To outsiders Western Australia may appear as a state with a buoyant economy riding a wave of mining and energy investment, but away from the resources sector things are tough. Over the past few weeks the WA Premier Colin Barnett has had to hold crisis meetings with farmers across the wheat belt. The impacts of the high Australian dollar, low commodity prices and poor seasons have combined to make it tougher than usual for the rural producers.

The state of agricultural business in Australia

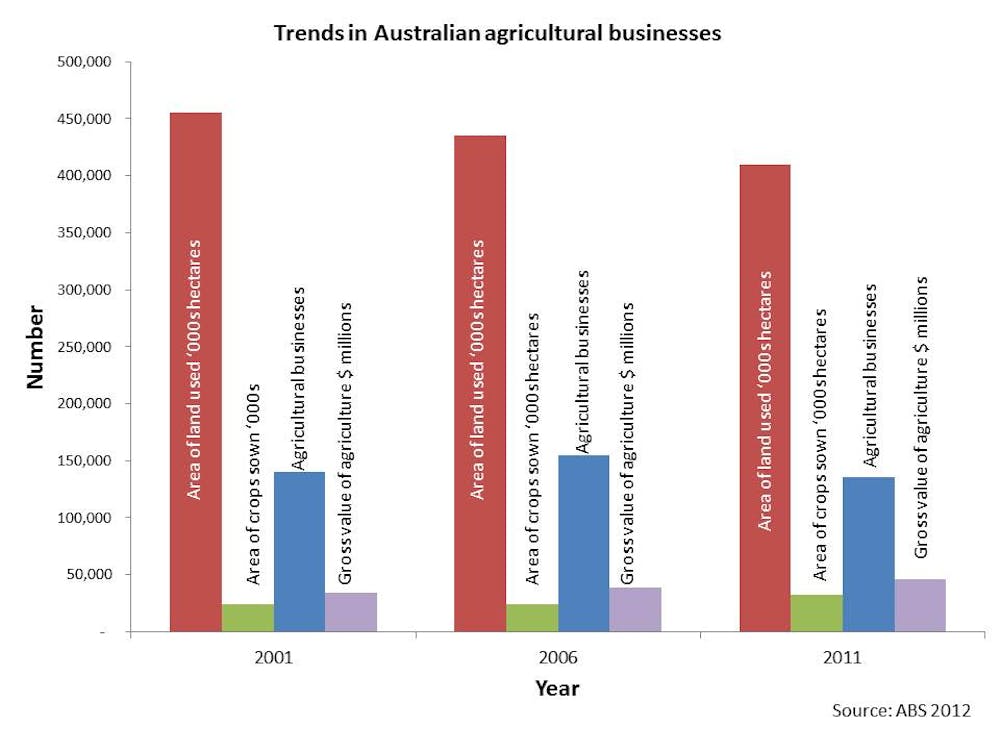

The Australian Bureau of Statistics (ABS) estimates that there are around 137,447 agricultural businesses operating across Australia. Over the past decade their numbers have decreased by about 3.5% and there has been a decline of around 10% during the same period in the amount of arable land used for farming. For example, in 2001 Australia had some 456 million hectares of land committed to farming, but by 2011 this had fallen to 410 million hectares.

Despite these falls in the number of farms and the amount of land used for farming, the overall productivity of Australia’s farmers has increased substantially. The amount of land used for crops has grown by 31% despite the reduction in overall land used, and the gross value added from agriculture has risen by about 34% since 2001. These trends can be illustrated in the following graph.

This suggests a trend in which the number of farms operating across Australia has shrunk but those that remain have become more productive. These trends are likely to continue well into the future, but there are some serious challenges facing the nation’s farmers that deserve greater attention from our political leaders.

It was part of the discussions that took place on 10 April at a “Food 2050” symposium held in Perth by the UWA Institute of Agriculture. This drew together a cross-section of experts in a range of fields who examined the challenges facing farming communities and the longer term security of our food production system. My task was to address the issue of the state of rural enterprises and this article is based on the speech that I gave there.

The “farm problem”

Lying at the heart of the crisis facing the WA growers, and impacting on rural enterprise across Australia, is what has been described as the “farm problem”. The problem is caused by the interplay between rising agricultural productivity and the inelastic nature of food demand.

This has led to continual decreases in real farm prices and decreasing returns to farmers. Increasing competition in the food market has meant that any efficiency gains made by producers within their farm businesses are actually captured more by the consumer than the producer.

