Without a clear direction of where the Australian economy is heading, the consensus to keep the cash rate at its current level of 2.5% remains strong.

Uncertainties surrounding the domestic and foreign economies have not abated since the RBA last met in December. Globally, while asset markets are performing well, GDP growth remains subdued, pointing to a disparity that must be resolved eventually.

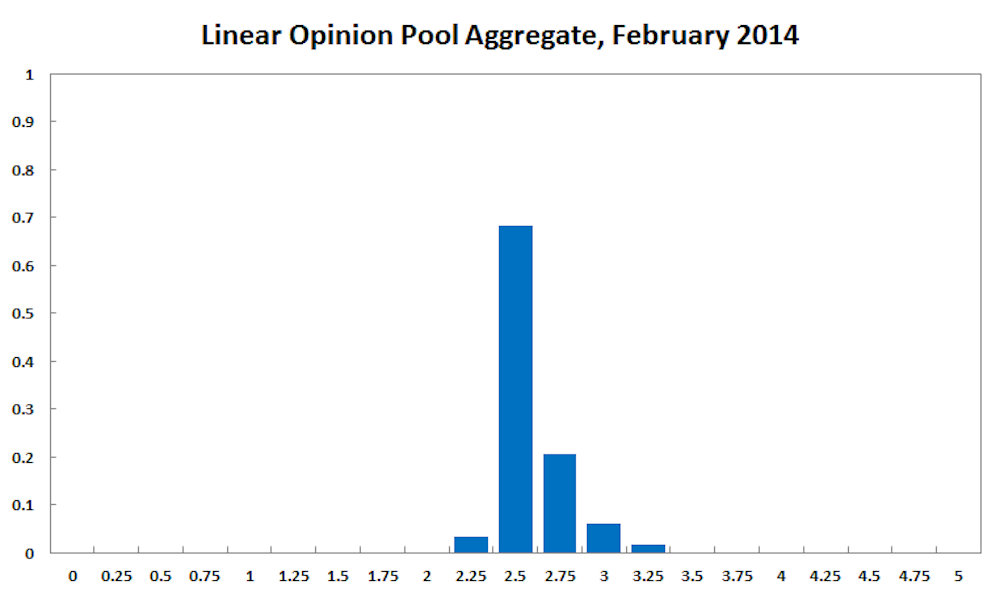

The Centre for Applied Macroeconomic Analysis (CAMA) Shadow Board’s confidence in leaving the cash rate steady rose to 68% (up from 63% in December 2013). According to shadow board members, the probability of a rate cut being required is 3% (down from 7% in December) while the probability of a rate hike being needed is 28% (down from 30% in December).

Inflation remains well within the 2-3% target range, despite a larger than expected increase in December, investment (especially in mining) and consumption remains tepid. The economy is being supported by historically low interest rates and an Australian dollar now hovering around 87 US cents, a 21% fall from its recent peak. This expansionary policy setting is generating early signs of improvements in retail sales, building approvals and local business conditions.

Overseas, the picture continues to be characterised by uncertainty. While growth in US output has accelerated to an annualised rate of 3.2%, underscoring the US Federal Reserve’s decision to taper its quantitative easing program, the rest of the global economy is looking less promising.

Europe will probably continue to show weak growth as long as the debt overhang and structural problems caused by the sovereign debt crisis are not fully addressed, while China will likely settle on a lower growth trajectory, with the possibility of a more damaging credit crisis persisting.

Both domestic and international asset markets have experienced double digit gains in 2013, fuelled by cheap credit and possibly excessive optimism. This divergence between the real economies and asset prices will ultimately need to narrow, either because global economic growth picks up significantly, validating the large increases in asset prices, or because asset prices will fall to more realistic levels.

