Australia’s decision to uncap university fees, announced in the budget last week, will for the first time expose Australian universities to unfettered market forces. It’s a decision that takes Australia’s higher education system into uncharted territory and precisely how it’s going to play out is difficult to predict.

What we do know is that Australia and the UK have similar systems of higher education, and the UK has followed Australia’s lead in recent reforms to the sector, such as adopting a local equivalent of Australia’s innovative Higher Education Contribution Scheme (HECS). With policy experts in the UK watching the latest developments in Australia closely, a comparison of the two countries is especially revealing of how different governments go about striking a balance between tight budgets and the needs of the sector.

Australia and the UK: similar systems in like countries

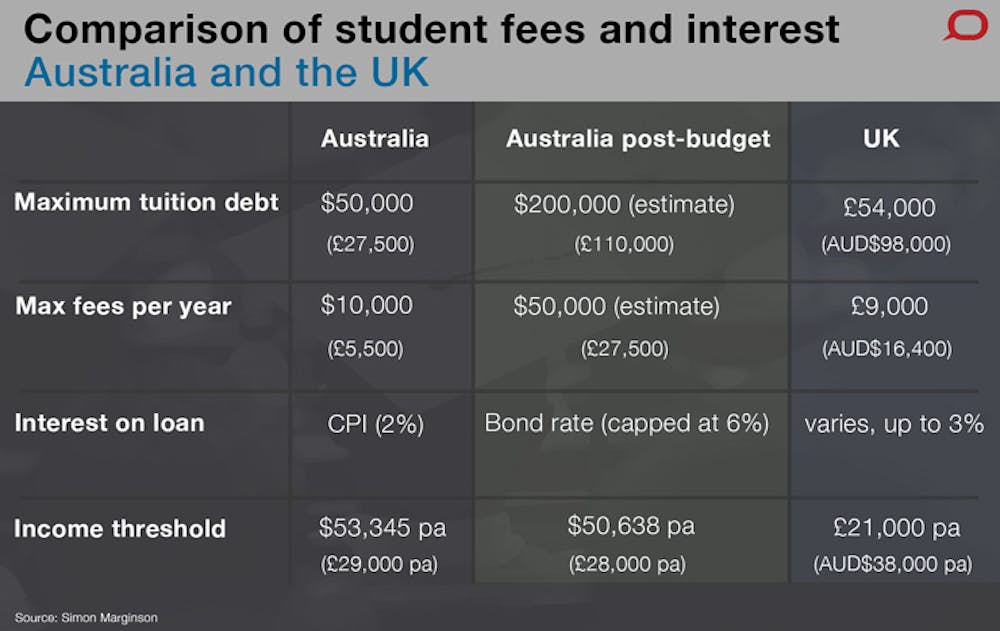

In the last generation, Australia and the UK have both doubled the proportion of the population entering higher education, while moving from near free tuition to a high tuition with loans repaid via income contingent taxation.

At a maximum of £9000, annual student fees for undergraduate degrees are higher in England. By comparison Australian students pay $6044-$10,085, depending on the discipline ($1 AUD = £0.56). However, student living support through grants and loans is considerably less generous in Australia.

Both nations extend income contingent loans to students in private higher education institutions, but with slightly different arrangements — in the UK funding for tuition fees is capped at £6000 while in Australia private students pay a surcharge of 25% of the loan amount.

In both countries the repayment of higher education loans doesn’t kick in until the student reaches an income threshold level. The threshold is higher in Australia as it is pegged to average weekly earnings. However, UK graduates repay only a proportion of income above the threshold, not total income. In both countries debts are written off at death, and in the case of the UK after 30 years. Both countries have problems chasing down debtors who move overseas.

In both countries the value of public subsidies of the present tuition schemes has been estimated at 35-45% of the total money loaned to students. This means that government is expected to carry 35-45% of the final cost of the tuition loans system and students and their families are expected to pay 55-65% (though it must be said that economic calculations of what is going to happen over the lifetimes of current students embody an element of guesswork).

This figure of 35-45% combines the effective public subsidy resulting from charging students interest below the commercial rate, in relation to tuition debt during the period before repayment is completed, plus the additional public subsidy that results from the fact that some former students will never repay all or part of their student debt, because their incomes will not be high enough to trigger the full repayment.

In Australia’s case it is estimated that in the final wash-up 23% of student debt will not be recovered. On top of that there is the effective subsidy due to the non-commercial interest rate on loan debt. Until this year’s budget the HECS debt has been adjusted annually on the basis of the CPI. There has been no interest rate above that.

In the UK, government calculates a figure, called the Resource Accounting and Budgeting (RAB) charge, that incorporates both elements of subsidy. The RAB is currently fixed at a high 45% of all student debt, up from 35% a couple of years ago. In part the change in the RAB occurred because forward estimates of UK graduate salaries have been lowered, due to the state of the UK economy. The RAB is of great political interest in the UK, because it indicates the public cost of the £9000 tuition system, and particularly whether the UK gained or lost money from the imposition of the controversial £9000 fee regime. An RAB of much above the current 45% would indicate that the English taxpayer has lost money overall on the change to the new system, despite the shift to a high fee market.

Australia does not calculate its own version of the UK RAB. The long term outcome for public finances, and the balance between the aggregated public subsidy and the student/graduate contributions, is sensitive to a number of elements including the interest rate on tuition debts, and whether this is fixed or variable at different levels of income or for different courses or categories of student. It is also affected by the income threshold for repayment through tax, and the rate of repayment.

The parallels between the UK and Australia go further than just the existence of income contingent tuition loans. In 2012 the Australian government uncapped the number of places universities could offer. This triggered an accelerated growth in student numbers in lower status institutions. It also created cost pressures on the budget, and debate about minimum standards of higher education providers. Growth has now slowed. The Lord Chancellor has announced the UK will deregulate numbers in 2015. Similar effects can be expected.

Now that Australia is to deregulates its fees, will the UK follow suit?

In last week’s federal budget in Australia, the uncapping of student places was maintained, as well as the uncapping of tuition levels from 2016. This will allow higher education providers to set their own fees, financed by income contingent loans as before.

The increased public cost will be balanced by an average 20% cut in teaching subsidies and by putting a higher interest rate on student loans, based on the bond rate. It is widely expected that most Australian universities will raise fees to at least two to three times present levels, though there will be a bargain market among lower status institutions and private colleges. Research-intensive universities will build extra resources and become more globally competitive. The students will pay for this. While present students accumulate a maximum debt of $50,000 (Medicine) over the program that could rise to $100,000-200,000 on graduation, and then become subject to commercial rates of interest on the student debt, which would mount for every year out of the workforce. Debt of this magnitude is likely to deter poorer families.

The government also intends to provide income contingent loans for students in approved private college courses on the same basis as loans for students in public universities, making those private colleges more competitive at the bottom end of the market. In the longer term this equal treatment of public and private institutions could encourage elite private universities to emerge. The government also plans a partial tuition fee for research degree students formerly covered by full scholarships, albeit a tuition fee again subject to income contingent loans.

These changes are yet to pass through the upper house. There is much student opposition to higher fees, interest rates and debt. Nevertheless, it is likely that at least a modified version of the package will be implemented. If the upper house strikes out the commercial interest rate on debt, as some are predicting, it is hard to see how the income contingent loan system could contain the ballooning public cost. In that case the level of tuition subject to income contingent loans may be capped, with fees above the loans cap subject to commercial borrowing. If Australia deregulates fee levels, no doubt UK policy makers will watch closely.