To counter this trend farm enterprises have sought to expand their area of production, develop new or additional crops or pastures, or grow large via the amalgamation of farms. This has led to the “get big or get out” mindset that has occurred across many of our rural areas in past decades.

However, many farmers lack the financial capacity or the opportunity to expand their business operations. This will result in a few much larger farms and the smaller farms that still exist will generate only minimal income.

These issues were highlighted in a study undertaken by the CSIRO for the Grains Council of Australia and Grains Research and Development Corporation (GRDC) back in 2003/2004. As the report noted:

“These two issues – amalgamation and low incomes – combined with the fact that much of the productivity increases have been labour productivity leading to less demand for farm workers, have led to a gradual depopulation of many regions and depressed regional economies. Local value-adding may have some scope for increasing the value of farm products, but value adding also adds cost, hence there may not necessarily be a net gain. These trends are a long-term reality of agricultural economies and are very unlikely to be easily reversed despite community and government will.”

Current state of the global food system

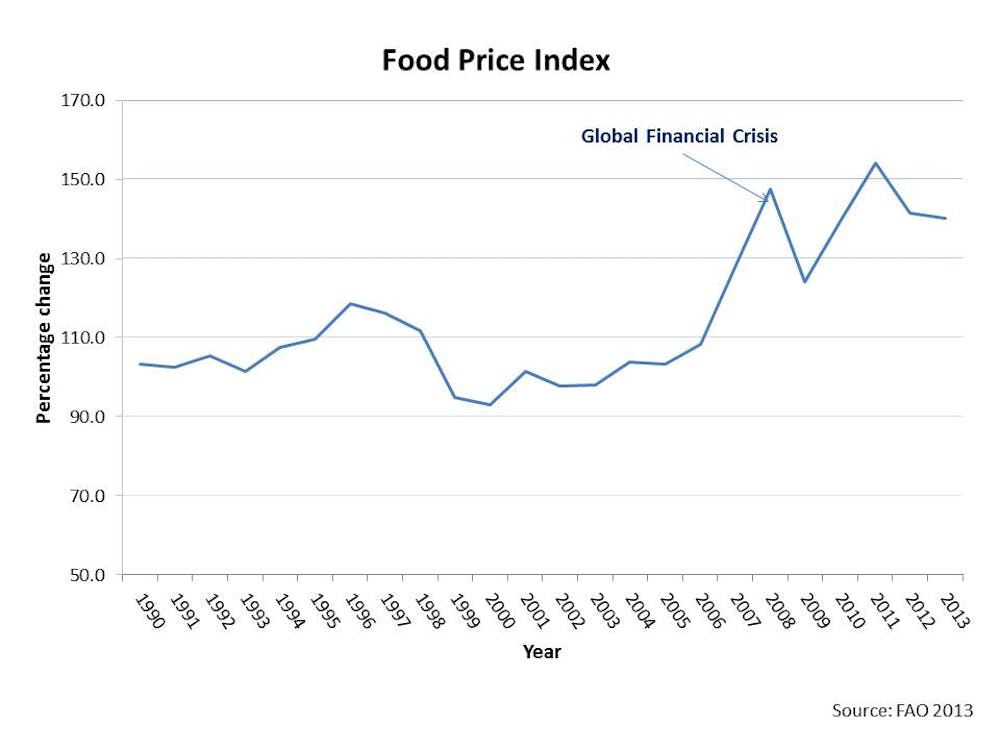

To understand the forces that are impacting on our rural enterprises it is important to take a look at the current state of the global food system. Despite farmers experiencing difficulties with farm gate prices the actual price of food rose significantly over recent years. The diagram below shows the Food Price Index of the UN Food and Agriculture Organisation (FAO), which illustrates the trend.

Between 2006 and 2008 global food prices increased significantly and despite the Global Financial Crisis (GFC) impacting on many other commodities the overall price of food has not declined, in fact it rose again sharply in the period from 2009 to 2011. Wheat prices rose by almost 30% and the price of corn was pushed up due to extreme weather conditions in the United States and Ukraine.

Another problem is the productivity within agriculture at a global level. Many rural producers around the world are undercapitalised and lack the land or technology to significantly enhance their efficiencies. The food to people ratio of productivity is estimated to need to rise by 70% over the next 40 years if food production is to match supply.

