{kind=link}

The government’s plan to charge up to 6% interest on HELP loans has been widely attacked as unfair. Many critics, including Shadow Education Minister Kim Carr, the Group of Eight universities, Universities Australia and HECS architect Bruce Chapman, have come out against pegging HELP loans to the bond rate, rather than CPI as it is now.

CPI versus bond rate: the difference

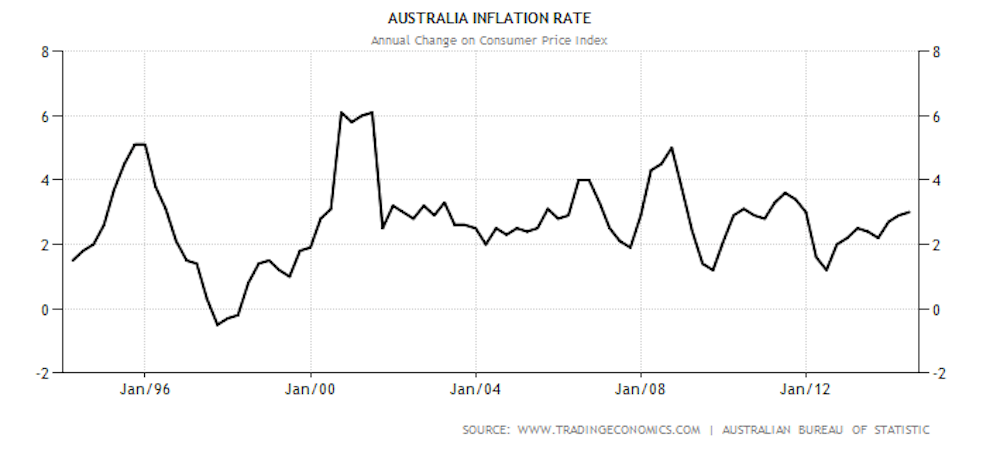

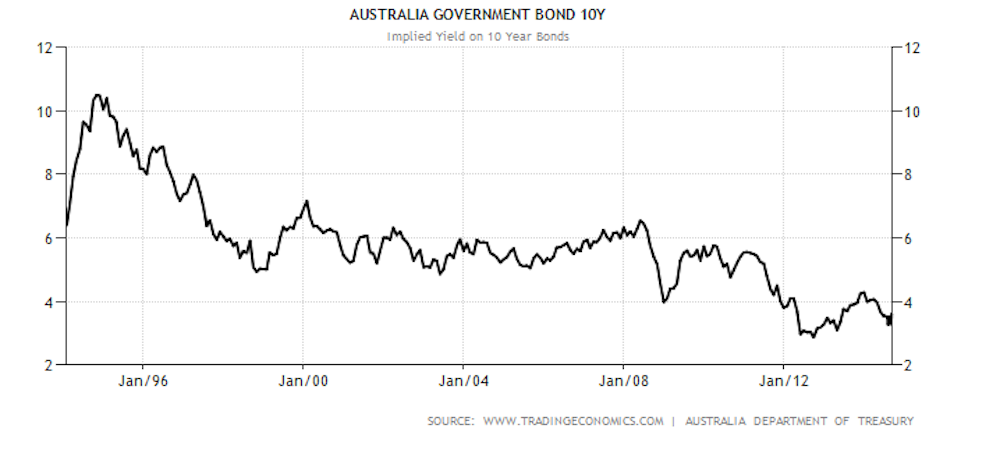

Interest charges on HELP debts currently reflect the Consumer Price Index (CPI), so students pay zero real interest after inflation is taken into account. But if charged at a long term government bond rate, as proposed by the Commission of Audit report in March, students would pay the government’s cost of borrowing.

Over the past 20 years CPI has varied from 0% to 6% (Figure 1) and the bond rate from 3% to 10% (Figure 2). The difference between them – real interest after inflation – also varies, from less than 1 to more than 5 percentage points.

Risks with a 5% bond rate

Detailed modelling by ANU economists Bruce Chapman and Timothy Higgins shows how compound interest on HELP debts at real rates of interest would hit lower income graduates harder, since they may repay over much longer periods. With an initial A$60,000 HELP loan and a bond rate averaging 5%, a high income earner may repay A$75,000 and a low income earner A$105,000.

Chapman and Higgins also looked at ways for the government to recoup its borrowing costs with less disparity between high and low earners. Chapman’s preferred option, reportedly, is a flat surcharge of say 25% added to the loan. The total debt is then indexed at CPI to maintain the same real cost for all who repay, whether quickly or slowly.

Risks with a 25% surcharge

However, depending on how large it is, a surcharge has some problems. First, it can only be applied to new HELP loans. More than A$30 billion of existing HELP debt already sits on the government’s books. So the budget savings may be less than if real interest were applied to all HELP debts, as proposed.

Second, for students a 25% surcharge adds a dollar of upfront cost to every four dollars borrowed. As a recent NTEU briefing shows, a degree priced at A$75,000 would require a A$94,000 HELP loan from the outset.

Third, with CPI there is no incentive to repay debts sooner, a concern raised by Education Minister Christopher Pyne.

