The Conversation is fact-checking claims made on Q&A, broadcast Mondays on the ABC at 9:35pm. Thank you to everyone who sent us quotes for checking via Twitter using hashtags #FactCheck and #QandA, on Facebook or by email.

… This nation, when you look at what we give in the form of tax concession, tax subsidy on negative gearing and capital gains tax discount, is spending more at the Commonwealth level on negative gearing and CGT discount than we are on child care or higher education. – Opposition Leader Bill Shorten, speaking on Q&A, June 13, 2016.

Opposition Leader Bill Shorten told Q&A viewers (watch from 6:26 in the clip above) that the federal government spends more on negative gearing and capital gains tax discounts than it does on child care or higher education.

Is that right?

Checking the source

When asked for sources to support Shorten’s statement, an ALP spokesperson said the Grattan Institute has estimated the cost of the capital gains tax and negative gearing concessions at $11.7 billion per year.

The Treasury’s tax expenditure statement (TES) lists the cost of the capital gains tax discount as $6.15b for 2015-16. The TES does not list the cost of negative gearing, but using Grattan’s total figure and subtracting the value of the capital gains tax discount, this shows that the cost of negative gearing is around $5.5 billion… this cost exceeds the cost of child care assistance or university education as per the budget papers.

You can read the longer response here.

So, does federal government spending on child care or higher education outstrip the cost of revenue forgone due to negative gearing and capital gains tax (CGT)?

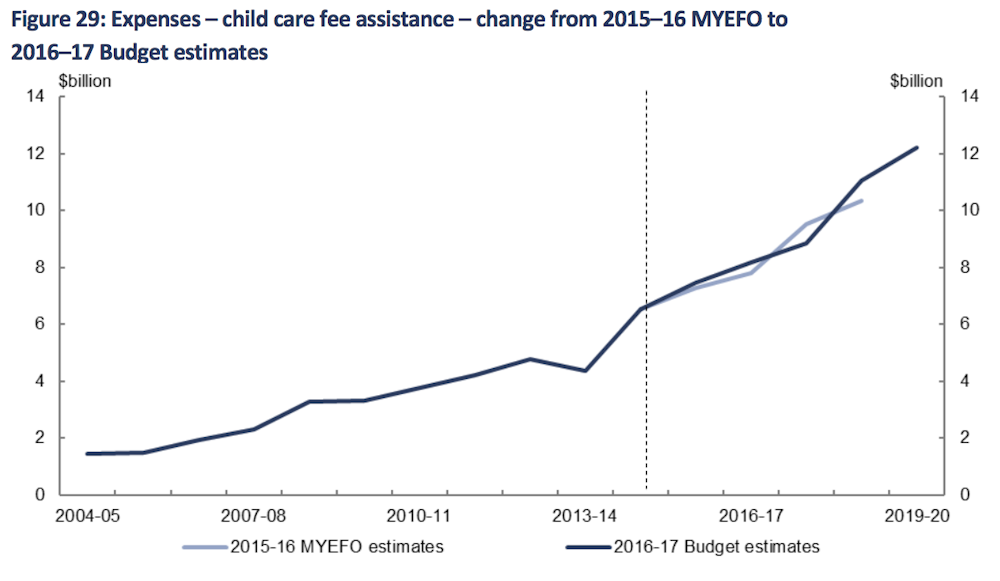

How much does the government spend on child care subsidies?

This year’s budget showed the federal government is estimated to spend about $8.2 billion on child care fee assistance in 2016-17. That’s comprised of about $4.2 billion for the child care benefit and about $3.9 billion for the child care rebate.

Here’s a graph produced by the Parliamentary Budget Office showing how the cost of child care subsidies is projected to change over time.