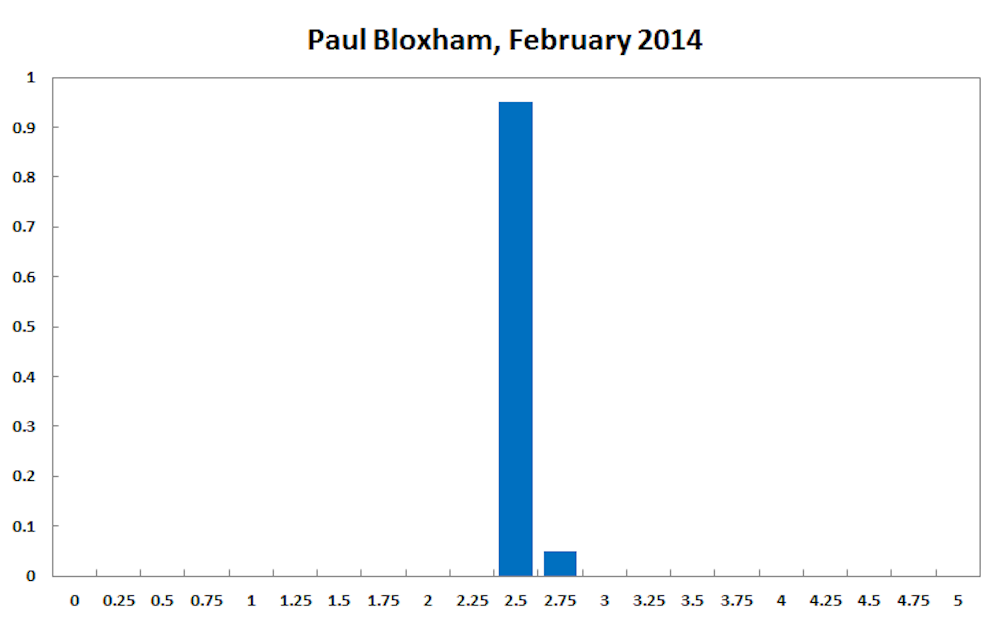

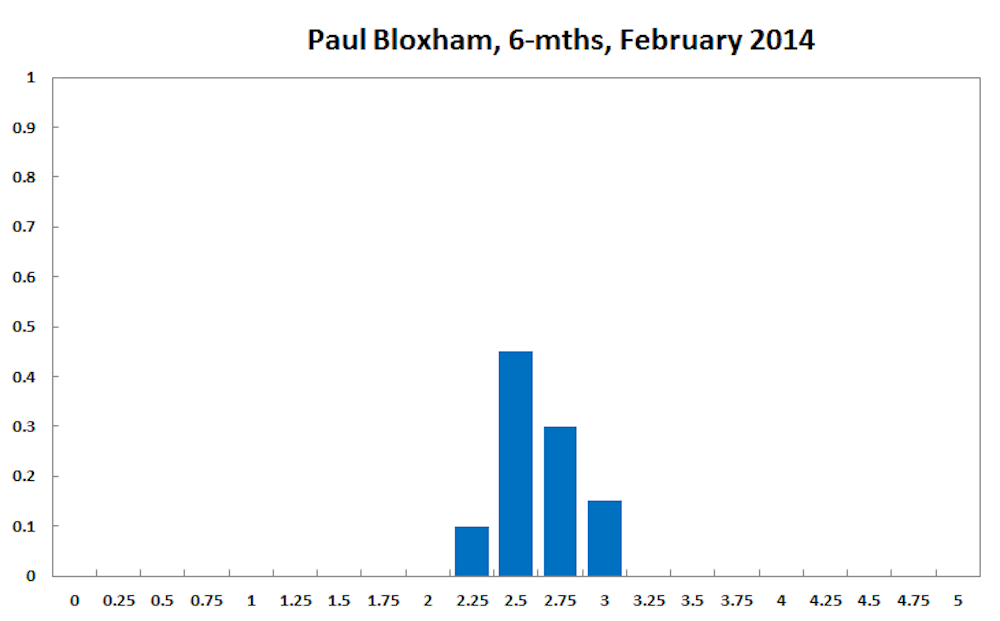

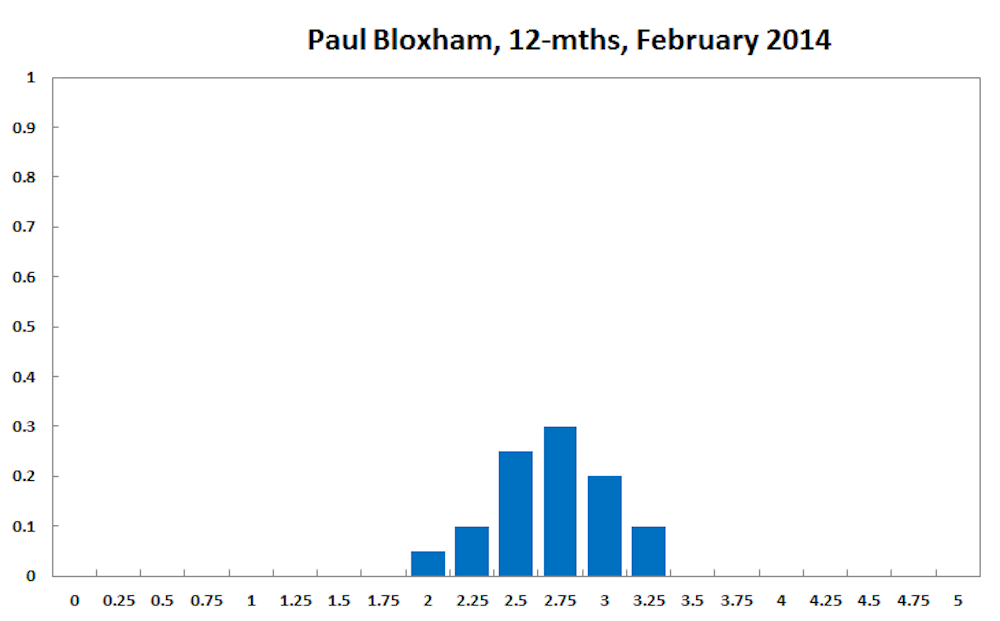

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Timely demand indicators for the local economy have generally lifted since the last board meeting. Retail sales, building approvals and measures of local business conditions have all shown improvement over the past couple of months. The housing market has also continued to pick up strongly. Together, these indicators suggest that monetary policy is continuing to get traction in the economy. The recent fall in the Australian dollar has also helped to loosen financial conditions further. The recent lift in inflation suggests that there is unlikely to be much scope to cut interest rates any further during this easing phase, barring an unforeseen negative shock. I recommend that the cash rate is left unchanged at 2.50% and see it as more likely than not that the cash rate will need to be higher than its current level in 12 months time.

