The past year has seen two major reports on the economics of higher education, each seeking to reform the way undergraduate study is financed.

The Grattan Institute’s Graduate Winners appeared in August, and is best read as a counterpoint to last December’s Higher Education Base Funding Review.

Each report has a different aim. The Review proposes a new formula to finance universities sustainably, based on assessing the costs and benefits of their teaching and research programs. Graduate Winners proposes to slash the cost of taxpayer support for undergraduates – now around $6 billion a year – by charging students more.

How things work now

First let’s look under the hood, at the mechanics of the current system.

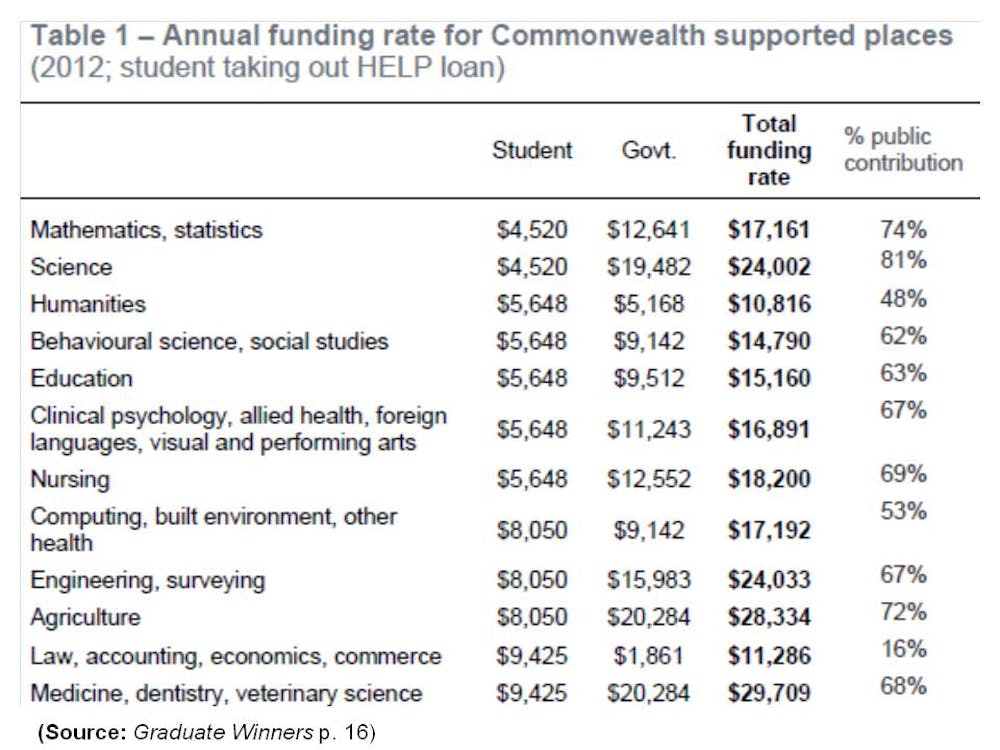

Public places in bachelor degrees are co-funded by students and taxpayers. The total per place varies widely due to different delivery costs: humanities courses get around $11,000 a year while medicine gets around $30,000.

Relative to costs, students pay different fee rates: from around 20% of the total in science, to 30% in nursing, to 50% in the humanities, to 80% plus in commerce or law. (see Table 1).

The logic here is mixed: fee rates may factor in higher incomes for graduates in higher status professions such as law, or low demand for courses such as science.

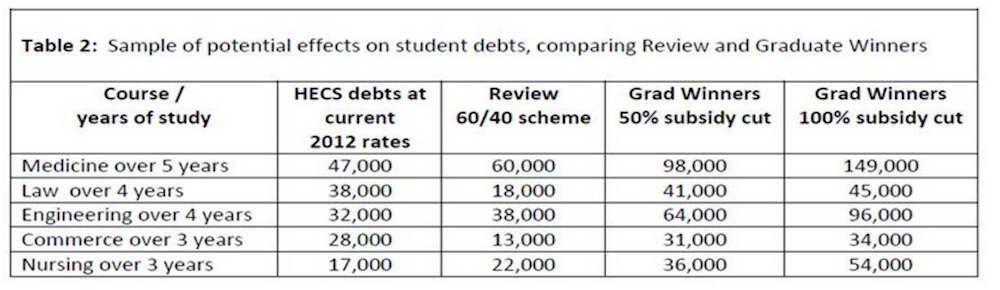

At 2012 rates, students relying on HECS loans until they graduate can expect debts of $47,000 after 5 years in medicine, $38,000 after four years in law, $32,000 after four years in engineering, $28,000 after three years in commerce and $17,000 after three years in nursing.

The Review notes that our student fees are among the highest in the OECD; but that the proportion who benefit from government loans is also the highest.

Reviewing the Review

The Review looks at provision costs in different disciplines. Then it estimates the public benefits of higher education generally, as a basis for a 60% rate of public funding across the board. Student fees would then make up the remaining 40% needed in each discipline, varying in line with course delivery costs.

A problem here is that a 40% rate would raise fees in high-cost courses such as medicine or engineering, where students now meet around 30%.

The Review argues that fair access could still be maintained with HECS loans: on average, these are repaid in 8 years although low income earners may never repay.

We can see how the Review’s scheme would affect HECS debts in each discipline by lifting or dropping student fees to 40% of total current funding, that is student and taxpayer payments combined (see Table 2 further below).