However, there is a lot of wastage. For example, the UN FAO estimates that as much as 1.3 billion tons of food is lost between the field and the table each year due to poor logistics management and storage. Writing in The Global Journal, Paolo Cravero observed:

“Agriculture is at a crossroads. Since the global food crisis of 2007 and 2008, foreign investment has soared as a means to lower costs and ensure the long-term viability of worldwide supplies. At the same time, a growing chorus of experts and activists is questioning the sustainability of a status quo approach. The industrial production system favoured by major agribusiness players has failed to address the challenge of chronic hunger, nor account for adverse environmental impacts – is ‘agroecology’ the future of food?”

Maintaining sustainability of the food system

In a study of the future of the global food system published in the Philosophical Transactions of the Royal Society – Biological Sciences in 2010, Charles Godfray and nine colleagues over viewed the current and future state of play for the world’s food system.

A further report by [The Institute for the Future](http://www.iftf.org/uploads/media/SR1255B_FoodWeb2020report_1.pdf)_ published in 2010 and authored by Miriam Avery, Bradley Kreit and Rod Falcon, projected key trends in the global food system over the next 20 years.

According to these analyses there are a number of forces likely to shape the global demand and supply of food over the next 40 years. The first of the factors driving demand is the rising population levels around the world.

By 2050 the world’s population (currently just below 7 billion) will rise to over 9 billion people. China will be expected to see its population peak around 2030, but India’s population will keep growing and the population of Africa is expected to double. For countries across Europe and for Japan the outlook is for population decline.

The rise in population will not only see a demand for more food, but there will be a growing demand for more luxury foods such as meat and dairy, and for foods to be supplied out of season via global supply chains.

The growing population will increasingly live in major cities and there will be a growth in supermarket and fast food retailing operations. In short, people will be wealthier and they will want more processed food, and exotic foods with a change in diets from primarily vegetarian to more meat and protein foods.

The ability for rural producers to meet this rising demand will depend on a range of factors of which one of the most important is the ability of farmers to keep increasing crop yields. Over the past 50 years there has been a dramatic increase in crop yields; however the rate of such increases has slowed each decade.

Our farmers’ capacity to produce more food by 2050 is likely to be dependent on R&D that can result in breakthroughs in technologies and farming practice. This will require the adoption of new animal breeding and husbandry techniques plus new varieties of crops.

Working against this rise in primary production is the impact of climate change and concerns over food safety and ethics. For example, climate change is already impacting on weather patterns generating floods or drought and while scientists continue to debate the nature of this impact, there are already signs of climate change negatively affecting already fragile river systems and associated fish stocks.

In the oceans the supply of fish is also under pressure. There has been a growth in the past 50 years in the world’s fishing fleets and over the past 40 years this fleet has increased sixfold. However, most of the world’s fish stocks are now harvested to full capacity or over exploited and fish harvests are either static or declining.