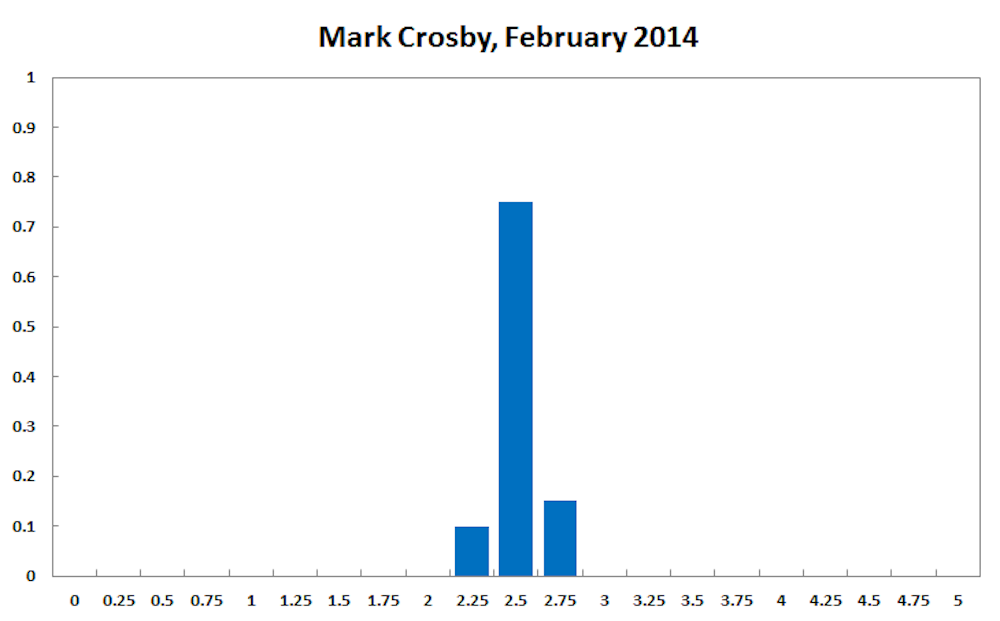

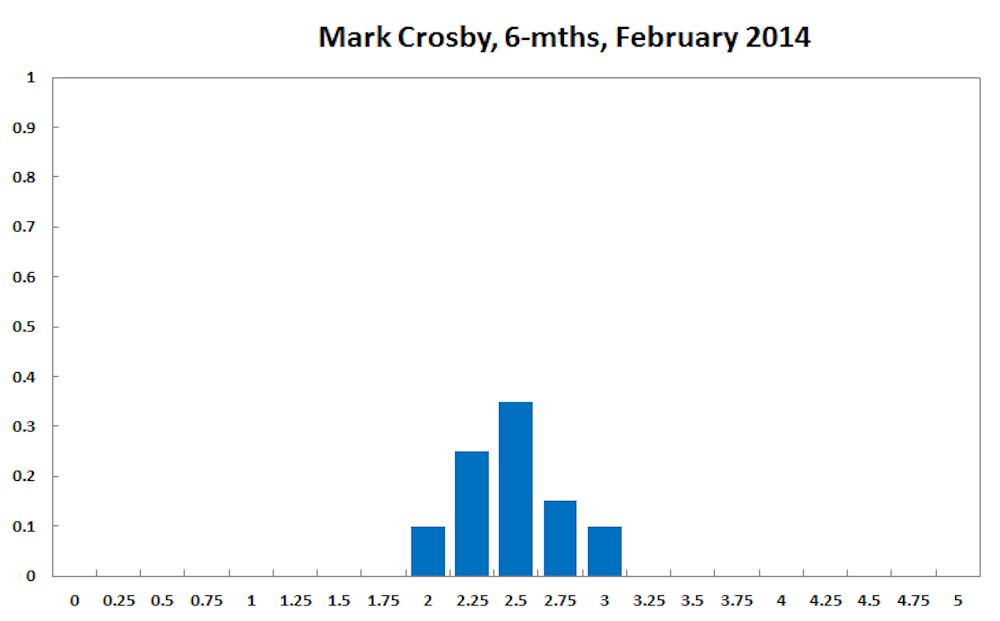

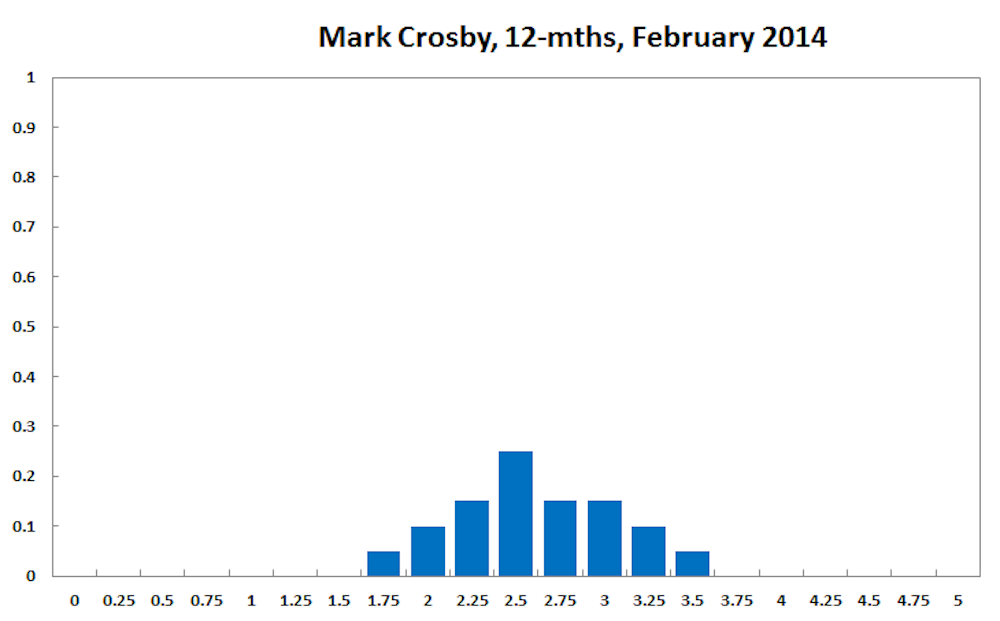

Mark Crosby, Associate Professor, Melbourne Business School:

Continuing uncertainty about the speed and impact of tapering suggests adjustments to monetary policy in the short term ought to be made with caution.

At the six to 12 month horizon, the RBA will have to juggle continued weakness in advanced economies, and some important emerging markets against the problems of inflation and asset price growth caused by continued low interest rates.

