What is the new normal for the Australian economy? With unemployment rising, commodity prices reaching new lows, and confidence subdued, is the Australian economy prepared to handle offshore headwinds that continue to concern the market? We explore the fundamentals in this ‘Economic headwinds’ series.

The Australian economy is well placed for the medium to long term. But we face risks as we transition back to broad-based growth.

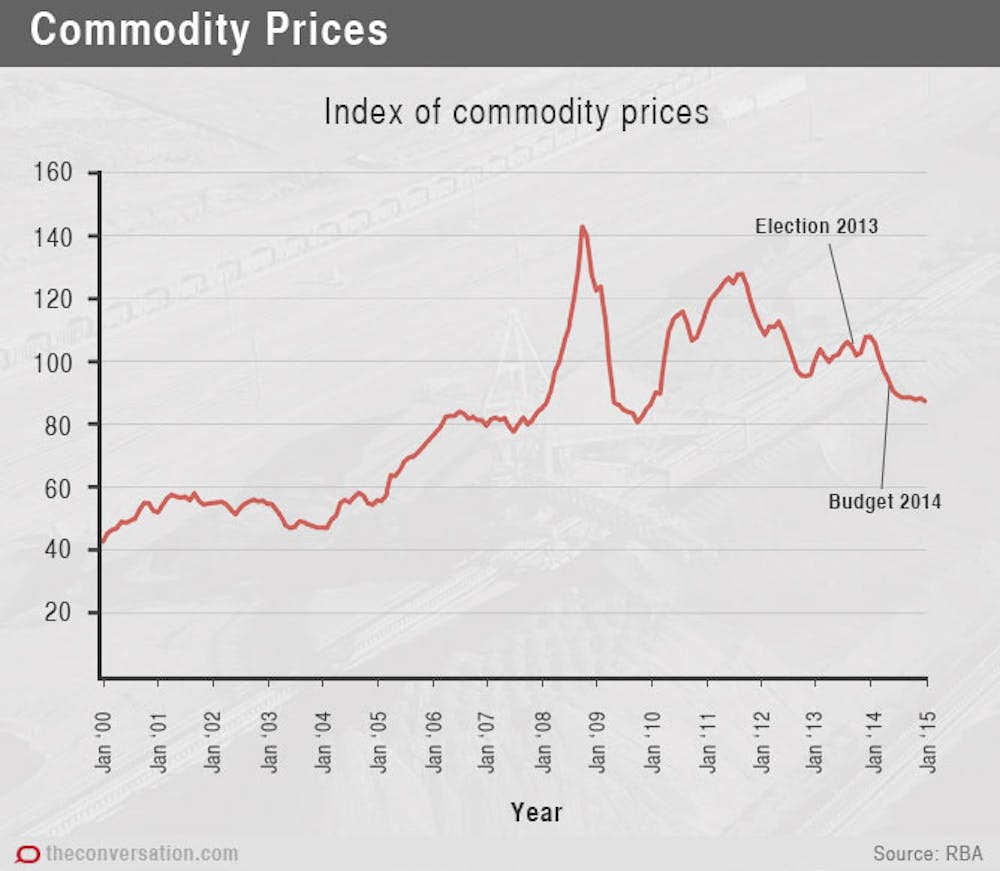

Australia’s resources boom lasted a decade. Iron ore, coal, gas, gold - you name it. If we could dig it up, China was ready to buy it at record prices.

But adapting to a boom is hard. The boom increased demand for the Australian dollar, increasing the exchange rate (which is just the price of an Australian dollar). This hurt non-commodity exporters and led to a two-speed economy. The resource centres of Western Australia and Queensland boomed while the manufacturing and services centres of Melbourne and Sydney hit the wall.

We adapted. It was tough.

However, mining booms are temporary. As exploration and development expands supply, the prices inevitably drop. Our mining boom has ended. We have seen massive falls in iron ore, coal, oil and gas prices in recent years. It was fun while it lasted, but the inevitable has occurred and now the Australian economy is adjusting back again.

It’s good the boom is over

This is a good thing. A mining boom is like a boozy party. Great while it lasts, and it may lead to a short-term hangover. However, so long as our economy can adapt back to the “new normal” of a lower exchange rate and more balanced growth driven by broad trade with our Asian neighbours, the end of the boom will lead to a new period of economic prosperity. The key is adaptability.

The end of the boom doesn’t mean that our earnings from mineral exports are back to 2000 levels. The development of new projects means that we will keep exporting and earning more. Put simply, quantity matters as well as price.

Further, as the end of the boom leads to a fall in the Australian dollar, this hurts consumers as the price of imports rise. But Australian companies that compete with imports will find life easier. There will be more growth and jobs in these areas.

Similarly, the drop in the exchange rate helps our non-commodities exporters. Australian farmers, tertiary educators, high-end manufacturers and other service exporters should all have big grins on their faces. They will be expanding over the next few years as the rest of the world finds that they are much cheaper.

So the end of the boom will mean a return to more sustainable, balanced long-term growth across our economy. Asia is still growing and we are still well placed to benefit from that growth.

What are the short-term risks?

The biggest risk is that the federal government will panic. Transition means that unemployment will increase as workers fly-out of the mining centres and move back to the south eastern states. Federal tax revenue will also temporarily fall as profits decrease in the resource sector but are yet to rise in other sectors. This means that there will be an increasing budget deficit. Fortunately, we have low levels of government debt by international standards, interest rates are at historic lows and our government can easily borrow to both cover the deficit and invest in infrastructure that will assist the transition.

Our federal government should not party like it is 2010 again. But there is no budget crisis.

The second biggest risk is that state and federal governments will fail to continue the necessary long-term reform needed in areas such as taxation, health, education, transport and energy. The outcome of the Queensland state election has undermined reform. It shouldn’t. The evidence is clear that reforms, including privatisation, but particularly reforms that sensibly introduce competition where it can work, have benefited people in the states that have had the leadership to push forward.

There is still plenty of scope for reform. Congestion charging on urban roads with funds being used to improve public transport, is a no-brainer. Removing impediments to the sharing economy, such as the regulations that protect vested interests but undermine platforms like Uber and Airbnb, will mean better and cheaper choice for families. Requiring government infrastructure projects to have independent cost-benefit analysis will reduce political boondoggles that help marginal electorates but cost the broader community. Moving to real-time pricing in electricity and using smart grids to give consumers more control over their power bills, will reduce energy use and carbon emissions while saving money for households.

There is a long list of reforms that governments should be pursuing. These reforms are necessary to maintain our economic flexibility. But with any reform there will be winners and losers. Governments need to have the guts to implement reforms, but the compassion to reform in a way that protects the most vulnerable in the community.

Finally, our governments need to remember the compact that has underpinned Australia since federation. We do not leave people behind. There has long been a series of transfers, through the grants commission and through the distribution of the GST, from the richer states to the poorer states and from the cities to the bush. These transfers help guarantee that all Australians can gain from long term economic growth. These transfers need to continue. But they also need to be transparent. And states need to remember that today’s winners can be tomorrow’s losers. The transfers are like a national insurance policy that protect us all.

So, the economic future is looking bright for Australia. Sure, the economic winds have changed. But so long as we can adapt and “change tack”, and governments do not get in the way, the next ten years for Australia are likely to be even better than the last ten.