Soon after the Great Recession, the U.S. stock markets plunged – and rebounded within 36 minutes. The Dow Jones Industrial Average dropped more than 9%, losing more than 1,000 points before suddenly recovering.

This May 6, 2010 event was the first recorded “flash crash.” While it didn’t have long-term effects, it raised concerns among investors about the stability of stock market.

Computers have made trading faster and more efficient, but they also can create instability in the markets. Today, quantitative analysts use complex algorithms to make many trades in many markets within a fraction of a second. These new algorithms now account for more than half of all trades. But this may lead to even more flash crashes.

As engineers, we were interested in that May 2010 crash. No single reason can explain why flash crashes happen. But are there ways to predict and mitigate these anomalies? We took on the challenge of developing a theory that may help predict flash crashes.

The flow of markets

We started with fluid dynamics, the study of the flow of fluids such as water. These principles can be applied to other problems; one of us previously used fluid physics to examine the movement of traffic.

In fluid dynamics, researchers look at how measured quantities, like velocity and pressure, affect the dynamics of the flow. For example, weather forecasters use the changes in wind speed and pressure to predict the movement of severe storms.

We asked ourselves: Could this science give insight into the dynamics of the stock market?

We felt that the existing theories predicting flash crashes are inadequate, because they focus on only a small part of the whole picture, like the performance of some subset of stocks. Dow Jones or the S&P 500 indices provide a limited amount of information about the market, by observing the behavior of a subset of appropriately chosen stocks.

Our approach was to include all the stocks in the market. In contrast, our model gives this information for almost the whole range of stocks, broken down by specific price ranges. All of these ranges can be simultaneously observed, generating an early warning.

We found analogues for the measurements that scientists typically use to understand flow. For example, for our model, the “density” of the flow was the number of stocks per unit price, and “pressure” was the upward or downward force on the price caused by the buying and selling activity of traders.

Observing stock markets from a computer screen, we could see that the movement of stock prices resembles the flow of a fluid like air or water.

Examining the flash crash

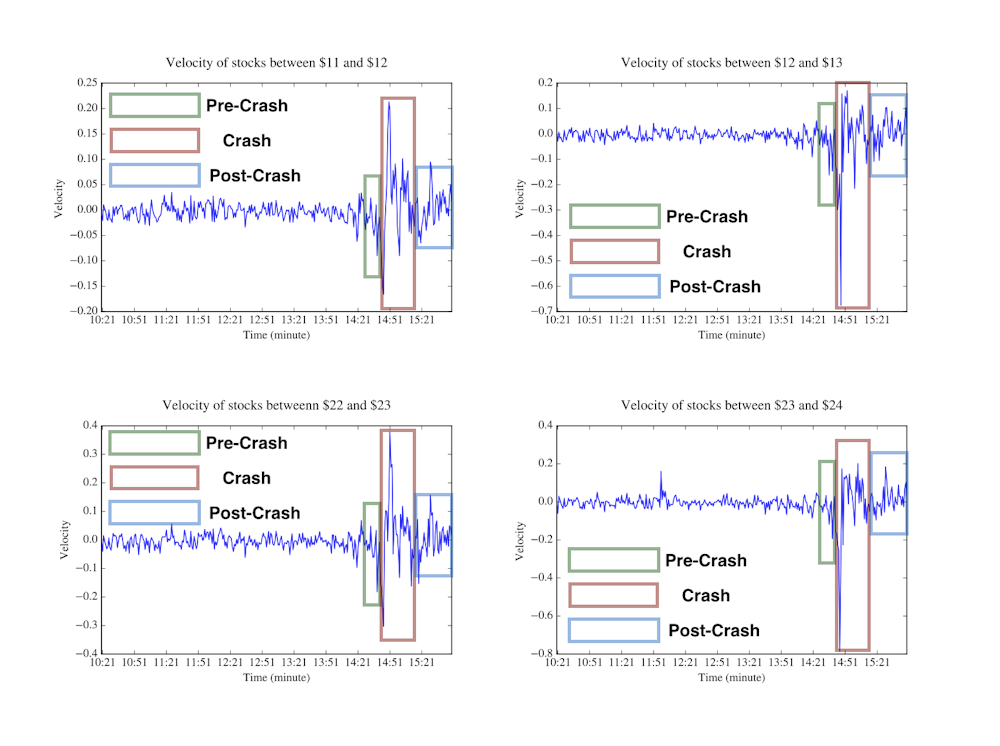

In our study, published on Sept. 1, 2018, we obtained price-per-minute data for about 4,000 stocks in the NYSE, NASDAQ and AMEX on the day of the May 2010 flash crash. We used these data to test our fluid dynamics model of the market.

When we looked at the prices of 700 stocks on the afternoon of the crash, we saw that the shock was clearly visible. The velocity graphs looked like the printout from a seismographic device monitoring shocks from an earthquake. Graphs of the pressure also clearly showed a major event at the flash crash time.

Looking at all stocks also gave us the ability to predict the near future of their behavior. Our model showed signs of a flash crash 10 minutes before the big event – before any issues would have been evident to human observers.

We have observed similar results from the model in the case of other crashes. For example, we studied Facebook’s initial public offering on May 18, 2012. The company raised about US$16 billion, but this massive offering was plagued by unexpected technical difficulties. The IPO was delayed for 30 minutes, causing turmoil across the markets for a few hours.

In our effort to analyze what actually happened on this day, we tested our model to see if it could observe signals prior to the offering time. The model showed a high volatile period that affected many stocks, creating chaos in the markets.

The next big crash

Our next step is to generate an intelligent system that will automatically consider the data and warn the overseers about the impending disturbances in the market. If this warning arrives early enough, investors could potentially use it to take preventative measures.

However, there are a few ways that the model still needs to improve. Relying on early signals can lead to false positives, which we want to minimize. Some of our recent results, not yet reported, suggest how many false positives and negatives occur.

In a different study, not yet published, we describe a system that analyzes trading days when abnormalities were reported. We have found that our system was able to produce low false positive and negative rates.

In light of these alarms, market regulators might then take the appropriate action. For example, they might prevent certain trades from being made or block particular traders from any activity for a period of time. Traders might choose to purchase shares at times when the stocks are falling in price, and sell during the times the prices are rising back to their precrash values. These actions might help reduce the crash’s impact.

In other words, investors could exploit the crash to improve their positions – and simultaneously help dampen some of the crash’s effects.