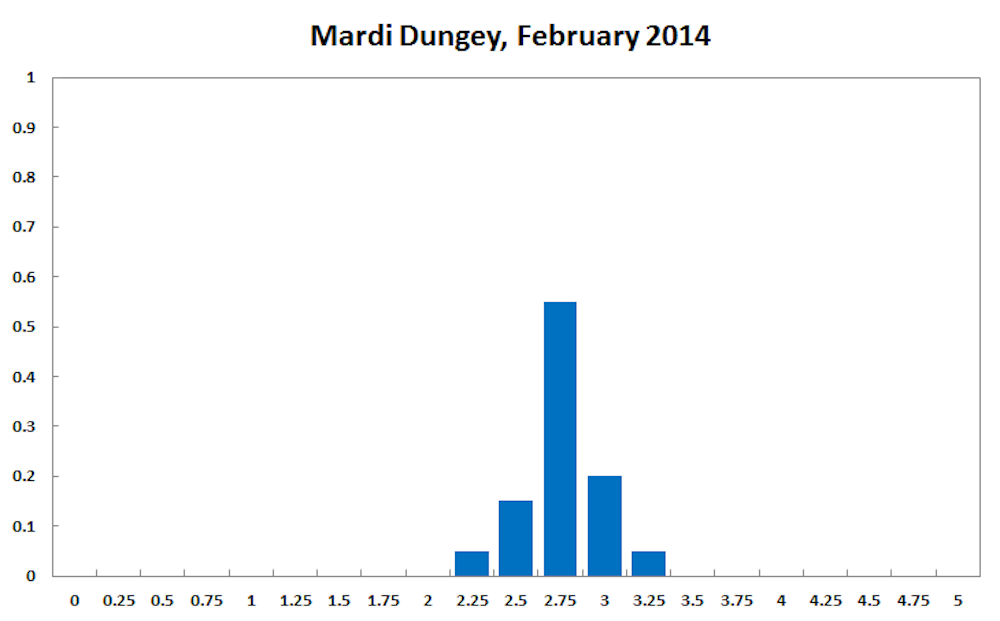

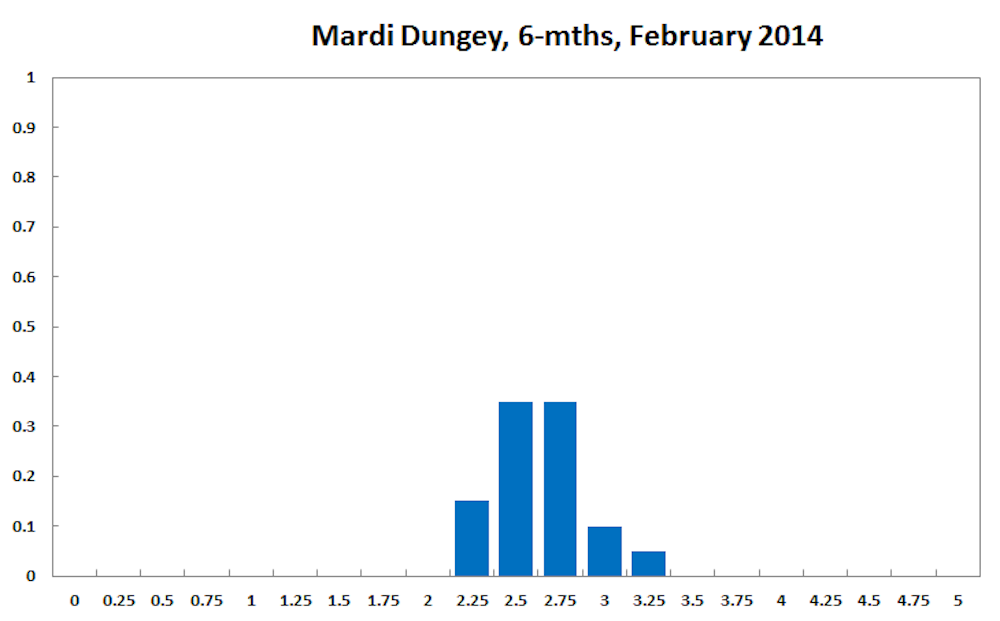

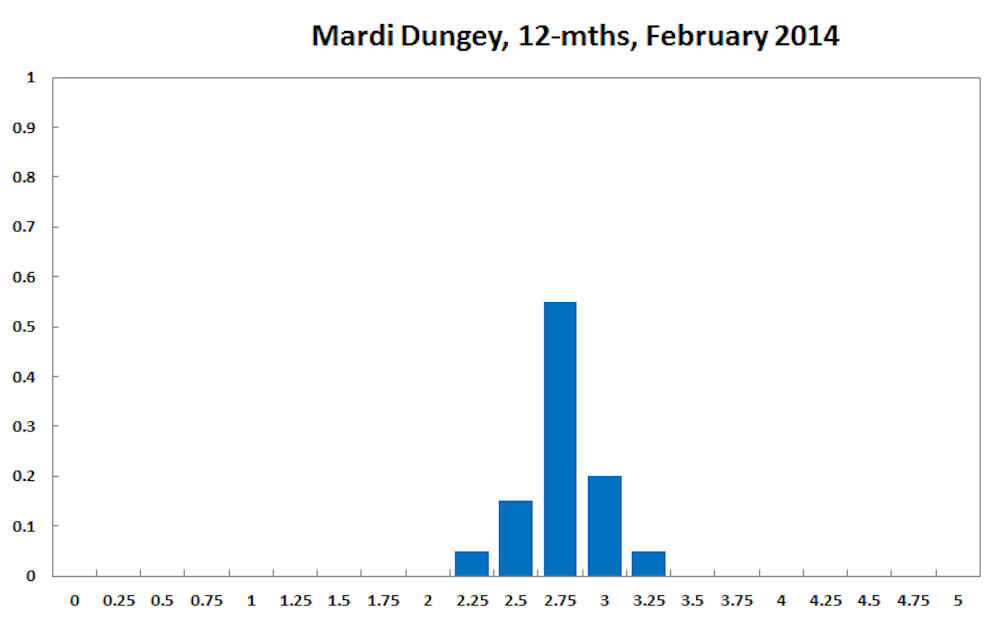

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA:

No comment

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

No comment.

