While this year’s relative stability in crude oil prices appears to have lulled us into a false sense of security, the dramatic fall over the last few weeks reminds us just how volatile these prices can be.

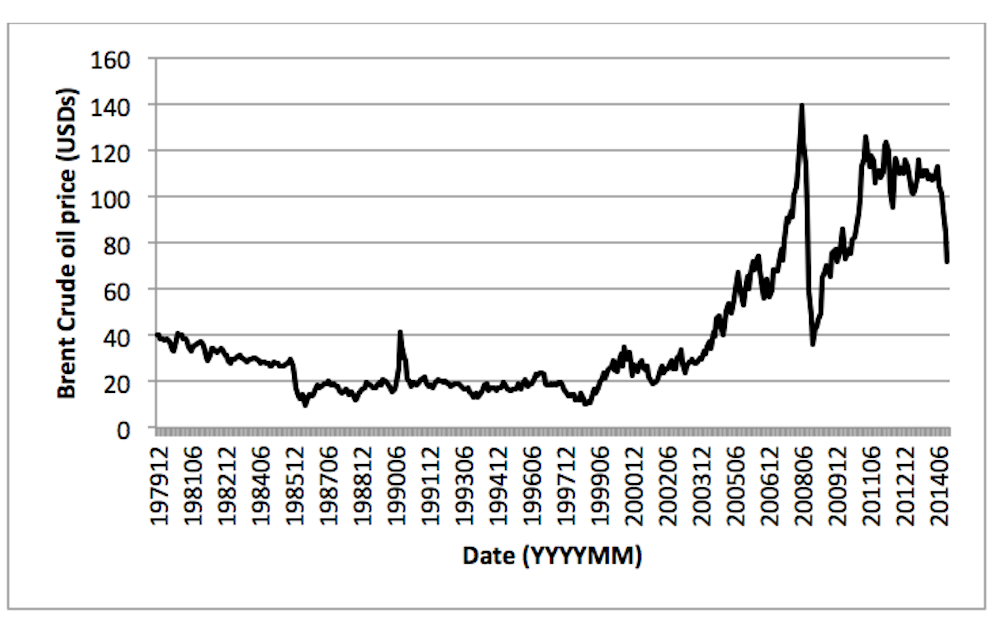

The chart below highlights the movements in the USD price of Brent crude over the period from January 1980 to mid-December this year. The rapid growth in crude oil prices over the period from 2007 to 2008 gave us some insight as to just how quickly crude oil prices could rise. The fall in late 2008 associated with the global financial crisis and the more recent plunge in crude prices show us how quickly crude oil prices can fall. The price today is a little over US$60 per barrel.

Brent crude oil price (FOB USD price per barrel)

The impact on Australian petrol consumers

Who gains and who loses with these dramatic shifts in price? It is hoped these movements will eventually be reflected at the petrol bowser. The problem for consumers is that it takes time for stocks of crude purchased at higher prices to work their way through the system to the petrol bowser. Refineries hold stocks of crude oil acquired at the previously high prices and stocks of diesel and petrol refined from this higher priced crude also take time to pass into the market.

Nevertheless, we are seeing some benefits from this drop in crude oil prices. For example, the chart below shows the Australian average retail unleaded petrol price (ULP) has decreased from a little over 146 cents per litre at the end of September to around 132 cents per litre at present. This will probably continue as crude prices have almost halved over the last six months and these price falls will eventually affect petrol prices.

National Average retail ULP price

The impact on producers

The main players in the crude oil market include the OPEC members (Algeria, Angola, Ecuador, Iran, Iraq, Kuwait, Libya, Nigeria, Qatar, Saudi Arabia, United Emirates, Venezuela), US, Russia, China. The US, Saudi Arabia and Russia are the biggest producers by a considerable margin, accounting for almost half of world crude oil production in 2014.

Crude oil producers earn lower profits from the sale of crude oil and if the crude oil price falls then countries like Russia that are particularly dependent on revenues from sale of crude oil will suffer. It has been suggested the recent tumble in the Russian rouble is due solely to the fall in revenues from sale of crude oil. Apparently, Russia requires a price around US$100 per barrel for oil production to make sense.

