Securitisation was once lauded as an innovation designed to enhance the resilience and stability of the financial system by redistributing risk efficiently. Yet the housing bubble that burst and triggered the 2007-08 global financial crisis was fuelled by this financial mechanism.

It allows banks to repackage and sell bad debt, including loans and mortgages, to third party investors in the form of a security. At the micro-level, it drove opportunistic behaviour by banks, which created complex, opaque and lower quality financial assets. Ten years later and we could be seeing the return of this risky business.

The 2007-08 financial crisis illuminated the dark side of securitisation. When the housing bubble burst, investors suffered significant losses and lost confidence and interest in securitisation. Moreover, stringent regulatory responses to address the shortcomings in securitisation markets have rendered these transactions costly for banks to engineer. Minimal investor interest coupled with tougher regulatory requirements has had a detrimental impact on securitisation.

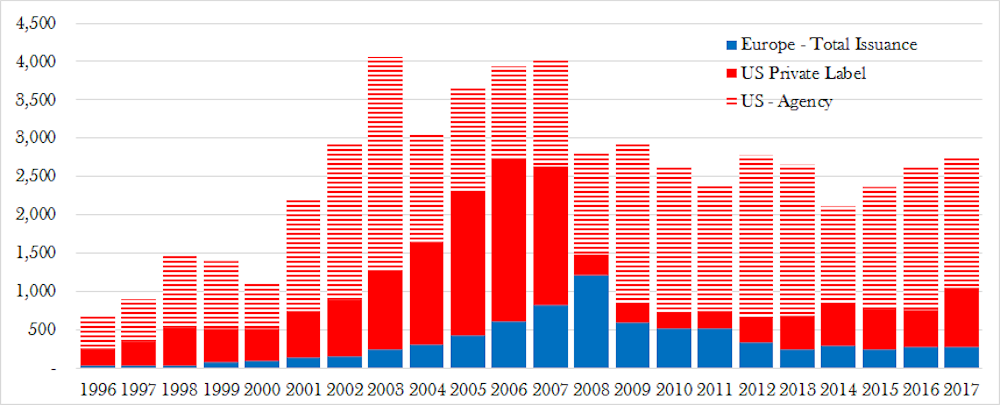

The volume of securities that were issued shrank substantially in the post-crisis period, especially in Europe. But, today, ten years after the crisis, European policymakers are eager to revive it. They say that a well-functioning securitisation market will provide significant benefits to European growth. However, there is little empirical evidence supporting this claim.

The dark side of securitisation

Securitisation modified the traditional banking business model, where banks keep loans until maturity. It is a complex financial mechanism that enables banks to sell otherwise illiquid loans to third parties. The proceeds of the sale are then used to finance additional lending and this cycle may be followed repetitively.

Since the financial crisis, a large body of work has investigated the negative effects of securitisation. There is overwhelming evidence that securitisation increases the credit risk of banks.

A number of studies have found that it increases the opportunistic behaviour of banks, too. In the pre-crisis period, banks active in securitisation rejected fewer loan applications and brokered poor quality mortgages. Riskier mortgages were more likely to be securitised and some banks even misreported the credit quality of the underlying mortgages by obscuring information from investors.

Banks also reduced their monitoring efforts of the borrowers of securitised loans. Securitisations from larger banks were granted rating favours by credit rating agencies, thereby misleading investors. Unable to assess the risk due to the complex structure of these assets and a lack of information, investors were impelled to rely on credit ratings.

Europe immune?

These undesired consequences of securitisation on bank behaviour were much less evident in the European market. European banks did not seem to have securitised low quality loans or relaxed lending standards in the same way that US banks did.

In fact, the securities market in Europe was more robust. In the post crisis period, average defaults ranged between 0.6 and 1.5%, compared with 9.3 to 18.4% for US securitisations. Nevertheless, the securitisation volume in European markets has suffered equally, if not more than, the US market.

The growing amount of European securitisations is, on the one hand, deceptive as not all the securities created are actually sold onto private investors. A large amount is retained by the issuing banks and subsequently used as collateral to secure funding from central banks such as the European Central Bank. But, on the other hand, UK banks have recently increased their issuance levels significantly relative to pre-Brexit levels.

Lessons learned

Since the crisis, European regulation has tightened significantly. In particular, it has targeted the negative effects of securitisation on bank behaviour and increased transparency in the markets. Banks must hold more capital for asset-backed securities, they must take more responsibility for their own risk and investors are now required to perform due diligence.

But, given the current market stagnation, the securitisation framework has been revised repeatedly to revive the market. After much debate, Europe’s new securitisation regulatory framework will come into effect fully on January 1 2019.

In particular, the new framework aims to promote the issuance of simple, transparent and standardised securitisations that are easy to evaluate and monitor by investors and regulators alike. For example, to be eligible, underlying assets should be “homogeneous” by type (having similar cash flow characteristics and risk) as well as maturity. The framework provides capital relief for investors who wish to hold these simple, transparent and standardised securitisations.

But there are still some shortcomings. The capital relief advantages are not applicable to large long-term institutional investors such as pension funds and insurance companies. Countries will also be given the autonomy to impose sanctions on non-compliance with the risk responsibility measures. This may potentially temper cross-border activity.

Despite these limitations, the new framework is expected to broaden investment opportunities for long-term investors. The EU hopes it will boost lending to European households and businesses by providing an extra €150 billion to the real economy. But, with a lack of evidence to support this and with the dark side of securitisation in mind, it’s important to tread carefully and learn from the lessons of the financial crisis.