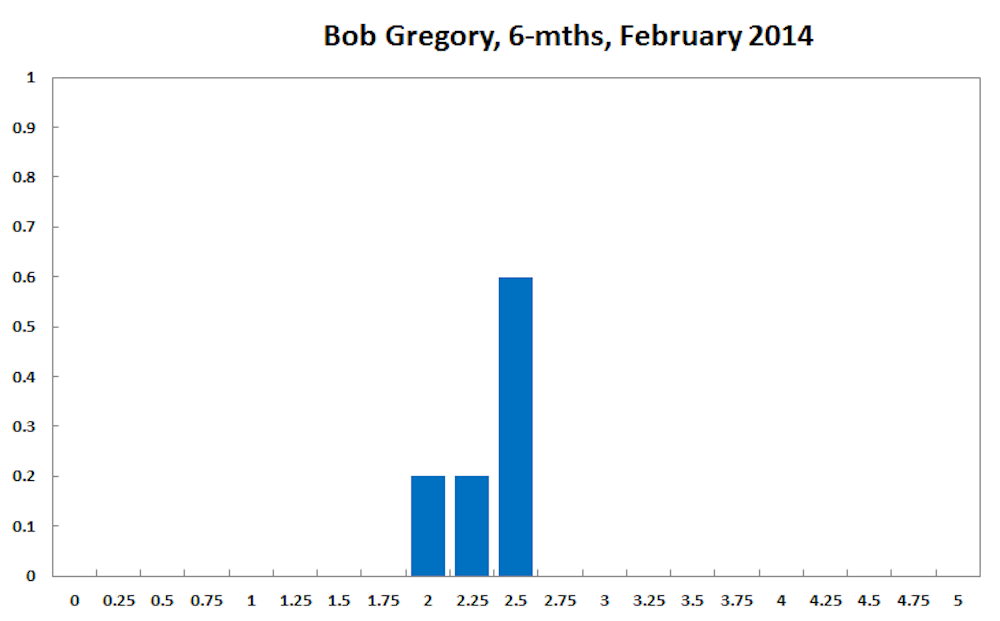

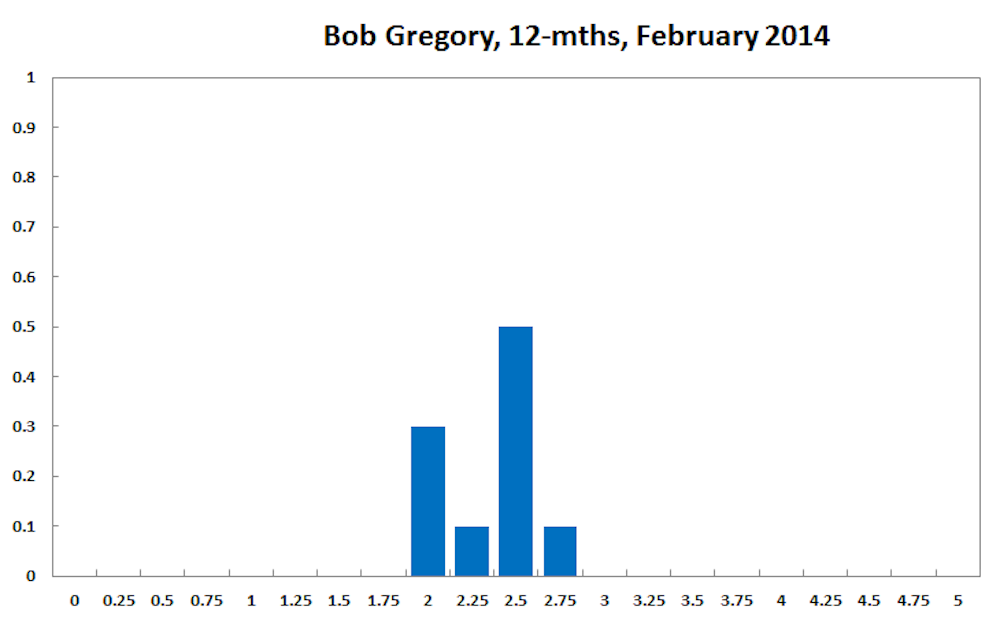

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology:

I am becoming more uncertain, not about the range of possibilities, but what probability to attach to each one. Have a clear view on the economy - it is sliding down slowly. But interest rates have a high relative content - that is relative to overseas and I think overseas interest rates will begin to go up. So if we stand still it is like a cut, from the RBA view.

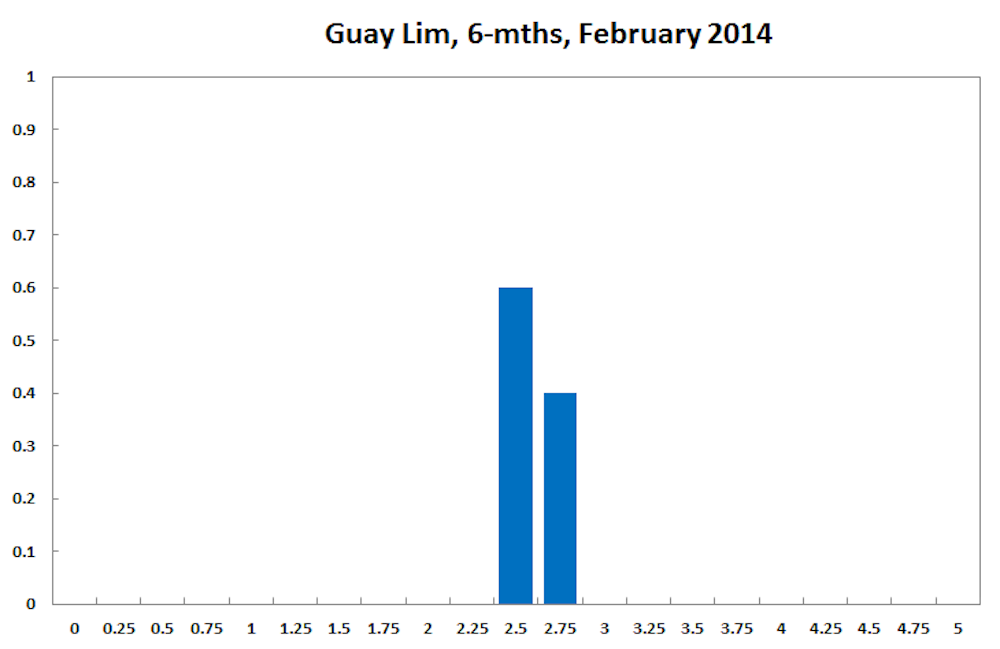

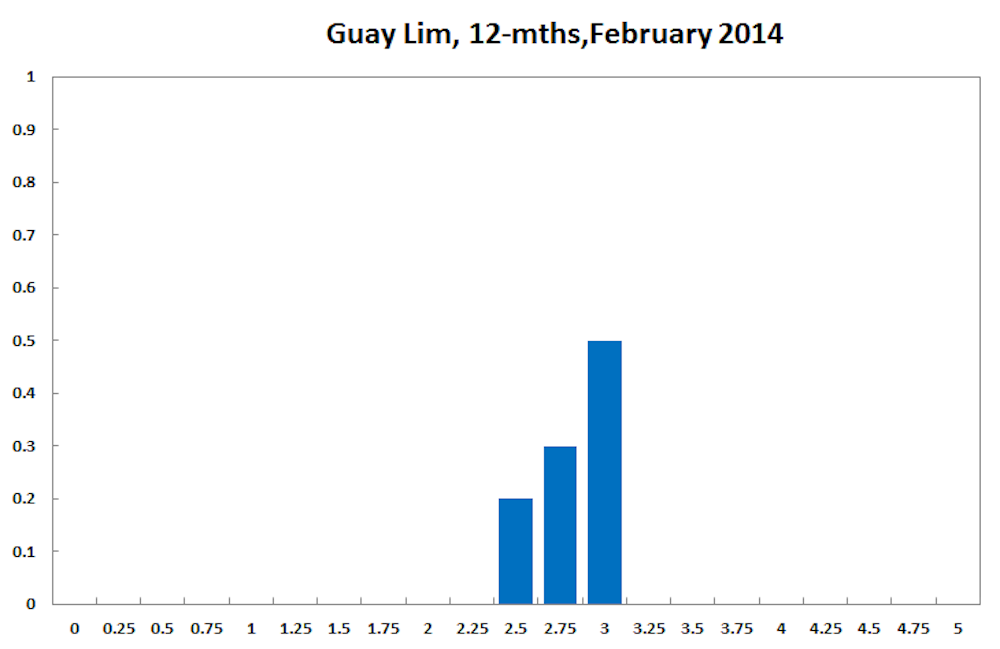

Guay Lim, Professorial Research Fellow and Deputy Director, at the Melbourne Institute of Applied Economic and Social Research, Melbourne University

No comment.