At total funding of around $30,000 a year a medicine student paying 40% would have a higher HECS debt of around $60,000. An engineering student’s debt would also be higher at $38,000. But a law student’s debt would be lower at $18,000. Likewise a commerce student’s, at $13,000. Meanwhile a nursing student’s debt would be higher at $22,000.

That nursing students should incur higher debts than for law or commerce in a 60:40 scheme highlights the design challenge for policy makers. The question is how can universities finance each discipline sustainably, while making places affordable for students, while recognising that graduates in some courses benefit more highly, while spending public money frugally.

The Review also argues against deregulating HECS prices, noting that public universities have all lifted their fees for public places to the maximum allowable. This has been partly for the income; partly because price is seen as a proxy for quality, and partly because with deferred repayment, HECS loans reduce consumer pressure to be price-competitive.

Grattan’s radical response

Graduate Winners starts at the other end. It estimates the private financial benefits from degrees in different disciplines, compared with the incomes of year 12 school leavers.

Then it asks at what point the cost of tuition would be seen by students to outweigh the private benefits, leading to fewer enrolments and labour market shortages.

Only then would public subsidies be needed, to attract enough students into each discipline to ensure a sufficient supply of qualified people.

It finds that in almost every discipline “Graduates are such big winners that people would study even without subsidies”.

Then it proposes subsidy cuts in most courses by up to 50% in the short term, and longer term to zero, to free up public funds for other purposes.

Where the Review sees public funding underpinning the public benefits of higher education, Graduate Winners claims that these would still flow to society, whoever pays. Since the non-financial public benefits of higher education are indirect and hard to measure, it’s hard to prove or disprove either position.

Graduate Winners makes its clearest case where professional training meets defined demand, as in medicine. It is less persuasive in fields not geared to professions, which aim to cultivate inquiring minds and responsible citizens.

The humanities for example are not amenable to economic calculus. We may as well ask policymakers to price wisdom, outsource virtue or run a cost-benefit analysis on sin.

Possible consequences of subsidy cuts

The Graduate Winners cuts imply much higher student HECS debts, if total funding is to stay at current levels.

The suggested short term 50% cut to existing subsidies would lift a graduate’s HECS debt in medicine to around $98,000, in engineering to $64,000, in law to $41,000, in commerce to $31,000 and in nursing to $36,000.

The longer term zero-subsidy suggestion would mean medicine, engineering, law, commerce and nursing graduates would incur HECS debts of around $149,000, $96,000, $45,000, $34,000 and $54,000 respectively. (see Table 2).

Note, the Review found many courses under-funded but its costings include a base research element. It says many could be offered in non-universities for 10% less. Graduate Winners says research should be funded separately. On its zero-subsidy figures debts would be lower than given here. It says universities may not maximise fees in courses such as medicine.

Graduate Winners also claims that with higher fees, HECS loans would keep study affordable. It insists that for those on low incomes, even high-fee study is “free”.

On affordable access, the evidence is mixed. Low SES students are more debt-averse. But, while HECS rates have risen since the scheme began two decades ago, the rate of low SES participation has been stable during massive expansion. Then again, low SES students remain clustered in lower-cost, lower-status courses. And again, this may reflect lower school performance against the entry requirements for higher-status courses.

Do low-income graduates study for free? Not really. While unpaid HECS debts are indeed funded by taxpayers, this does not make study “free” as in the 1970s: a large HECS debt will limit a person’s capacity to borrow for a home or business venture.

Whitlam-era students did not face the prospect that study might leave them in debt till they drop, whether or not they graduate. At zero-subsidy fee rates, why would a gifted, low-SES school leaver keen on medicine not opt for commerce instead, just to avoid the risk of a HECS debt four times larger for a degree taking two years longer?

Conclusions

Each report seeks new trade-offs, to be implemented gradually. Given course differences a 60:40 formula is too simple as a funding optimiser, while Grattan leans too hard on HECS as an opportunity equaliser.

Yes, HECS has helped to expand the sector fairly and cost-effectively. A typically makeshift Australian innovation, it’s up there with the Ute and the Hills Hoist clothes-line. Is it a fee? A loan? A tax on over-achievers? All of these, sort of. But the TARDIS it is not. It can’t contain the risk to students of cranking up fees and over-revving HECS. Unless governments waived unpaid debts say 10 or 12 years after graduation (thwarting Grattan’s attempt to save taxpayers billions each year).

For universities, a risk with Grattan-style policy is the UK example, where funding cuts and fee hikes have led to 52,000 fewer enrolments this year. For some institutions this may crunch revenue, close programs, hurt students and damage reputations.

In Australia, similar scenes are taking place in TAFE colleges, due mainly to State government funding cuts. And some universities are closing programs in thin domestic markets, as competitors expand in an uncapped system.

A risk with program disruption in domestic student markets is damage to the sector’s reputation in international student markets. Here we outperform the world as exporters: low or negative growth can cost our economy billions over time.

With higher education offering major channels to bridge cultures and economies in Asia, policy should now aim for a stable and vibrant sector, with accessible domestic provision and an unassailable global brand.

Sustainable quality rests on stable rules and stable investment. To contain costs, there is scope to optimise the way the sector supports research-centred versus teaching-centred missions, and on-line versus on-campus modes of delivery.

In the end, policy will turn on two questions. How do we construct (and finance) a fair go for each new generation? And what role do we want the sector to play as a nation-builder, beyond meeting market demand for expertise?