Liberal MP Andrew Robb has criticised the rise in public debt under the current Gillard government in a recent ABC radio interview. During the interview, Robb claimed growth in public debt was excessive and unsustainable, and accused Treasurer Wayne Swan of improperly representing the government’s current position on the public debt.

That public debt may constitute a problem is a familiar refrain from the conservative side of politics and economics. Many no doubt remember Howard and Costello’s incessant criticisms of the Keating government’s management of public finances when they took power in 1996, blaming them for being bad economic managers. The Coalition government certainly hasn’t let Labor forget this.

When discussing public debt, it makes sense to compare it to the size of the economy, or GDP (Gross Domestic Product). Quoting absolute figures is not sufficient to understanding the scale of any debt (see here for a bad example). GDP represents the size of a country’s income, though, of course, governments can only commandeer a portion of that income through taxation. The following figure displays the commonwealth government’s debt since Federation.

In its first decade, the government had no debt before piling it on to finance Australia’s involvement in World War I. The period 1914 to 1918 represented the largest growth period by far in federal government debt (the second largest occurred in 2009 to combat the effects of the Global Financial Crisis). Interestingly, debt decreased between 1931 and 1937 in absolute terms, certainly the incorrect policy response to an economic depression.

The ratio jumped once more due to World War II, to a record peak of 104% in 1946. A combination of solid repayment and strong GDP growth resulted in the rapid fall of the ratio to a low of 7% in 1974. The ratio would’ve likely fallen even further if not for the mid-1970s recession, requiring the government to debt-spend. The same again occurred during the early 1980s recession.

During the late 1980s, a massive commercial property (land) bubble formed, primarily in Melbourne and Sydney. It burst in 1989 due to the rapid escalation of interest rates to a nominal 18%. The resulting recession forced the Keating government to engage in a spending spree in an attempt to reduce the high unemployment during the early 1990s. Commonwealth debt peaked at 21% in 1996.

Once the Coalition gained power, again a combination of debt repayment and strong GDP growth saw the ratio fall to the lowest point on record, to 5% in 2007 (the Rudd government managed to lower it by a tiny fraction in 2008). Since the onset of the GFC, however, public debt expanded again under the Rudd and Gillard governments, to 16% in 2012.

A better measure of public debt is net rather than gross debt. The federal government doesn’t have liabilities alone; it also owns the debts of others. Subtracting this debt from the government’s shows net debt, which is always smaller than gross debt.