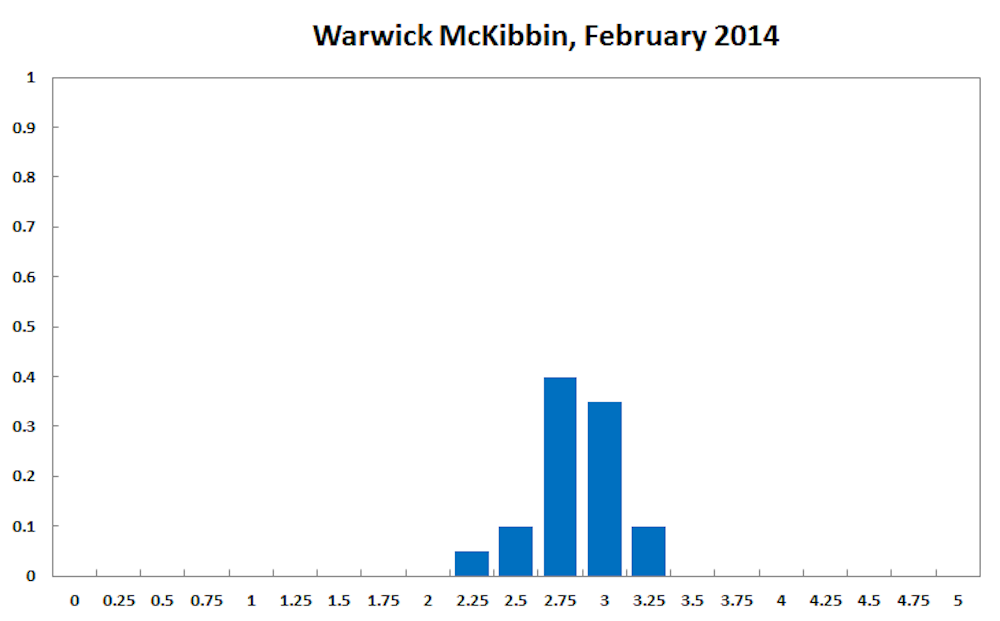

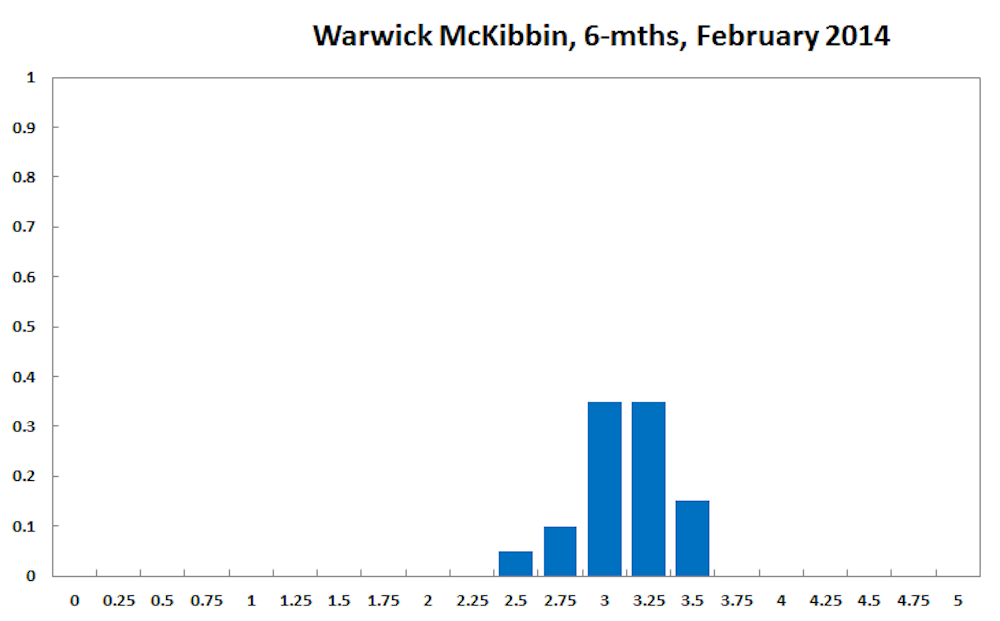

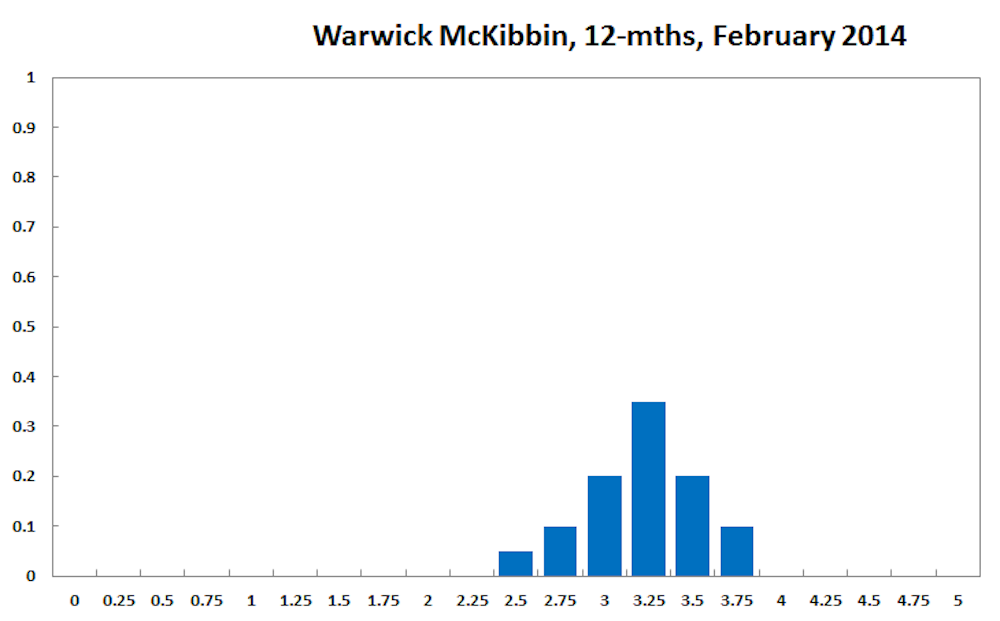

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

No comment.