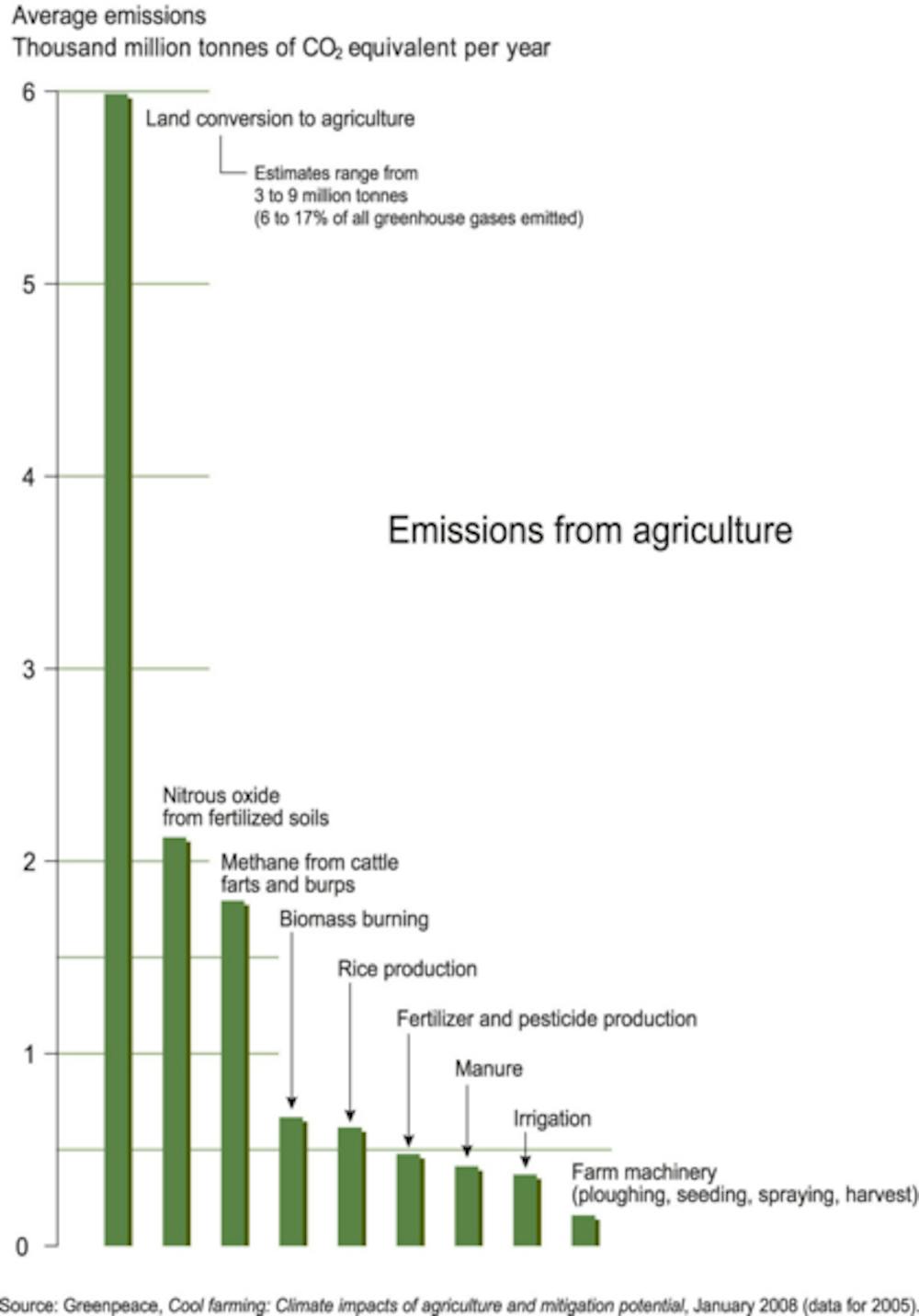

In many regions there is a decline in soil productivity and the clearing of new farmland is fraught with environmental concerns due to the impact this has on carbon emissions. For example, it is estimated that on average the clearing of land for farming leads to net CO² emissions that are 6 times greater than those generated by other forms of land use. This is shown in the accompanying diagram.