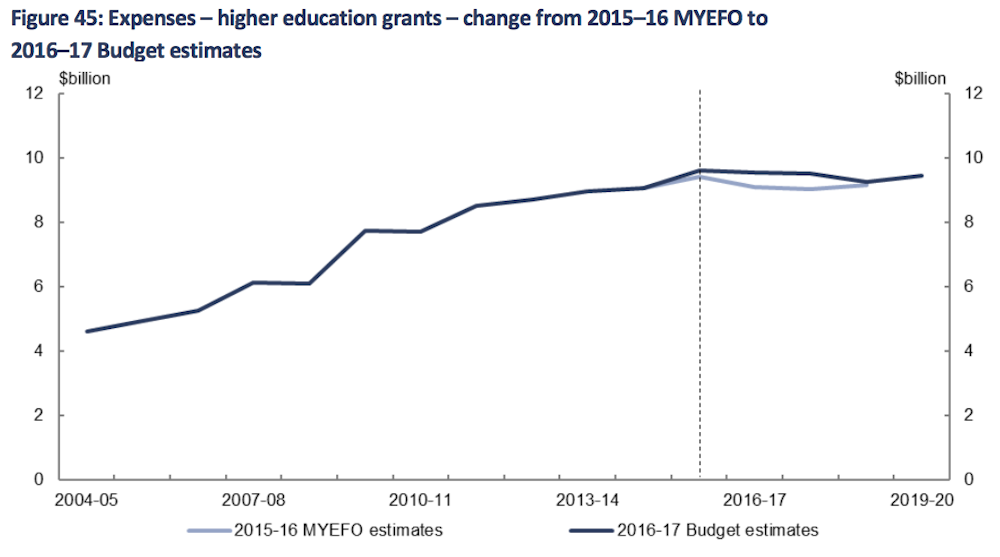

How much does the government spend on higher education?

This year’s budget shows that the federal government is estimated to spend about $9.5 billion on higher education in 2016-17, an amount which is fairly stable over the forward estimates period. It is projected to be about $9.4 billion by 2019-20.

Here’s a graph produced by the Parliamentary Budget Office showing how the cost of higher education expenses is projected to change over time.

How much do negative gearing and capital gains tax concessions cost the government in revenue forgone?

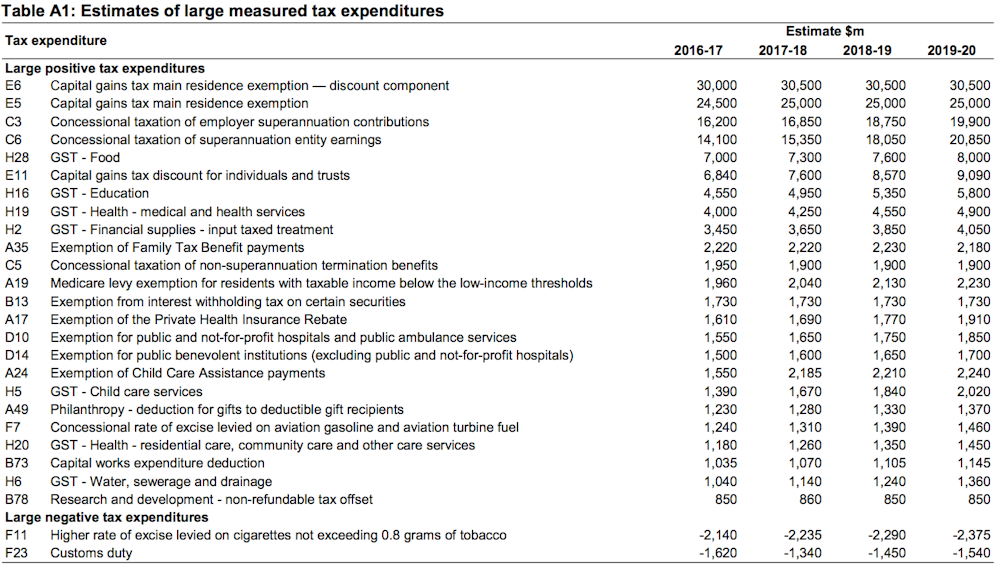

Capital gains tax: As Labor’s spokesperson says, the Treasury’s 2015 tax expenditure statement (TES) lists the cost of the capital gains tax discount as $6.15 billion for 2015-16.

According to Treasury’s estimates of tax expenditures, the “cost” associated with the capital gains tax discount for individuals and trusts is estimated to be $6.8 billion in 2016-17, rising to $9.09 billion in 2019-20. Note that this estimate does not include any estimate for the concessional treatment of owner-occupied housing.