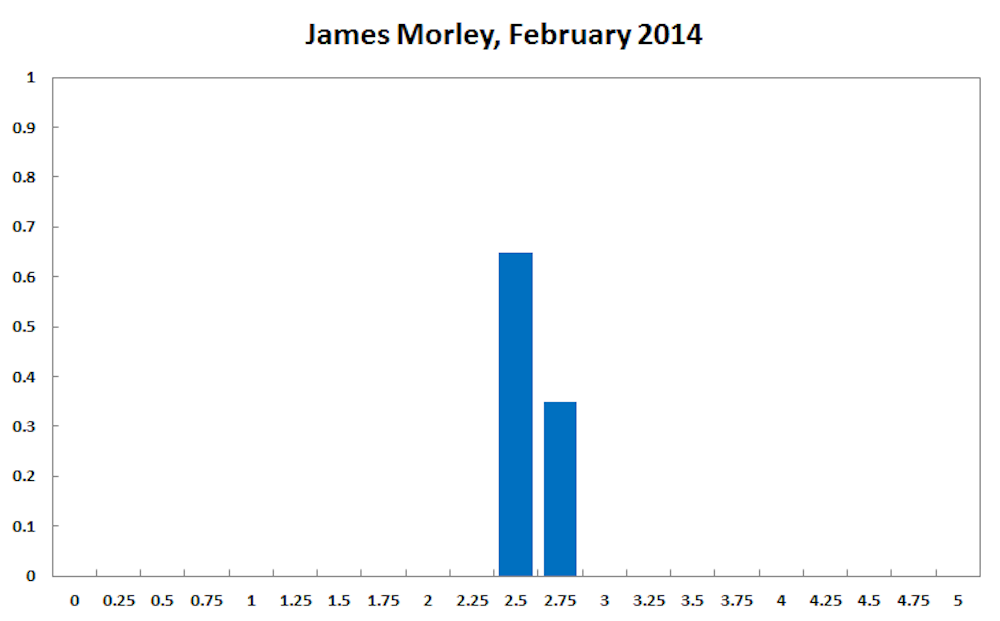

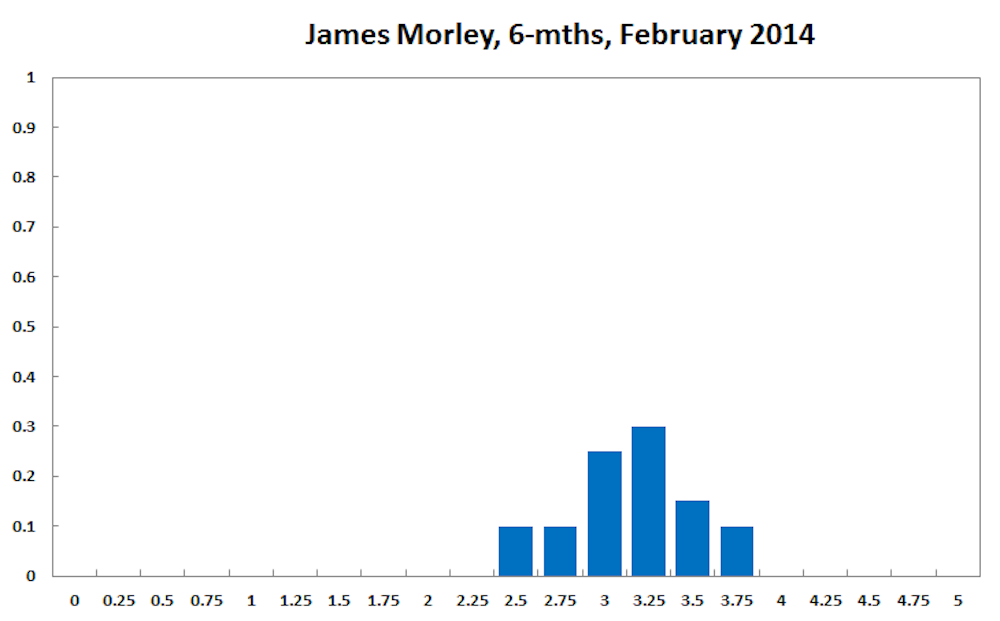

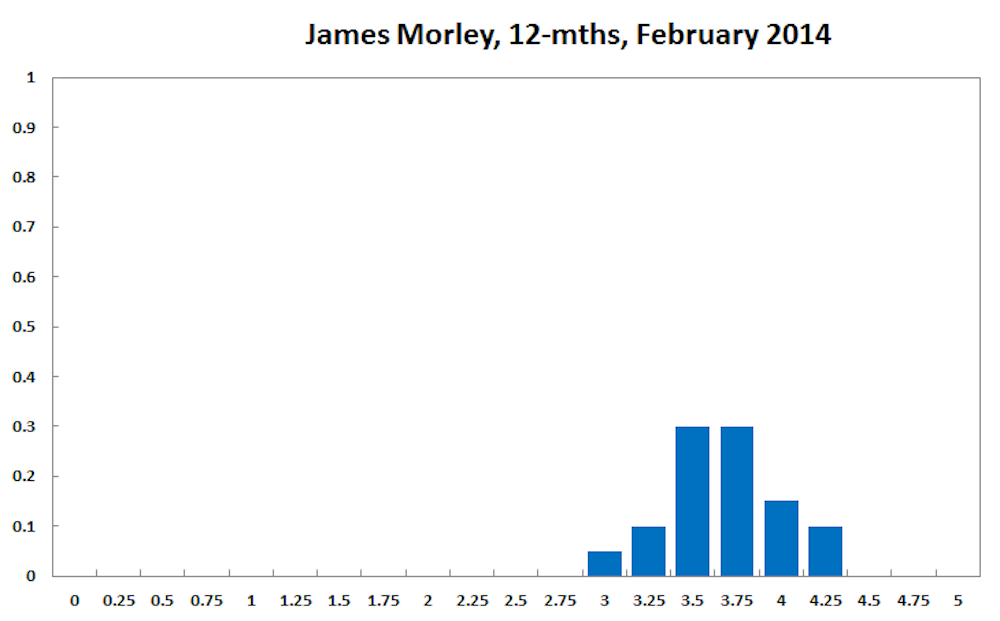

James Morley, Professor, University of New South Wales, CAMA:

Inflation for 2013 was 2.7%, which is slightly above the mid-point of the 2-3% target range. However, this is likely due to one-time effects of the depreciation in the Australian dollar from its record highs against the US dollar. As a result, inflation can be expected to run at the lower end of the target range in 2014 unless the dollar depreciates a lot further.

The policy rate should be returned to its neutral level over the medium term of one to two years. However, the RBA can continue to monitor the effects of low real interest rates on asset and housing prices before embarking on a tightening cycle.

