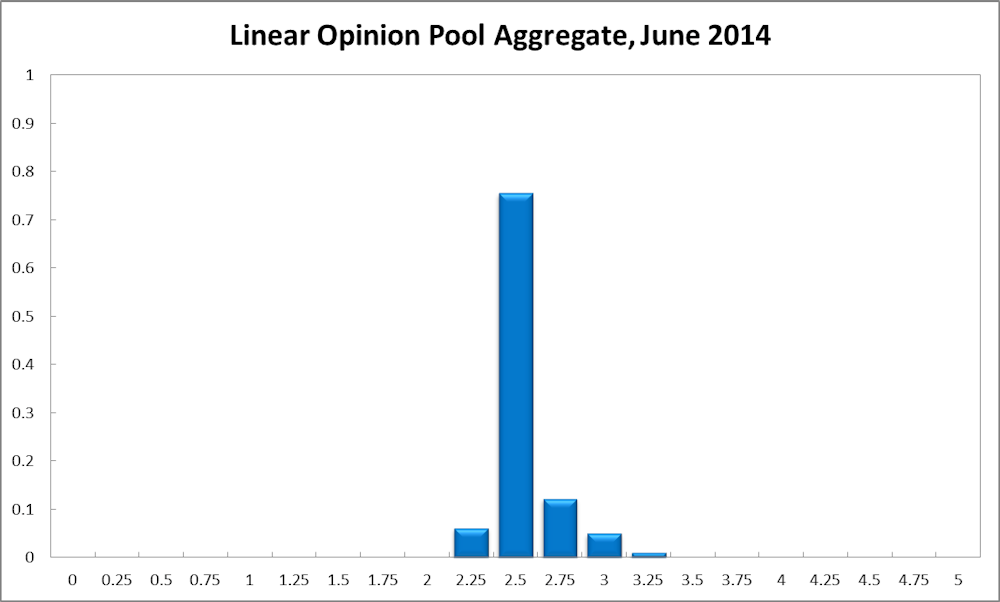

The CAMA RBA Shadow Board overwhelmingly believes the cash rate ought to remain steady at 2.5%; it is attaching a 74% probability that this is the appropriate setting.

The probability attached to a required rate cut equals 6%, unchanged from last month, while the probability of a required rate hike has fallen slightly to 20%.

The consensus to keep the cash rate at its current level of 2.5% has strengthened slightly. The Shadow Board’s confidence in keeping the cash rate steady equals 76% (74% in May 2014). The probability attached to a required rate cut remains steady at 6% while the probability of a required rate hike has slipped to 18% (20% in May).

