There is little doubt that Kevin Rudd’s plan to bring forward international linking and trading of emission permits is a smart political move. It removes a key option for Tony Abbott.

Now Mr Abbott is forced to apply the most extreme interpretation of his promise to remove the carbon tax: remove all pricing mechanisms. Until now, many commentators have pointed to the vague wording of his promise to argue that bringing forward the internationally linked trading scheme would be an obvious path for him after winning the election.

This puts many Liberal-leaning businesses in an awkward spot: they were betting on this option. Most business people know we will have a price on carbon at some point. They also know that right now they have the best deal they’ll ever get. In a future scheme, the target would be tougher, the carbon price would be higher and the present generous concessions would be reduced or removed. They also want certainty, and dumping carbon trading now will just continue the uncertainty regarding when, and in what exact form, carbon pricing will be reintroduced.

But the proposed shift complicates progress on reducing emissions. All other things being equal, the expected lower carbon price will reduce the incentive to cut emissions. But it’s a lot more complicated than that. Carbon policy operates within a context of other markets and the signals they send.

Even today’s carbon price has been a relatively small contributor to increasing electricity and gas prices. So the ongoing decline in National Electricity Market electricity use is being driven by multiple factors that are not affected by the carbon price.

In recent years, an increasing number of businesses, both big and small, have discovered they can cut their emissions at a profit by investing in energy efficiency and smart energy management. The top 250 energy-using businesses in Australia are saving around a billion dollars each year at a carbon cost of minus $95 per tonne, according to the recent ACIL-Tasman review of the Energy Efficiency Opportunities Program.

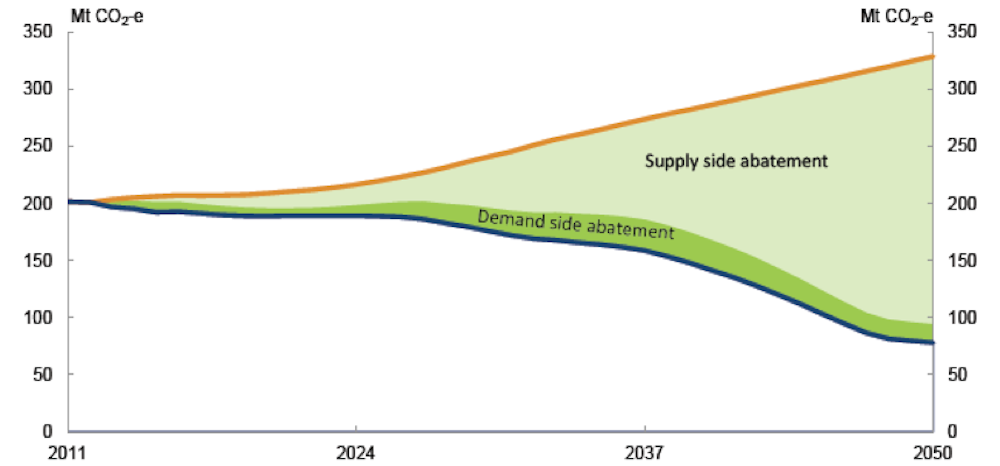

Many businesses are taking advantage of funding from the carbon scheme revenue to capture energy efficiency benefits, too. Economic modelling of the impact of energy efficiency improvement has been seriously underplayed in Treasury modelling, as shown in Figure 1. Treasury thinks that most electricity related abatement will be due to a shift from coal to renewables and gas generation, while “demand side” energy efficiency will be minor. In contrast, the International Energy Agency, in its World Energy Outlook 2012, estimates electricity savings by end users (much of which has a low or even negative carbon cost) will be roughly equal to supply-side abatement. So future carbon costs have been overestimated by Treasury.

Discussion of the impacts of high carbon prices has also failed to understand the fundamentals of the scheme’s operation. For example, Treasury expects the greenhouse intensity of Australian electricity to decline by more than three-quarters by 2050. So the carbon cost on a unit of electricity in 2050 would be the same as today if the carbon price quadrupled in real terms. Further, if we become, say, twice as efficient, we would only have to buy half as much electricity to run our appliances or industrial equipment.

So fear-mongering about future high carbon prices is simply a political game, playing on people’s ignorance of how carbon trading works.

Will a lower carbon price actually affect abatement? No-one really knows. In recent years we have seen a shift from coal generation, driven not just by the carbon price, but by factors such as the need for flexible peaking plant and the ability of renewables to displace conventional generation by offering power to the National Electricy Market at lower prices.

Also, we must consider whether the lower carbon price would influence investors in high-emission energy supply and industry. We are seeing emerging pressure on investors to divest their investments in high-emission industries and fossil fuel production, due to the fundamentals of climate science: the carbon bubble. Investors must look to the long term returns when committing to major projects: the present situation is very risky.

On the other hand, linking our carbon price to the international level means we lose the flexibility to manage our carbon price for the greatest benefit and become vulnerable to the flaws of global trading schemes. And a low price means there is less revenue to invest in accelerating abatement.

Despite the deeply held beliefs of many policy makers and economists, carbon pricing need not be the “centrepiece” of climate response, although it is an important element. Driving emission-reducing innovation, incentives, regulation, and rewarding voluntary abatement action can all be very powerful. Over a million Australian households are now green electricity generators, and increasing numbers of businesses are benefiting from abatement. Momentum for major reform of electricity markets is building. Government could even introduce separate niche carbon trading schemes in addition to the core scheme, along the lines of the Carbon Farming Initiative.

Overall, while a lower carbon price reduces the incentive for emission reduction, its impact may be offset by a reduction in emphasis on pricing as the silver bullet, leading to stronger action of other kinds. Also, emerging trends towards energy efficiency and renewable energy, and strengthening perceptions of risk by potential investors in fossil fuels are accelerating emission reduction.