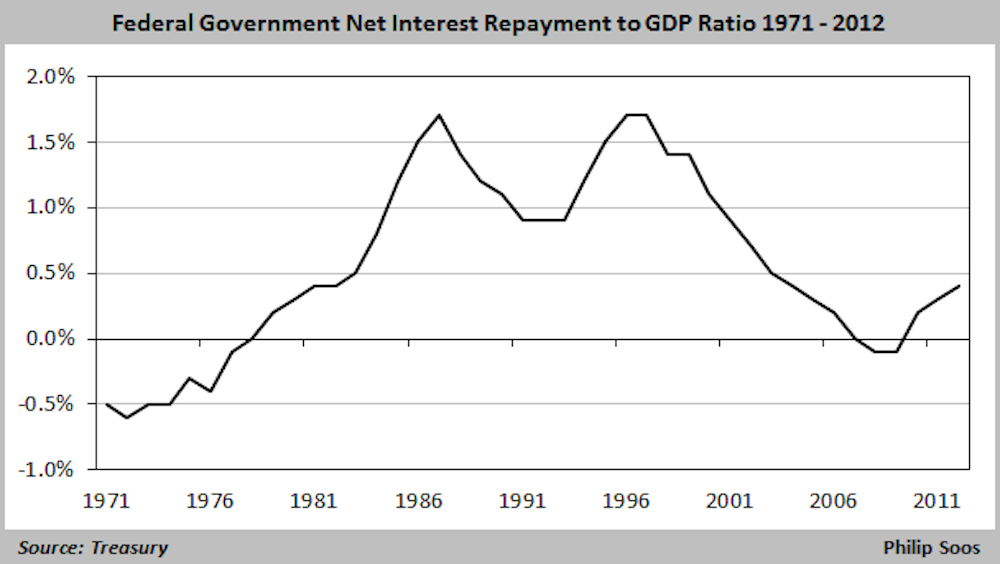

An even better indicator of the government’s debt position is its ability to service the debt - the net interest repayment burden - again expressed as a percentage of GDP. The gross or net debt to GDP ratio is not a perfect reflection of the government’s ability to finance its debt due to changes in interest rates at different times.

The following figure shows the net interest repayment burden peaked at 1.7% of GDP in 1987 and 1996, even though the gross and net debt to GDP ratios were higher in 1996 than 1987. The difference is due to higher interest rates during the 1980s.

What matters for countries with high levels of government debt is how high the net interest repayment burden is. This separates the US and Japan – countries with a relatively high level of government debt – from the basket-case PIIGS nations (Portugal, Italy, Ireland, Greece and Spain).

The federal government is currently in an excellent financial position. Even if the gross and net debt to GDP ratios were to rise, this does not necessarily translate into higher net interest repayments if the RBA further cuts interest rates from already historical lows and purchases government bonds. The federal government has one of the lowest debt burdens in the world.

Similar trends to the federal government public debt to GDP ratio is found in aggregate state and local government debt. From the 1850s through to 1890, colonial governments used debt to finance the construction of infrastructure. Tax revenue comprised a paltry amount of public finance (from 2% to 5% of GDP).

The surge in the ratio from 1890 onwards was not so much due to state and local government spending to offset the effects of the depression, but rather due to falling GDP. For Australia, this depression was economically worse than that of the Great Depression of the 1930s. A similar spike occurred during the 1930s.

Unfortunately, data on aggregate state and local governments were not continued after 1982 in the sources used to compose the figures. Parliamentary Library analysis provides some data on current state and territory net debt, again showing the debt burden is certainly not onerous. Gross foreign public debt sits comfortably at 20.7% of GDP.

Currently, public debt at all levels of government is tiny by historical standards and is certainly sustainable. The fashionable idea often repeated these days that rising public debt poses a risk to the economy has little substance in reality. Compared to the pre-WWII era, governments of today are a picture of fiscal responsibility and prudence, with the rise in taxation revenue helping to offset the need for using debt.