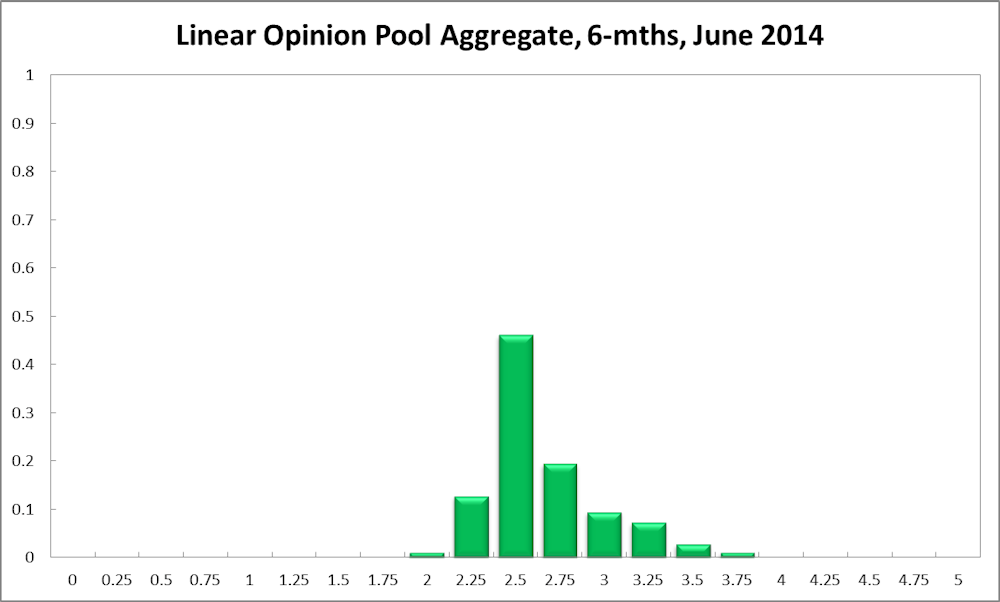

The six month probability that the cash rate should remain at 2.5% rose to 46% (39% in May). The estimated need for an interest rate increase is 40%, down eight percentage points from May, while the need for a decrease has edged down two percentage points to 14%.

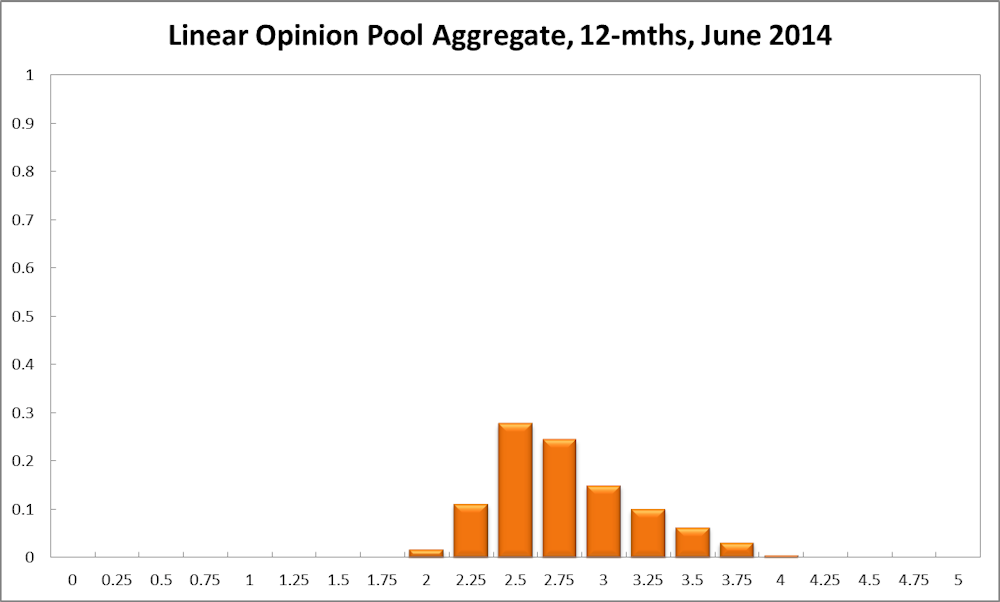

A year out, the Shadow Board members’ confidence in a required cash rate increase is unchanged at 59%, the need for a decrease fell to 13% (down from 18% in May), while the probability for a rate hold has increased to 28% (up from 23% in May).