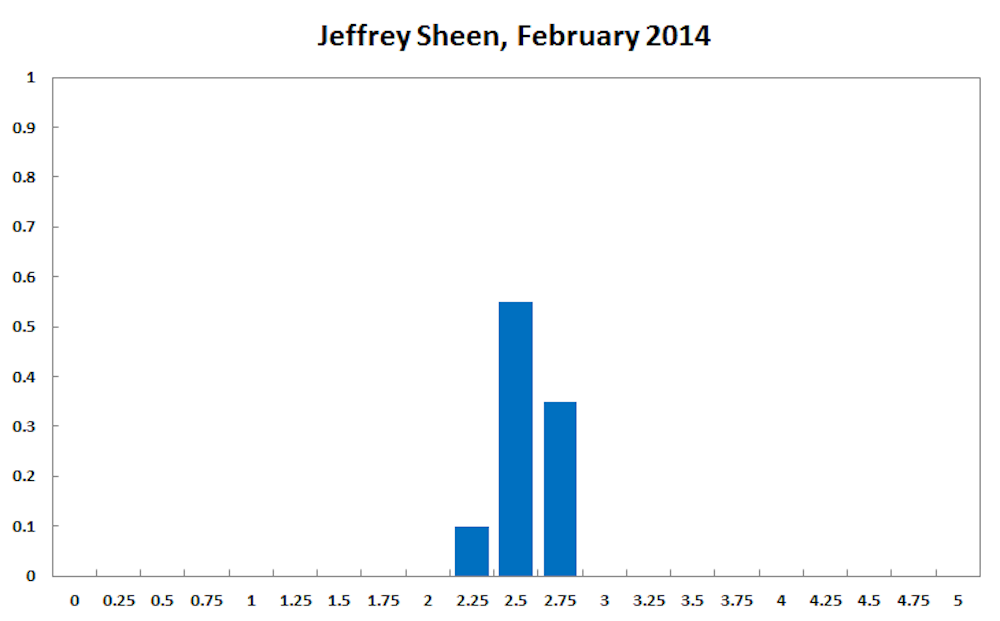

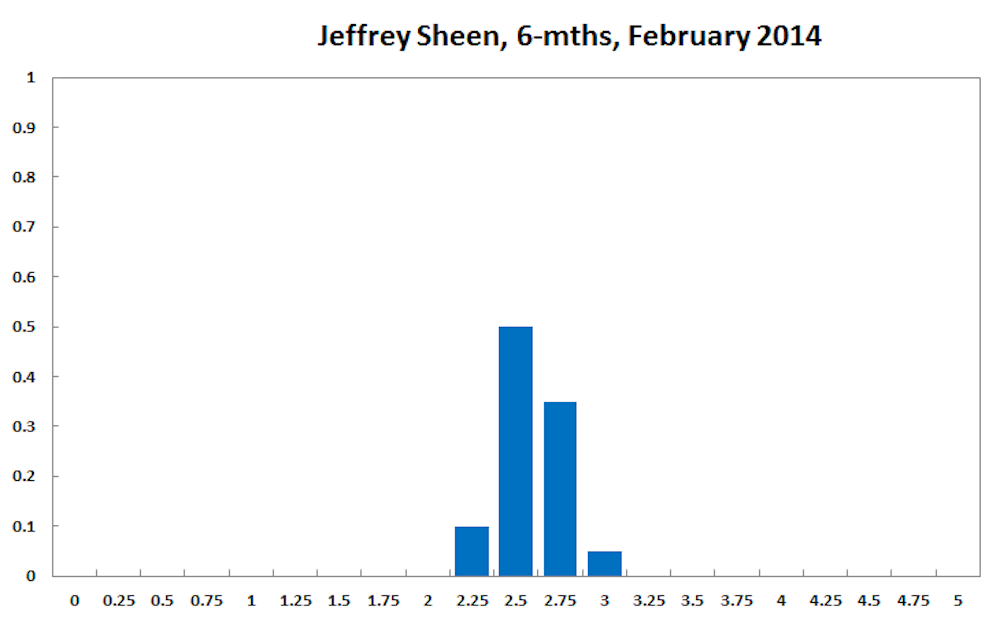

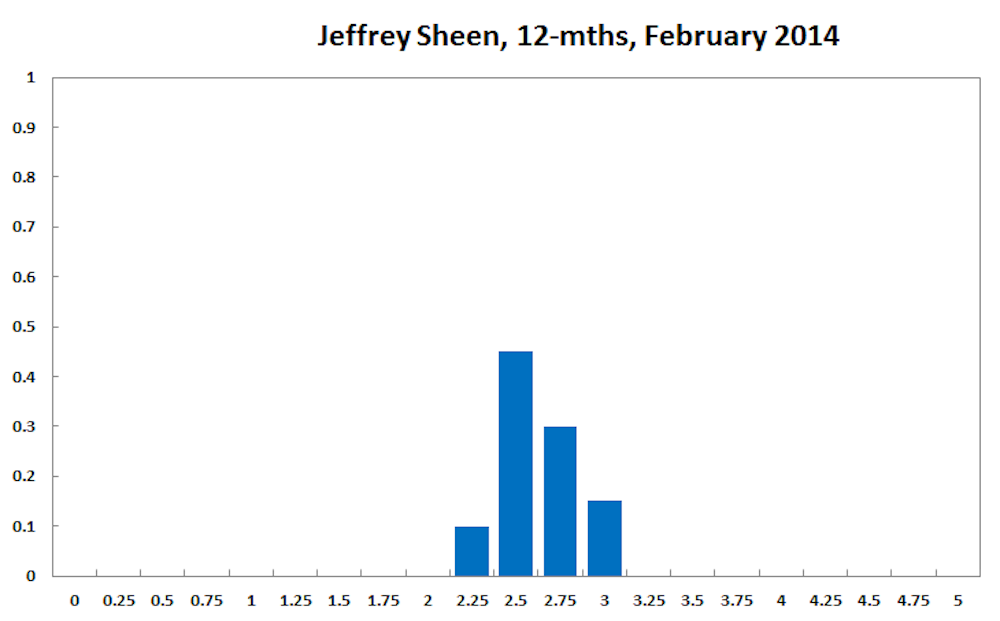

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

Since the last RBA board meeting, the Australian economy has continued to flatline. Its major trading partners improved their growth only modestly, and it seems now that this trend will persist for some time. The trade weighted index has depreciated only a little. On the other hand, housing and share prices in Australia have continued to rise significantly, in part reflecting investor confidence about the future.

However, in the present, economic activity appears restrained and capacity utilisation is falling slowly. While the impact of changes to fiscal policy settings by the Abbott government remain unclear, consolidation in 2014 is quite likely. Therefore a zero real value for the cash rate seems appropriate for now.