The Australian economy is limping along – growing barely fast enough to absorb new workers, with interest rates at record lows, slow wage growth constraining household consumption, and investment relatively weak and declining due to weak business confidence.

The 2015-16 Budget is not going to turn this around. The deficit is expected to decrease from A$39.4 billion to A$33 billion which, given the margin for error that we’ve observed in past budgets, is neither here nor there in its economy-wide impact. It is the change in the deficit, not the size of the deficit itself, that determines whether a budget is contractionary or expansionary. So this budget will have a roughly neutral impact on the aggregate demand for goods and services.

This is the right fiscal policy stance. In fact, a neutral fiscal policy stance should be the general rule for Australia. It is unwise to attempt to use the Australian federal budget to manage economic growth.

Fiscal vs monetary policy

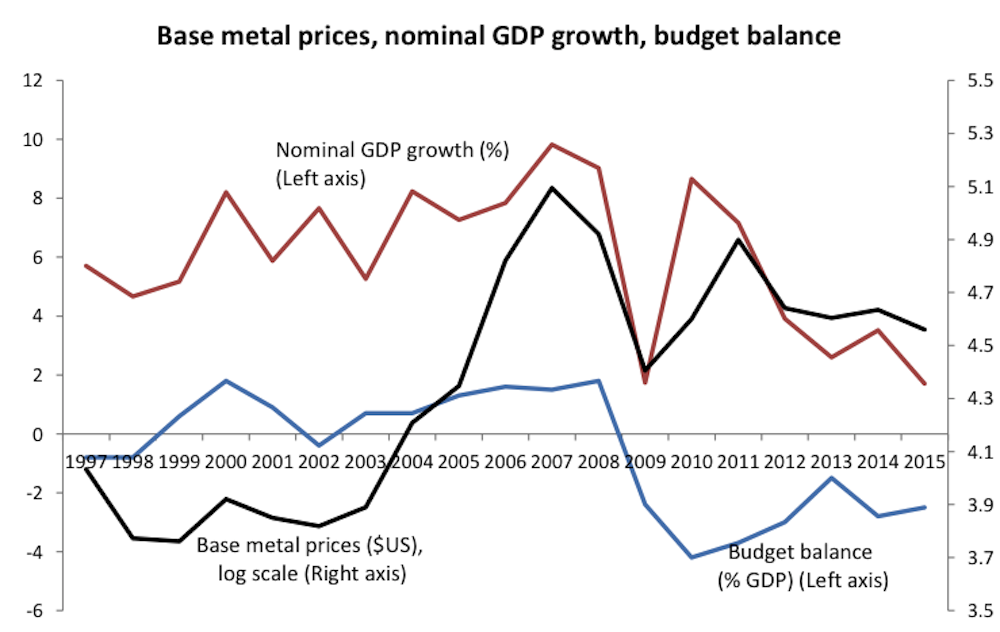

The Australian economy is periodically buffeted by large swings in commodity prices – base metal prices in particular, the last decade being a prime example. These swings are a major influence on growth in nominal GDP – the dollar value of the goods and services we produce. And this, in turn, is a key driver of the budget balance.

These relationships are illustrated in the chart below. You can see how closely the swings in base metals prices match growth in nominal GDP, especially over the past decade.

Attempting to use fiscal policy to smooth out these fluctuations is fraught with risks. Commodity prices can bounce back quite suddenly and unexpectedly, as they did in 2010-11 following the financial crisis (see chart). Fiscal stimulus is not so nimble.

In fact, the A$42 billion National Building and Jobs Plan – introduced in 2009-10 by then-Treasurer Wayne Swan to stimulate Australia in the aftermath of the global financial crisis - took years to roll out, with some school buildings still to be constructed in 2014.

As the chart shows, commodity prices had by, that time, risen and then fallen again, as had nominal GDP growth. That meant the government’s fiscal stance was out of sync with the state of the economy; it wasn’t clear exactly what cyclical downturn the stimulus was supposed to be smoothing out.

The claim that the Federal Government should have spent more in this Budget because Australia’s debt is low by international standards misses the point.

If you have no debt and then take a four week overseas holiday on your credit card, is it all OK because your debt is still lower than most other people’s? That depends on whether the holiday was better than the alternative use of the funds. Or is it OK because in a couple of years your income will pick up and you’ll be able to pay down the debt then? What if your income doesn’t pick up or you don’t have the discipline to pay down the debt?

This is what governments face when they try to stimulate the economy with borrowed money. Six years after the spending binge that started in 2009, the economy has not bounced back to enable the debt to be repaid as a naïve textbook model might assume. Rather, it sits on the balance sheets of current and future households, through their government, as future tax liabilities which will dampen future growth and cost future jobs.

Managing the swings in the economy is best left to the Reserve Bank of Australia (RBA). The RBA is more nimble than the government when it comes to stimulating aggregate demand.

For example, the RBA increased the cash rate seven times between 2009 and 2011 when nominal GDP recovered (see chart) at the same time as the Government was still pumping out billions of (borrowed) stimulus spending. So we had conflicting policy responses.

Also, the Australian dollar is very responsive to the RBA’s interest rate policy and supports it. It falls when rates are cut (which stimulates tradable goods and services) and rises when rates are increased.

Not so for active fiscal policy - the Australian dollar fights against active fiscal policy. It wants to rise when the government is trying to pump up the economy and fall when the government tries to slow down the economy.

Consumer confidence

Going forward, the main brake on the Australian economy is the lack of business and consumer confidence, as noted in the RBA’s May Statement on Monetary Policy. Consumers seem to be less responsive to lower interest rates than they have typically been. They have not responded much to the eight cuts in official interest rates from 4.75% to 2.25% that occurred between 2011 to 2014.

Why are consumers and business so cautious? One reason is because we have no idea whether a range of government policies in relation to taxation, superannuation, pensions, family benefits and so on, will get through the fractious Australian Parliament. So the less controversial this budget is, the better for consumer and business confidence.

There may be another factor at play. Households may worry that the Australian Government’s rising debt is, in fact, their own future tax liabilities (which they are, or those of their children). This debt has reduced the Government’s net financial worth by 20% of GDP since 2007, according to the latest Mid-Year Economic and Fiscal Outlook (Table D9).

Worse, the Budget Papers project a further 20% decline in the Government’s net worth in the next two years. This is a large transfer of net worth from future households to today’s households. So even though the deficit is stabilising and projected to decline, it is still significant and adding to government debt and future tax liabilities.

If this Budget does not kick-start confidence, we have to ask whether the large build up of future tax liabilities is partly to blame.