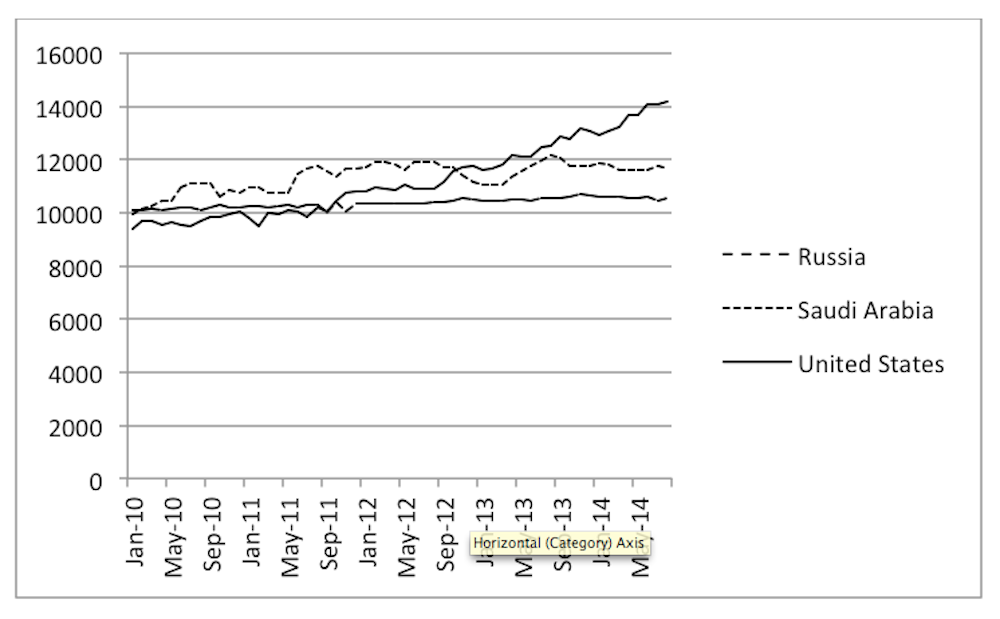

Some commentators have suggested US and Saudi production has been increased to apply further economic pressure on Russia. The chart below provides some insight into this question. It plots the Energy Information Administration international crude oil production data for the period from 2010 to August 2014.

There is clear evidence of increasing US production with the US monthly production increasing from 9,377 thousand barrels per day in January 2010 to 14,162 thousand barrels per day in August 2014, but this is not a reaction to recent events.

The growth in US production appears to be part of a continuing trend over the last 3-4 years, rather than a sudden reaction to the destruction of MH17 over Eastern Ukraine in September 2014 or the annexation of Crimea, in March 2014.

Saudi Arabian production has been quite volatile over the last 3-4 years though it has not grown to the same extent as the US production. Indeed, it appears quite flat over the last 12 months with the daily production rate actually decreasing between January 2014 and August 2014.

Russian production has been much more stable than either US or Saudi production.

Monthly Crude Oil Production, US, Saudi Arabia and Russia

There is no doubt that US crude oil production has increased since 2010 and that this increase accounts for more than half of the increase in world production over the period. But it is difficult to see a link between these general trends in crude oil production and recent activity in the Ukraine.

It takes time to change crude oil production levels and it is very costly to do so. It seems unlikely that production has led to the recent fall in crude oil prices though it is true this argument is based on monthly production rates up to August this year. It is possible that US crude oil production has been further increased in the months following August, though the most recent data for September suggest US crude oil production was down a little if anything.

Ultimately, crude oil production is increasing and much of this increase is coming from the US. The impact on the other crude oil producers in the world will vary from little impact in the case of Saudi Arabia though to considerable economic cost for countries like Russia.

The impact on crude oil purchasers

A cut in the crude oil price of almost 50% just as the Europe and US winter approaches has got to be good news for the northern hemisphere. The cost of energy and heating generally rises during this period and many will have full Christmas stockings with this particularly timely present.

More importantly, the less developed nations of the world depend on oil and coal for their energy needs and this drop in the cost of energy will have a dramatic impact on the living conditions in these countries as costs of electricity and transport fall. This will free up cash for the other necessities of life.

The crude oil producers have seen good times for more than three years with crude oil prices exceeding US$80 per barrel. It looks like the pendulum is swinging back towards a time of lower crude oil prices and consumers can again acquire energy at more reasonable rates. While this is bad news for the producers it will have a dramatic impact on the world economy which has slowed considerably in recent years.