Negative gearing: This is where it gets tricky. Treasury does not regard negative gearing as a “tax expenditure” and thus does not provide any estimates for the “revenue foregone” as a result of it. So we have to look at other sources for estimates.

Labor has inferred from the Grattan Institute’s report that the cost of negative gearing is around $5.5 billion ($11.7 billion minus the $6.15 billion cost of the CGT discount).

Labor did not provide The Conversation with any Parliamentary Budget Office (PBO) estimates on the cost of negative gearing to The Conversation. Labor’s spokesman said only that the PBO estimated Labor’s plan to restrict negative gearing to new property and to halve the capital gains tax discount could raise $565 million over the forward estimates.

The Greens put the cost of negative gearing at somewhere around $4 billion a year.

A 2015 report by The Australia Institute said that modelling by National Centre for Social and Economic Modelling (NATSEM) estimated that:

negative gearing of residential investment property is currently reducing tax revenue by $3.7 billion per year.

Ben Phillips, Associate Professor at the ANU Centre for Social Research and Methods (who previously conducted the NATSEM modelling quoted by The Australia Institute), reported in February 2016 that:

We estimate that in 2017-18 the total tax savings from negatively gearing properties is $4.3 billion.

And I have previously estimated that negative gearing costs more than $5 billion per annum in revenue forgone – although that estimate was for the 2010-11 financial year when interest rates were considerably higher than they are today. It was also a “gross” figure that did not allow for the impact of interest expenses being carried forward to be offset against future capital gains tax liabilities.

So what’s the combined cost of negative gearing and CGT? Nobody knows for sure. It could be as high as $11.7 billion, as the Grattan Institute has said. It could also be lower.

So does CGT and negative gearing cost more than child care or higher education?

This year’s budget showed the federal government is estimated to spend about $8.2 billion on child care fee assistance and about $9.5 billion on higher education in 2016-17.

Using the estimates outlined above, the combined annual effective cost of negative gearing and capital gains tax discounts to the public purse in revenue foregone is somewhere between about $9 billion and $11.7 billion (although no-one knows for sure because of differing opinions on the cost of negative gearing).

So Shorten’s statement that Australia is “spending more at the Commonwealth level on negative gearing and capital gains tax discounts than we are on child care or higher education” is likely to be somewhere in the ball park – but it’s impossible to say conclusively.

A word of caution

It’s worth remembering that none of the major parties are advocating scrapping negative gearing altogether.

And finally, it is worth drawing attention to Treasury’s caution that its estimates of tax expenditures such as the capital gains tax discount assume that taxpayer behaviour is unaffected by the existence of the concessional tax treatment. That assumption that may not be valid in practice, so that these estimates:

do not indicate the revenue gain to the budget if specific tax expenditures were to be abolished…. care needs to be taken when comparing tax expenditures with direct expenditures as they may measure different things.

Verdict

Is Australia “spending more at the Commonwealth level on negative gearing and capital gains tax discounts than we are on child care or higher education”?

Nobody knows for sure, because of the difficulty in measuring exactly how much negative gearing tax breaks cost the federal government every year in revenue foregone. (Treasury cautions against comparing tax expenditures with direct expenditures as they may measure different things.)

Using available estimates, however, Bill Shorten’s statement is probably in the ballpark. – Saul Eslake

Review

I agree with this assessment of the statement. There are official estimates on the projected spending on childcare, education and the revenue foregone in relation to the capital gains tax discount, although as Treasury notes these figures may not be directly comparable. It is more difficult to estimate the foregone revenue in relation to negative gearing as there are no official estimates. Each model will come up with a different estimate based on the parameters used for the estimate.

I would also caution that the statement by Bill Shorten should be read in conjunction with proposed ALP policies in these areas. In particular, tax concessions on negative gearing and the CGT discount will be pared back but negative gearing will still be available to taxpayers currently holding investment properties, and the CGT discount will be halved but not removed.

Given the difficulties in identifying the cost of negative gearing and the problems inherent in comparing data measured differently, the statement is within reasonable estimates. – Helen Hodgson