With several weeks having passed since the introduction of the carbon tax, the place to look for the most immediate effect is in the national wholesale electricity market known as the NEM.

It’s early days yet, but NEM prices are certainly up. To what extent can we attribute the rises to the carbon tax? And will the sky fall in?

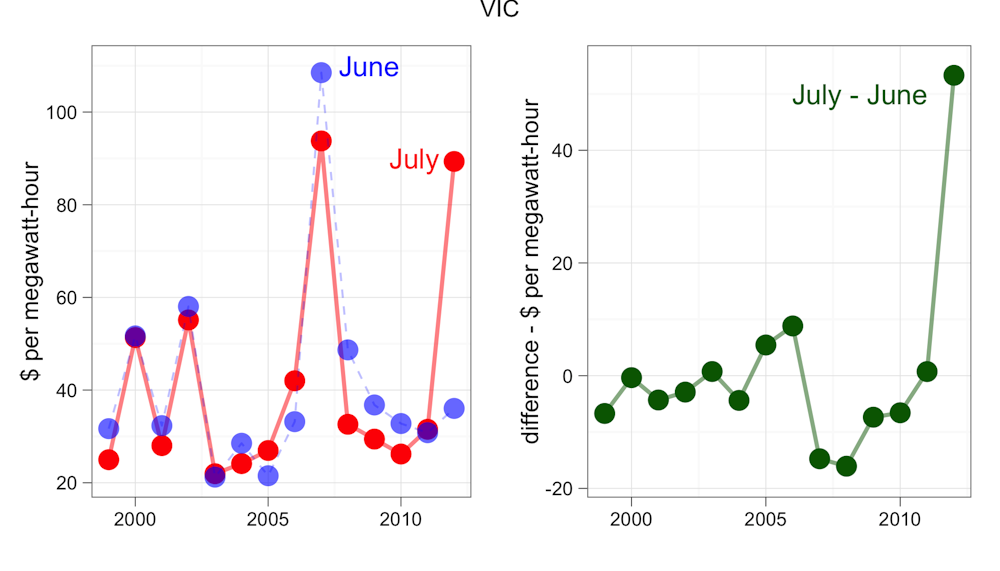

If we compare the NEM prices over the first two weeks of July with previous years we see a surprisingly large rise. For instance, in Victoria the early July 2012 prices were up by about $60 on the same time period for each of the previous three years.

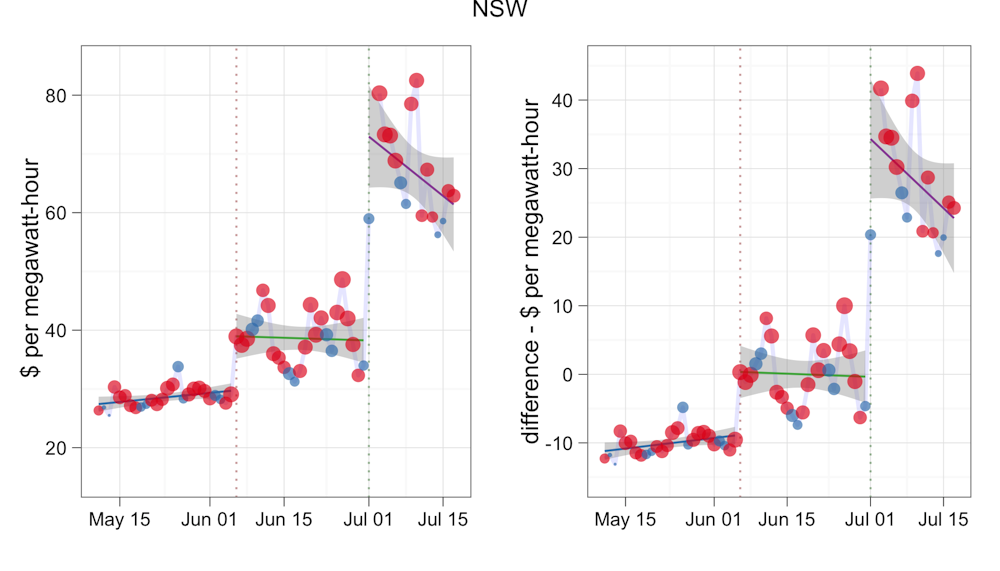

New South Wales and Queensland prices were also up, but not quite so much at about $40 each.

With wholesale prices varying for a range of reasons, on timescales from the seasonal to the hourly, a better comparison maybe between time periods immediately pre- and post- carbon tax implementation.

Victorian prices in the first two weeks of July were up about $50 on the first two weeks in June in 2012. In both New South Wales and Queensland the price differential was about $35. In South Australia it was almost $60.

Given that about one tonne of CO2 is generated for about each megawatt-hour of coal-fired power, these price jumps are significantly more than expected for a $23 per tonne carbon price.

So what gives?