Overcoming the climate change sceptics

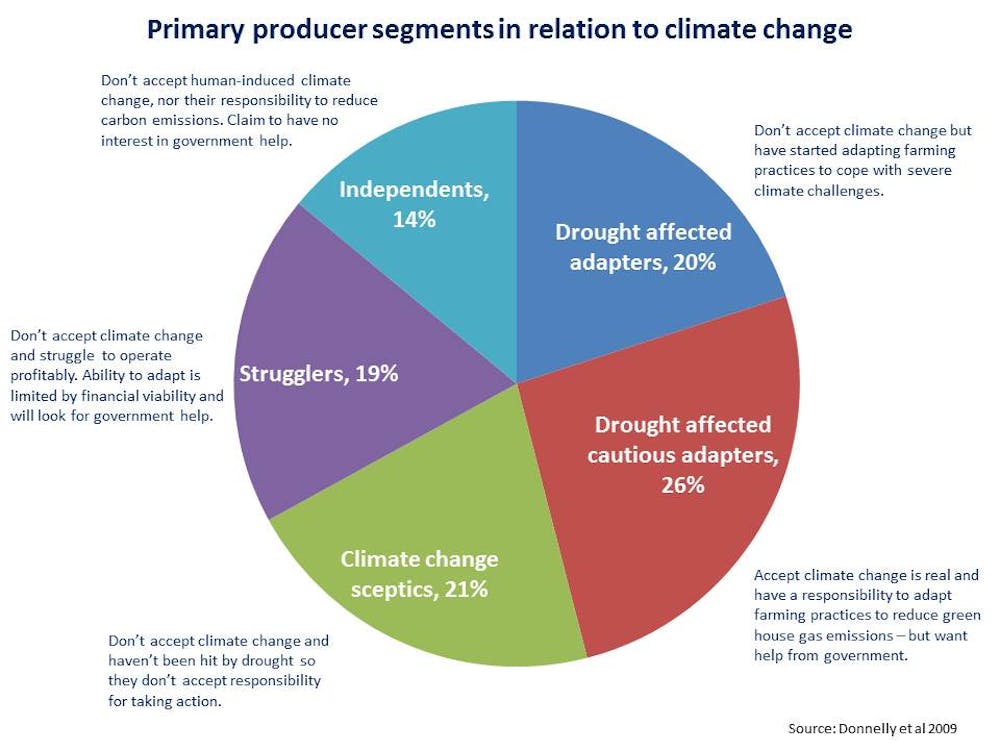

Yet many primary producers are resistant to the challenges of climate change. In a study of Australia’s Farming Future published in 2009 by David Donnelly, Rob Mercer, Jenny Dickson and Eric Wu for the federal Department of Agriculture, Fisheries and Forestry, surveyed 1,000 farmers in relation to their attitudes towards climate change. They also surveyed 1,000 people from urban areas.

While 58% of the urban population believed climate change was real and caused by human activity, only 26% of primary producers held this view. As illustrated in the following diagram these farmer groups were segmented into different types of sceptic. Some were sceptical but had been hit by drought and therefore were prepared to start taking action. Others were sceptical and had not yet felt any environmental impacts so they felt no need to take action.

The ‘strugglers’ were not only sceptical but had no resources to apply to any remedial action. Even those who accepted climate change science were of the view that government assistance was required to allow them to take action.

These attitudes amongst rural producers are important as they will determine how readily many farmers adopt more sustainable farming practices, reduce new land clearing and introduce programs such as enhanced biodiversity of cropping, interlocking crop cycles, dense polycultures, biochar and carbon management.

Feeding into this mix will be market based pressures over food safety and the ethical treatment of animals. Consumers are increasingly concerned over use of genetic modification in foods and the safety of foods. The complex nature of food supply chains makes it more likely that accidents will occur.

Already there are signs of the overuse of antibiotics in animal husbandry resulting in antibiotic resistant strains of bacteria emerging. High profile cases of food borne illness have an impact on consumer confidence. However, they also result in government regulators and major food retailing groups imposing more stringent food safety codes of practice. These factors impact on rural producers by forcing up the cost of food production and supply.