Finally, Group of Eight modelling for selected degrees suggests that most graduates may end up paying more with a 25% surcharge than with a lower bond rate. The Group of Eight paper agrees with Chapman and Higgins that

a surcharge would equalise interest costs across all graduates and remove regressive aspects of a real interest rate.

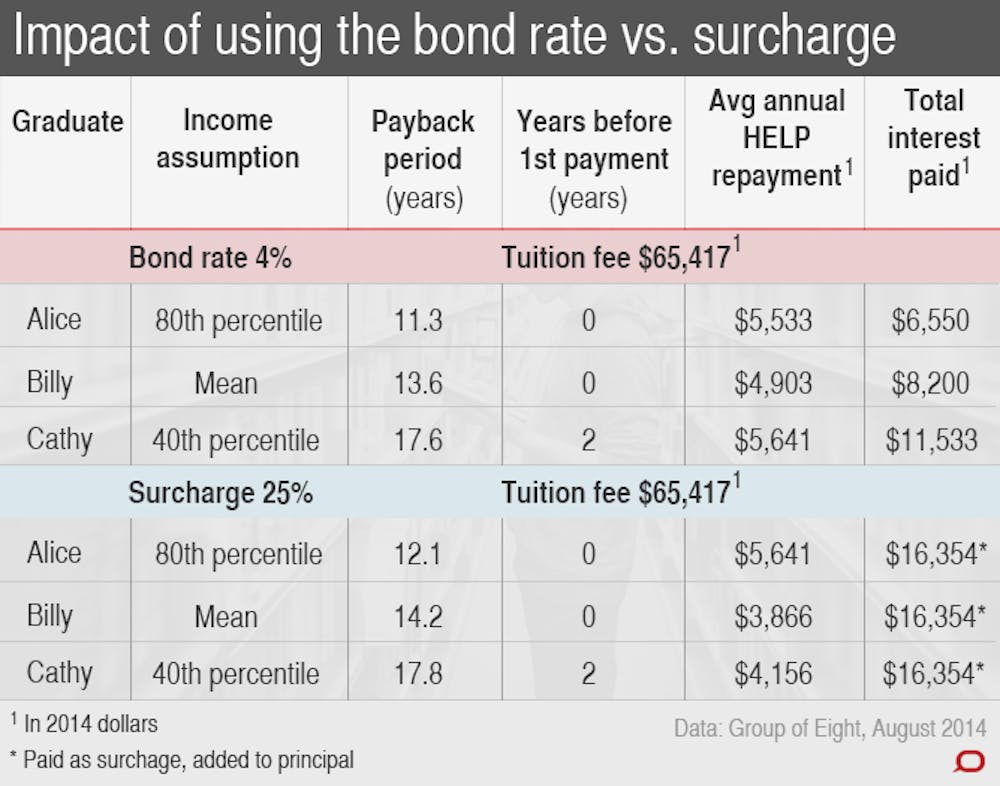

However it also shows a A$65,400 dollar law degree costing nearly A$82,000 on this basis. In the Group of Eight modelling in Table 1, high income Alice pays A$10,000 more than with a 4% bond rate, medium income Billy pays A$8000 more, and low income Cathy pays A$5000 more. A similar pattern occurs with smaller HELP debts for commerce and science graduates in the Group of Eight paper.

Different modelling, different policy?

The Group of Eight modelling of repayments on a A$65,000 degree doesn’t match that of Chapman and Higgins on a A$60,000 degree. One reason is that the Group of Eight bond rate assumption is lower, with real interest set at 1.4% a year, not 2.3%. Also its graduate income estimate is higher (for law graduates in this case, not all graduates). And it uses higher level income categories than Chapman and Higgins, who use the 30th percentile for “low” and the 75th for “high”.

Clearly, any cost recovery reform poses risks for students. Whether an upfront surcharge on HELP loans would cost them less will depend on its size, and what it replaces. Yes, it offers greater certainty. Yes, it “equalises” repayments on a given debt at different income levels. But for many, it may cost more than a moderate rate of real interest.

A compromise solution

In the government’s Senate negotiations, a good compromise would apply CPI plus 1 percentage point to all HELP debts. The savings would tap a larger pool of graduates, not just those likely to face higher fees and larger loans in the future.

At lower real interest than the cases described here, CPI plus 1% may still bridge much of the gap between the two rates. In the last 10 years CPI ranged from 1.2% to 5%, and the bond rate from 3% to 6.5%. In the last two and a half years CPI ranged from 1.2% to 3%, and the bond rate from 2.9% to 4.3%.

CPI plus 1% would also give graduates an incentive to repay HELP debts as soon as they can, not just the minimum required. The risk is notably higher repayment costs for those who don’t clear their debts in say 20 years. But at 1% the real interest risk is less than with the Group of Eight 1.4% scenarios.

If the Senate agreed to this “1% solution” the budget savings would still be substantial. This would allow more scope to minimise subsidy cuts, another savings proposal that shifts costs to students. In turn this would reduce the risk of higher tuition fees, and higher HELP debts in the first place.