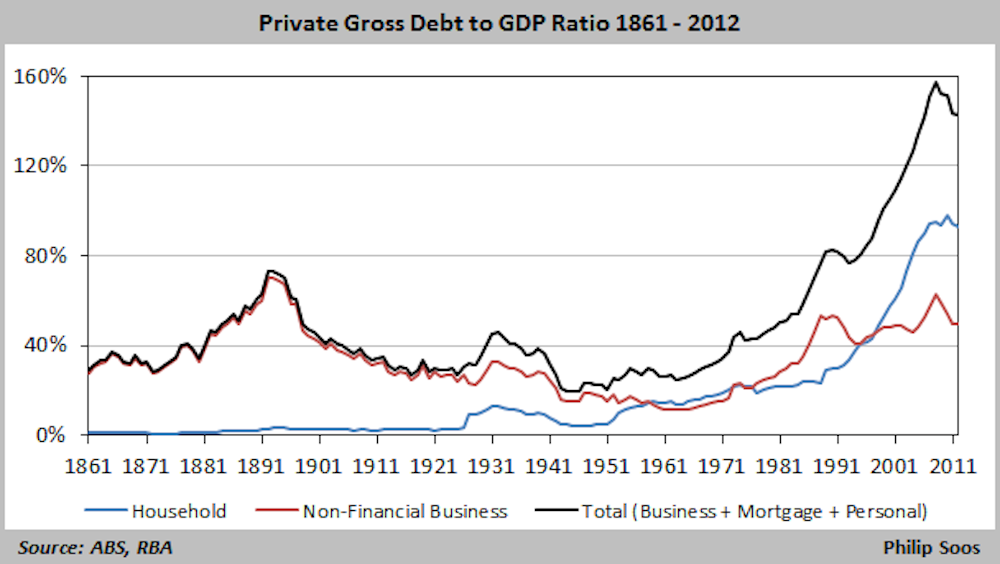

The real debt problem Robb has ignored is the colossal levels of debt that now saturates every part of the private sector. Private debt as a proportion of GDP is overwhelmingly larger than public debt. Personal debt is 9%, mortgage debt at 84%, and non-financial business debt is at 50%, for a total of 143%. A McKinsey and Co report estimates the non-banking financial sector debt at 91%.

Private debt is different to public debt. The historic record shows it is often used to speculate on assets prices, typically stocks and real estate, creating one bubble after another. Both the 1890s and 1930s depressions were caused by bursting commercial property bubbles, reflected in the sharp rise in the business debt to GDP ratios in the decade before both depressions.

A primary cause of the mid-1970s, early 1980s and early 1990s recessions were the bursting of smaller commercial and residential bubbles, financed by rising business and mortgage debt. The total private debt to GDP ratio reached a historical high of 158% in 2008, on an immense rise in household debt (mostly mortgage debt), driving the largest housing bubble on record.

Australia’s history shows increases in the public debt to GDP ratio have two causes: World Wars (1914-18 and 1939-45) and responses to economic downturns caused by private debt-financed speculation: the 1890s, 1930s, mid-1970s, early 1980s, early 1990s and the GFC in 2008.

An interesting point to note is the Coalition’s criticism of the rise in public debt that occurred under the Labor governments during the early 1990s and today. If the positions were reversed, we are supposed to believe Coalition governments would sit on their hands during a recession and GFC while unemployment and underutilisation increases, risking votes and consequently their power. In this scenario, Labor would then be denouncing the Coalition for being bad economic managers.

Economist Stephen Koukoulas has noted almost $40 of the $96 billion in debt inherited by the Coalition in 1996 was a leftover from the Fraser government in the early 1980s, when John Howard was treasurer. The recession during this period necessitated an expansion of government debt, though it was hypocritical for the Howard government to criticise Labor for its expansion of public debt when the Coalition acted no differently during an economic downturn.

That public debt has risen once again by a small margin since the onset of the GFC is not sufficient grounds to label it as excessive as Robb has. Thus, these criticisms over public debt have nothing to do with either political party being good or bad economic managers, but rather, is the result of cheap political point scoring, hoping the public doesn’t do its research.

Ultimately, the focus of concern should not be upon the government’s historically and internationally low position of public debt, but upon the immense burden imposed upon the Australian economy by private debt. Once the housing bubble begins to deflate and citizens reduce consumption to focus on debt repayment, the federal and state governments will have no choice but to go deeply into debt to ameliorate falling taxation revenue and higher unemployment.

There is no intrinsic problem with either public or private debt. Both need to be carefully considered to ensure efficient allocations into productive activity. Public debt is not a burden if it is used to produce an income stream to pay down the resulting interest or to enhance productivity, for instance, if invested in infrastructure, health, education, or research. It becomes a problem, however, if used to finance excessive defence spending, bank bailouts, pork-barrel projects and middle-class welfare.

The same goes for private debt. As long as debt finances production, the resulting income streams will be more than enough to pay down the debt. On the other hand, if private debt is used to speculate on stocks and real estate - as has occurred many times in the past - it simply results in a zero-sum game where speculators transfer assets among themselves without enhancing productivity.

Unfortunately, the discourse over debt is almost entirely focused upon public rather than private debt. There is no reason for concern over our relatively low federal or state debt. The real problem is in the major rise in the private debt, primarily within households. This is what commentators should be focusing upon.