In early June the international debt rating agency Standard & Poor’s granted a stay of execution by not downgrading the South African government’s IOU certificate to a “junk debt” status.

This preserved the country’s credit worthiness as investment grade. South Africa should therefore be able to keep on sourcing external finance at a relatively affordable cost.

But Standard & Poor’s maintained a negative view of South Africa’s economic prospects. Moody’s passed a similar verdict last time it revaluated the country.

The close shave should be an opportunity for government and all stakeholders to step back and reflect on the averted economic calamity. In a sedate and panic-free mindset they can begin to set the economy and its management on a transformative growth path.

What went wrong

How did South Africa earn this negative outlook and why is it teetering on the precipice of a downgrade?

A reasonable explanation for the current state of affairs can be found in a combination of factors. These include:

a drop in commodity prices. This has had a significant impact on a major source of foreign exchange earnings;

a disruption in production due to industrial action by labour unions that has been badly managed by all concerned: the private sector, union leadership as well as government; and

the troubling mixed signals the country’s leadership has been sending to the nation and the world on effective governance.

These are factors over which the country can exercise control.

The protracted labour strikes and questions around governance are particularly responsible for the rating agencies maintaining a negative outlook. In my view these factors, alongside growth-oriented structural reforms, are standing in the way of the country getting onto a long-term sustainable growth path.

Government responds with band aid

The government revealed its strategy for dealing with the dim economic state that precipitated the threat of downgrade in its most recent budget. It was the usual response of austere posturing made up of a concoction of measures. These included government spending cuts, a civil service job freeze and increases in revenue by hiking “sin taxes” on alcohol, tobacco, sugary drinks, fuel, environmental degradation and capital gains.

These measures amount to nothing more than band-aid treatment. The rating agencies weren’t fooled by the budget measures. This is because they know that South Africa’s economic fundamentals are not that bad: the issue is the country’s future prospects.

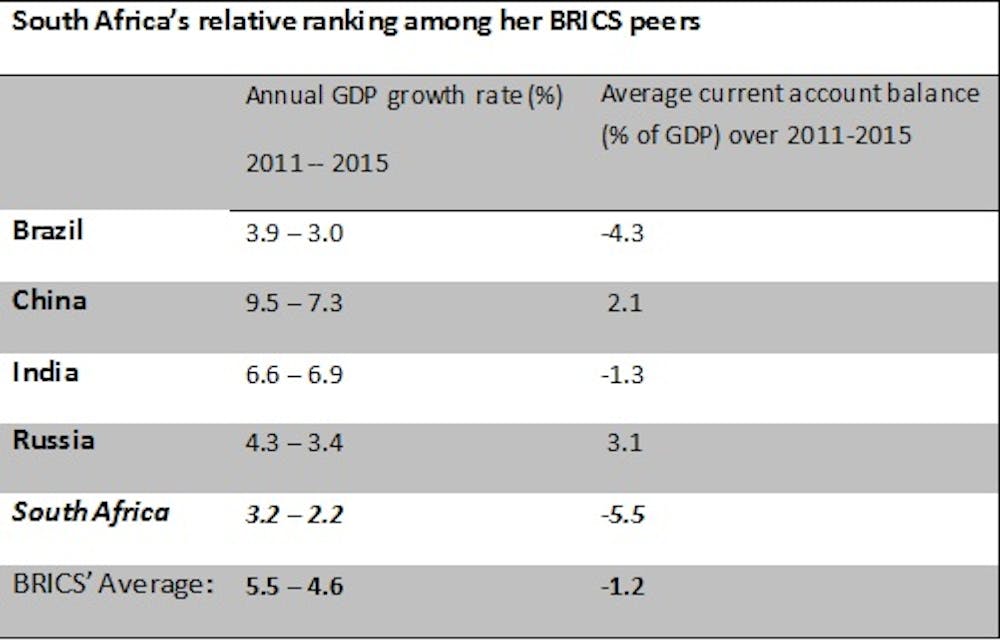

This is best illustrated by comparing South Africa with its BRICS peers (Brazil, Russia, India and China) in terms of some of the metrics reflective of a country’s credit worthiness. It in fact doesn’t fare too badly.

The ratio of public debt to gross domestic product of Brazil and India are in the 60% range, way higher than South Africa’s 50% ratio. Of this only about 10%-20% (of total national debt) is attributable to external debt, the lowest among its peers except China. Its tax management system and financial system infrastructure rank highly among emerging-market countries.

Its main areas of dubious distinction are in the economic growth and current account deficit comparisons. This is where it lags behind most of its peers. South Africa has historically recorded the lowest growth rate among its peers, with a projection that this year’s may be in the range of 0.9%-1.7%. Its current account deficit is again the worst, with a five-year average of -5.5%. This is generally considered a red flag to fickle foreign investors thinking of exiting.

How the threat can be averted

The main thrust must be to grow the economy rather than imposing willy-nilly spending cuts and fixating on taming inflation.

The increase in revenue via “sin taxes” instead of income or profit tax is wise. But a much less burdensome revenue source would be to stop the illicit flow of funds out of the country. Global Financial Integrity estimates that the leakage of funds from South Africa, mainly from multinational corporations, was R330 billion per annum (about US$21.6 billion at current rates) between 2004 and 2013.

One major contributor is transfer pricing by multinational firms. Transfer pricing is when a company, seeking to avoid taxes, can make its profit/loss record show loss. This is achieved through increased expenses by fictitiously providing inputs/parts/advice to a branch in another country. By falsely reporting a loss it cheats the South African government of taxes it would have rightly paid on its true profit.

Other steps that could be taken, especially on managing the damaging recurring strikes, include:

firms extending profit sharing fairly. This can be done by increasing the salaries of line-workers or by giving workers equity share-based wage increases;

the enforcement of black economic empowerment measures to redress the destructive legacy of apartheid; and

unions sensibly and nonviolently demanding fairness by negotiating in good faith.

In addition, the government should pay more attention to decoupling revenue and, by extension, the budgetary process and economic growth, from commodity price volatility. This can be achieved by government building “rainy day” reserves. Taxes, or a royalty tax, could be imposed when commodity prices rise beyond a certain level. The funds can be used for important ongoing capital and social projects (such as maintaining or growing the national productive capability via strategic funding of education) during economic downturns.

The country should also institute economic management mechanisms such as creating a sovereign wealth fund for capital investment planning. This should be used for macroeconomic stabilisation and expanding the production base. Countries that have done this successfully include Norway, Kuwait and United Arab Emirates.

On top of this South Africa must begin to use its superiority in manufacturing capacity and services such as banking and information and communications technology, to grow intracontinental trade.

The issue of job creation must also be given a serious rethink. And careful consideration of ownership structures is particularly germane given the lingering legacy of apartheid. But privatisation of all activities is not a cure-all. For example, government may not need to run an airline business. This can be handled by the private sector or through a public-private partnership. On the other hand it certainly can insist on having a say in rail transport, electricity and water.

These production activities affect most households in terms of price affordability and employment.

Finally, to address concerns about corruption and state capture the government needs to adopt a servant-governance approach by strengthening institutions and ensuring their independence from political influence.

If pursued diligently, these measures would save South Africa from what currently looks like constant danger of a downgrade.