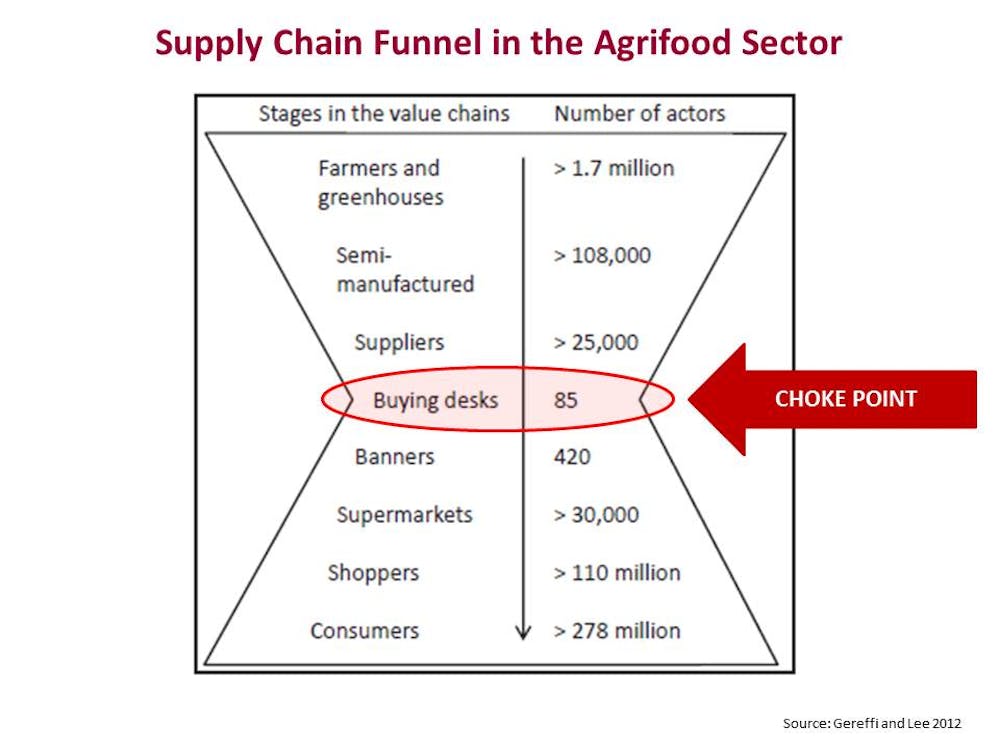

Supply chain funnel in the agrifood sector

One of the problems facing agricultural producers is the “supply chain funnel” that has emerged in the agrifood sector. As shown in the diagram below there is a “choke point” in the area of buying desks that are increasingly no longer in farmer or government control.

The diagram comes from a study by Gary Gereffi and Joonkoo Lee from Duke University in a paper published in 2012 in the Journal of Supply Chain Management on the state of global supply chains. The model is from the European Union (EU), but it shows a trend that is found increasingly around the world.

The power of global buyers has also been enhanced by the concentration of ownership into fewer large retailing businesses. These firms and large global buyers now dictate quality and the timing and price of food from producers.

Major retailers and buyers will demand more quality and stricter controls over food safety issues. Some will work with small groups of selected, often large scale producers, to supply produce at pre-determined levels of quality, price and delivery times. Many smaller farmers will not meet the necessary standards.

The role of co-operative enterprise

Smaller producers who wish to compete in these global supply chains must develop niche markets in order to survive. However, in Europe there is evidence that small producers working via co-operative enterprises can compete.

For example, a study published in the American Journal of Agricultural Economics in 2004 by Claude Menard from the University of Paris and Peter Klein from the University of Missouri examined the role of co-operative enterprises.

They examined the cases of 7 meat, dairy, fruit and vegetable co-operatives within the EU. It was found that these co-operatives could compete against three major wholesaler and retailer firms that controlled between 40% and 80% of EU markets.

They did this via large scale and scope from cooperative action, high investment in R&D and the development of their own producer brands that gave them a degree of marketing control within the retail channels.

Co-operatives can enhance the bargaining power of small rural producers in the face of major corporate players who control the “choke points” within the food supply chain. However, a problem for co-operatives is that they are often misunderstood, even by producers, and can be viewed as potential monopolies. As Menard and Klein explain:

“On the one hand, regulators are concerned with increasing concentration in the processing and distribution sector and tightly coordinated producer networks appear to counterbalance that concentration. On the other hand, tightly coordinated groups of legally independent firms look like cartels…, competition authorities tend to take an ‘inhospitable’ approach to such nonstandard contractual arrangements.”

Where to from here?

So in conclusion there are at least four major trends that are likely to impact on rural enterprises in the food sector over the next 40 years:

The first of these will be the mounting pressure on primary producers over food safety and also the need to supply more diverse, wholesome and “authentic” food. This will require producers to innovate and find ways to market their products differently to reflect value adding.

The second major impact with be that of climate change. In order to deal with a changing and uncertain climate there will be a need for more biodiversity of cropping and animal husbandry to avoid mono cultures that are less resilient to climatic change. This may see the emergence of regional brands with shorter food supply chains to local markets focusing on healthy, wholesome foods.

The third trend relates to the need for rural communities to collaborate for their own self-interest. There is the need to enhance their bargaining power against the concentration of increasingly global buying and distribution organisations. Such supply chain structures leave the farmer with a “price taker” role regardless of their attempts to enhance farm level productivity.

The demand for locally grown food may also rise according to some analysts. However, there will still be a need for greater collaboration at the regional level in order to offer flexibility in food production and distribution.

It is here where co-operative enterprise business structures can play a potential role. They have demonstrated over time a capacity to empower primary producers and draw together resources to achieve things that might otherwise have not been possible.

A final trend is the need for enhanced innovation in farming and land use practices as well as waste disposal methods. Farmers will need to move to more flexible land use, adaptive cropping methods and carbon capture and management processes. This will be assisted by use of information management tools to aid in farm business modelling and the monitoring of markets.

In summary the pattern that emerges is one of a globally competitive market with a highly concentrated buyer and retailing channels. Producers will need to get larger, find niches or cooperate. Future sustainability and productivity in the face of climate change, water scarcity and food safety concerns will pose significant challenges.