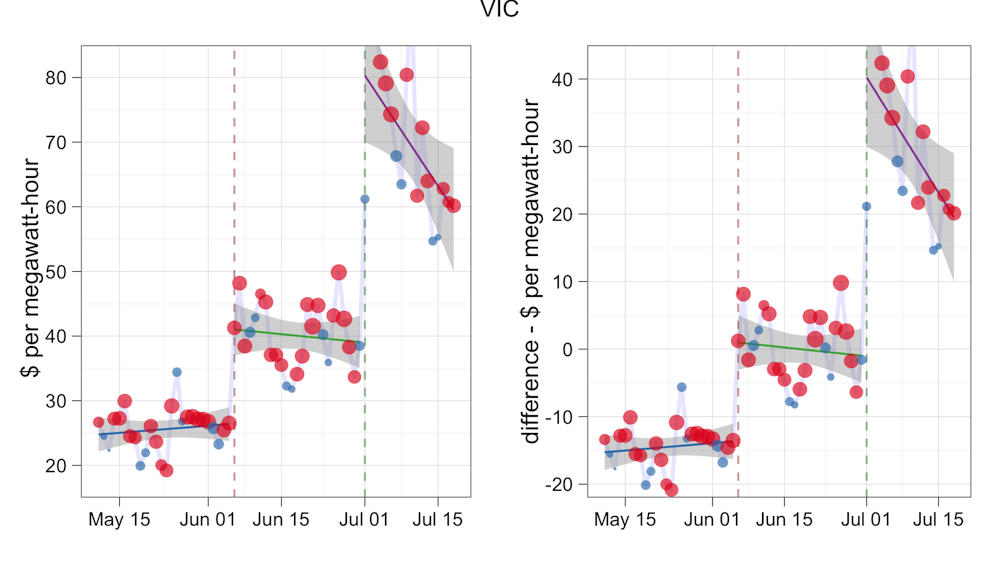

To work out what is going on, it’s useful to look at how average daily prices have changed over the last two months.

Up until June 6th, daily prices averaged between $25 and $30 per megawatt-hour across the NEM. On June 6th prices jumped by around $10 across all NEM jurisdictions.

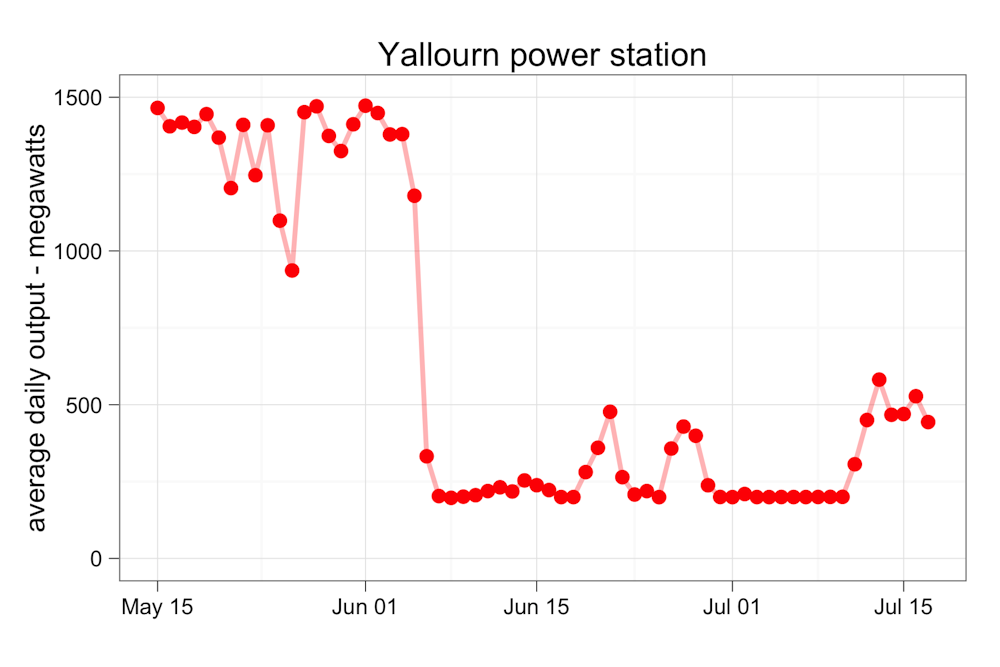

That price jump was largely due to the reduction in output at TRUenergy’s Yallourn power station following the Morwell River diversion collapse on June 6th. The flooding in the open-cut mine and damage to the conveyor system that delivers coal to the power station caused power output to reduce by over one gigawatt.

You might think the effect would have been largely limited to Victoria. However, interstate power flows allow the price signals of such outages to propagate right across the NEM. In fact, there was little difference in the price impact of the Yallourn outage between Victoria and the other mainland states connected to the NEM.

If we factor out the price impact of Yallourn, we see the price hike in early July was initially about $35-40 per megawatt-hour. However prices have dropped back considerably since the first week of July and are now only about $25 above late June prices. And the trend still appears to be heading downwards.

The initial carbon price hike at the beginning of July seems to have been a bit of an overshoot. Perhaps the generators were being somewhat “conservative” in their bidding strategy in the brave new world of carbon pricing. If so, market forces appear to be quickly pulling them back into line.

If and when Yallourn comes back to full prodcution, we could expect prices to drop back another $10 or so, and settle at around $50-$55 per megawatt hour. In a historical context, that not much more than the $47 annual wholesale price averaged over the last 10 years when adjusted to 2012 dollar terms.

In the bigger picture, the overall impact of the carbon tax will have been significantly cushioned by the very low wholesale prices over the last few years. Those low prices reflect the general state of oversupply on the NEM as discussed in my last post.

In spite of the issues at Yallourn, and the impost of the carbon tax, wholesale prices have not yet reached the heights of the winter of 2007, and do not look like doing so. The sky didn’t fall in 2007 and won’t be doing so now. Unless of course we have another Yallourn-like incident on the NEM.

Wholesale prices are up, but the trend in prices since early July suggests they will stabilise at only a few dollars above the long-term average adjusted wholesale prices. And that is with the cost of the carbon tax.