Comments from Shadow Reserve Bank members

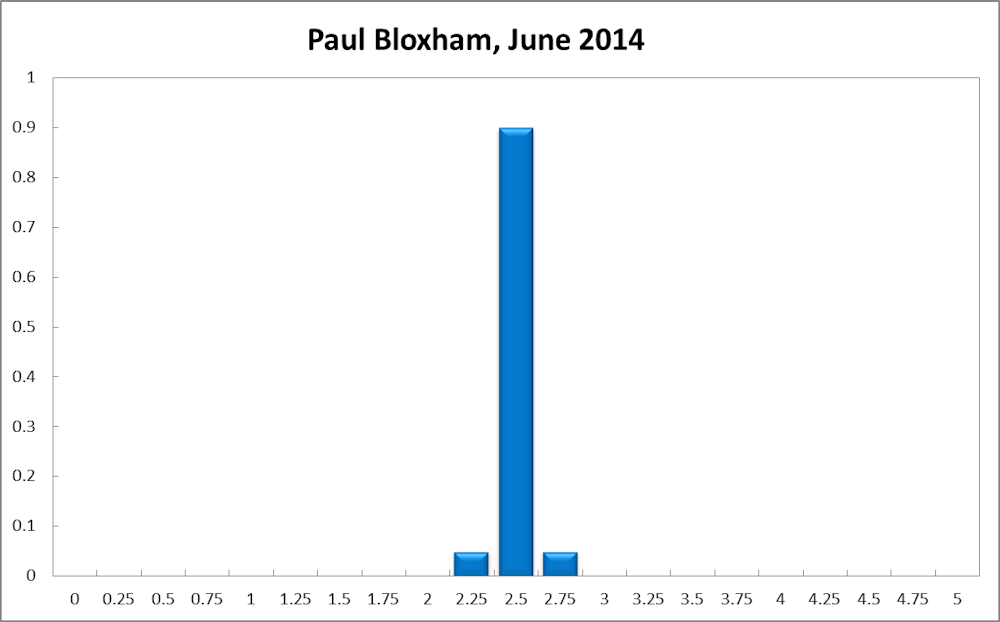

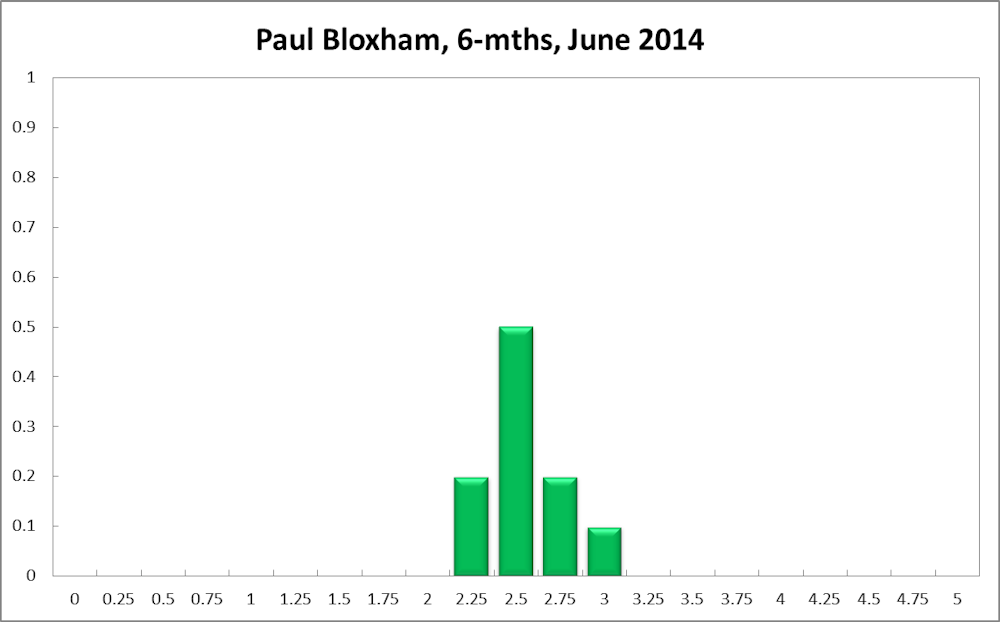

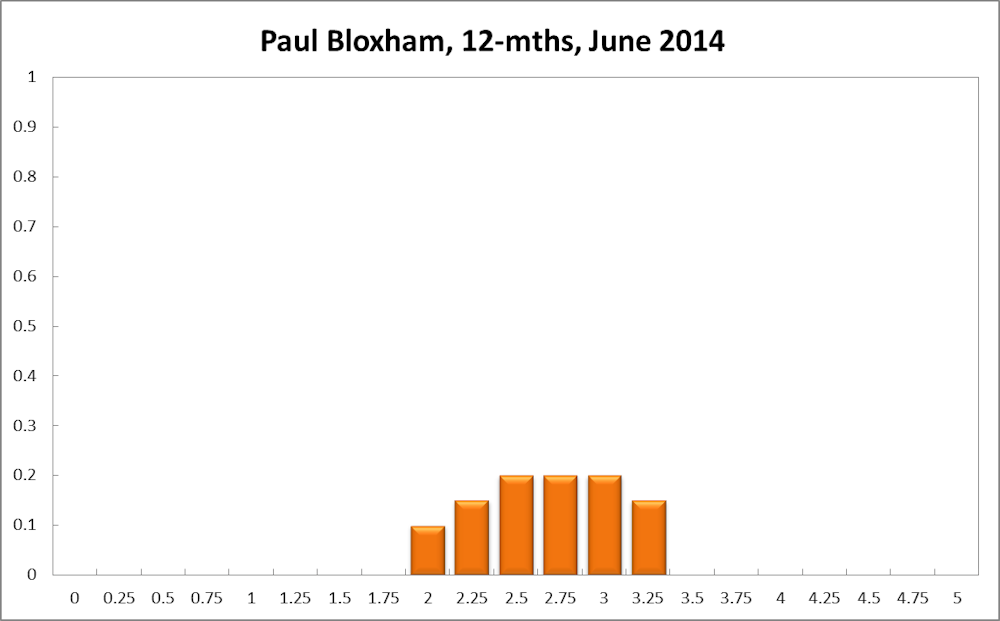

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Australia’s growth appears to be re-balancing from being led by mining investment to being driven by growth in the non-mining sectors.

Low interest rates are a key catalyst for this process, with the lift in activity mostly coming from the consumer and housing sectors. The lift in growth is also starting to feed through to an increase in hiring, with the unemployment rate having ticked down in the past couple of months.

At the same time, the current level of the unemployment rate has kept downward pressure on wages growth, which is helping to ensure that inflation remains well contained. The budget appears to have had a negative impact on consumer sentiment, although it is not yet clear if this will be temporary.

The slowdown in Chinese growth is also having an impact on Australia, particularly through lower iron prices. It will be important to continue to monitor the Chinese economy, given that growth is currently running below the Chinese authority’s target. I recommend that the cash rate is left unchanged this month.

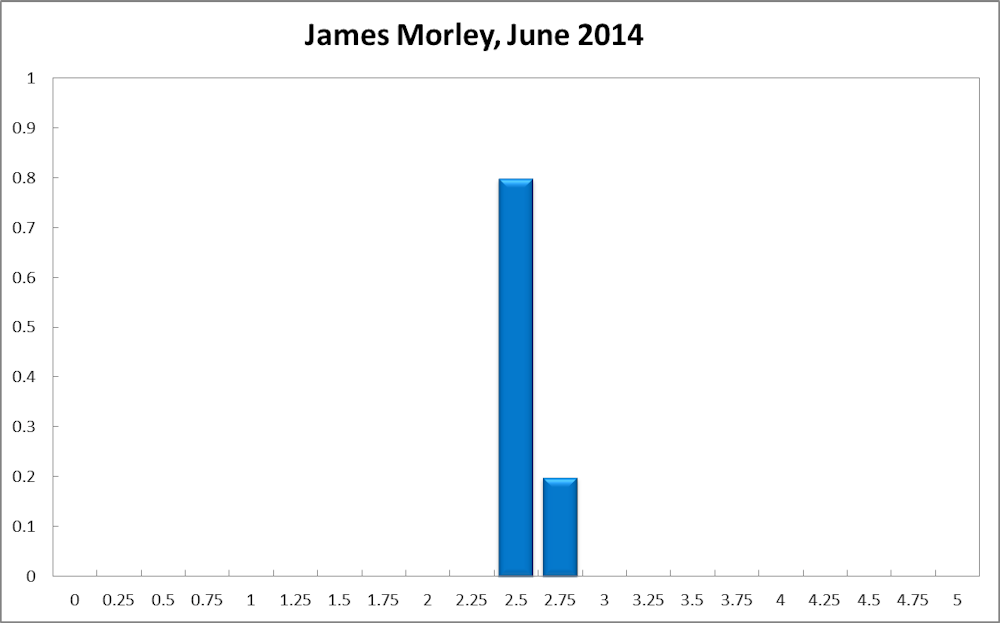

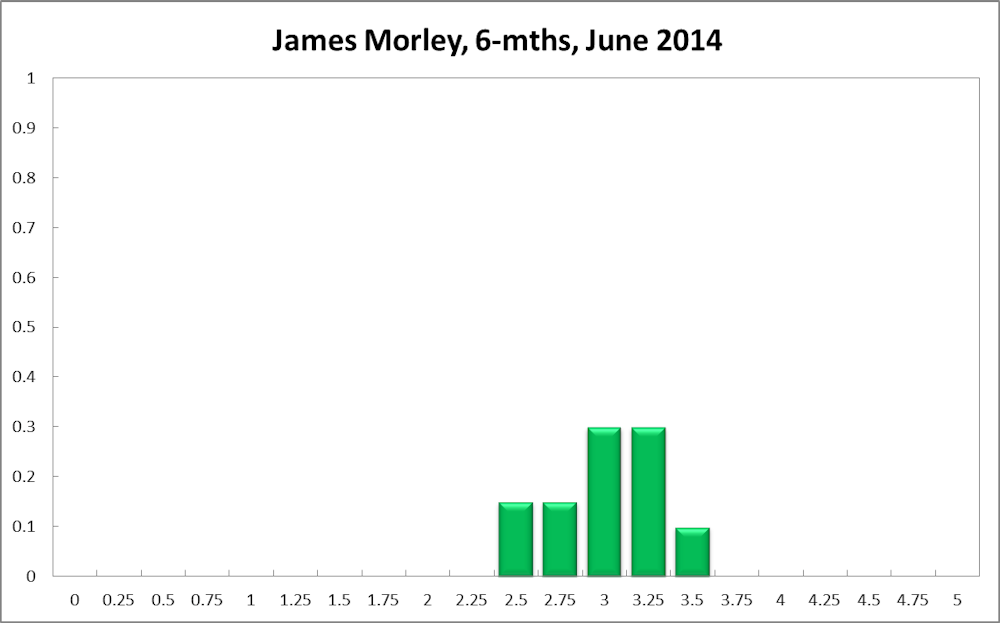

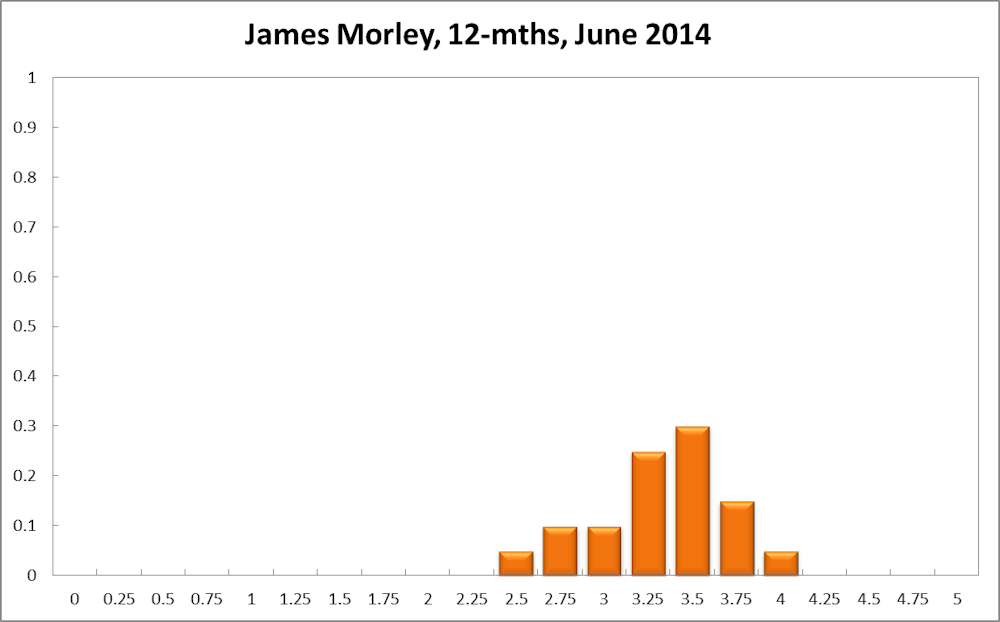

James Morley, Professor, University of New South Wales, CAMA:

The large decline in consumer confidence following the contractionary Federal budget makes it riskier for the RBA to start increasing the policy rate in the near future.

However, the RBA should monitor credit conditions and move quickly to adjust the policy rate in the event of abnormal credit growth.

Click here to view the full charts of all CAMA board members.

VERDICT FOR JUNE: rates should remain steady.