Australian homeowners who have been sharing their homes for profit using Airbnb, or like services, could be subject to the same “robo-debt” recovery services that have targeted Centrelink recipients.

This is problematic because of ongoing uncertainties about the legal relationship between owner and Airbnb guest, and whether or when the property can be subject to land tax. Despite this, owners are receiving automated notices and may possibly be admitting liabilities and paying fines they shouldn’t.

Until recently, governments, especially in Australia, have tended to be cautious and conservative in response to the sharing economy. That is not just because of the long-standing inability of regulatory systems to keep pace with technology, but also because of the threat of disruption to traditional industries and those who work in them. Despite this conservatism, the shift to a sharing economy has had a sense of inevitability about it.

Airbnb has had perhaps the most long-standing and significant influence in Australia, in most cases prior to any specific legislation being created to regulate it. And if trade and commerce are free of regulation, they are also free of government control, protection and taxation. In many cases legislators are still to work out how to regulate or tax this new economic model.

Identifying owners who Airbnb

While some arms of government, such as lawmakers, may have struggled to keep up with the information revolution, others, such as law enforcers, have not. Over the past decade, state and Commonwealth agencies have worked together to develop data aggregation and data-matching systems into a powerful regulatory surveillance tool.

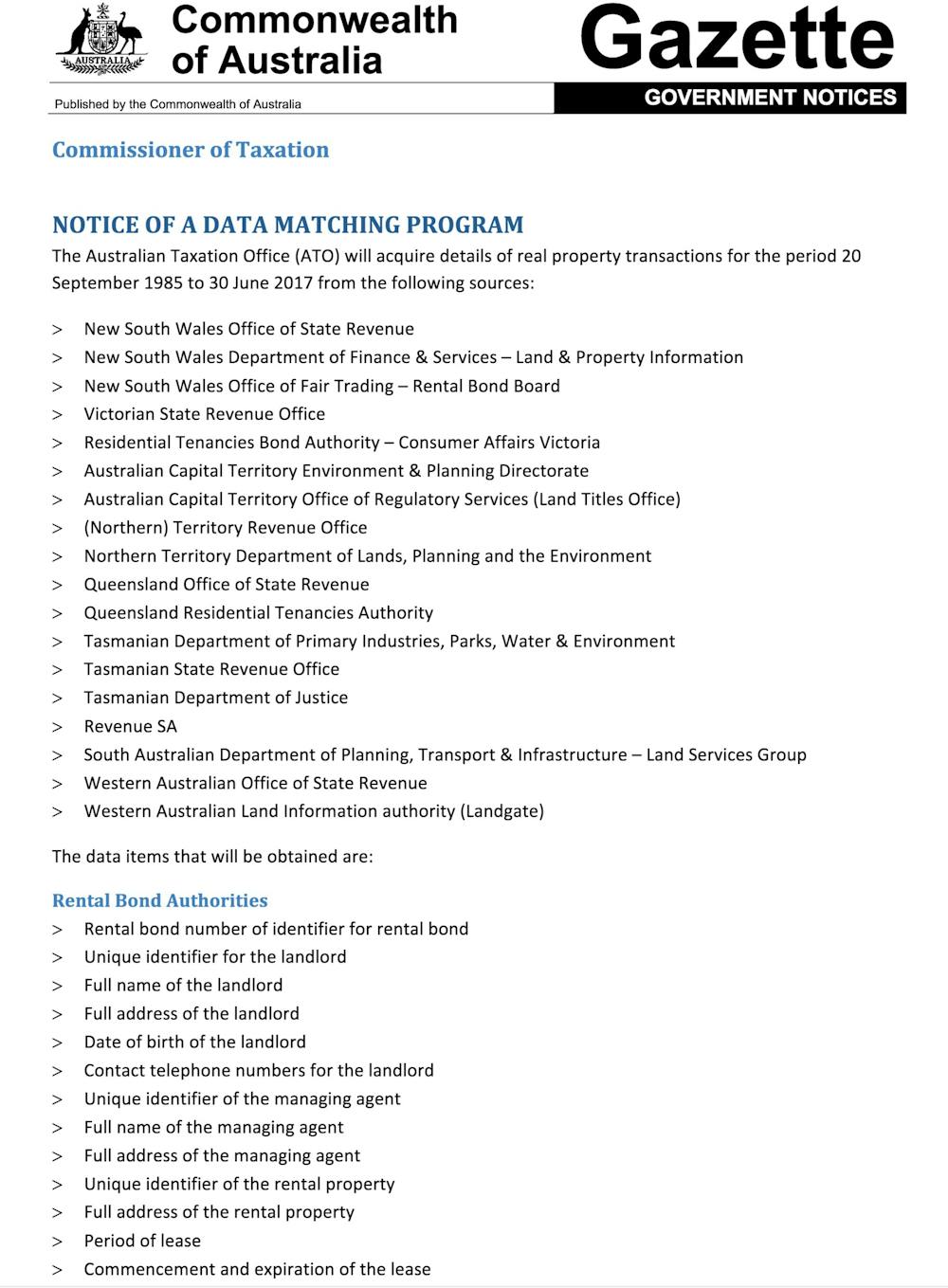

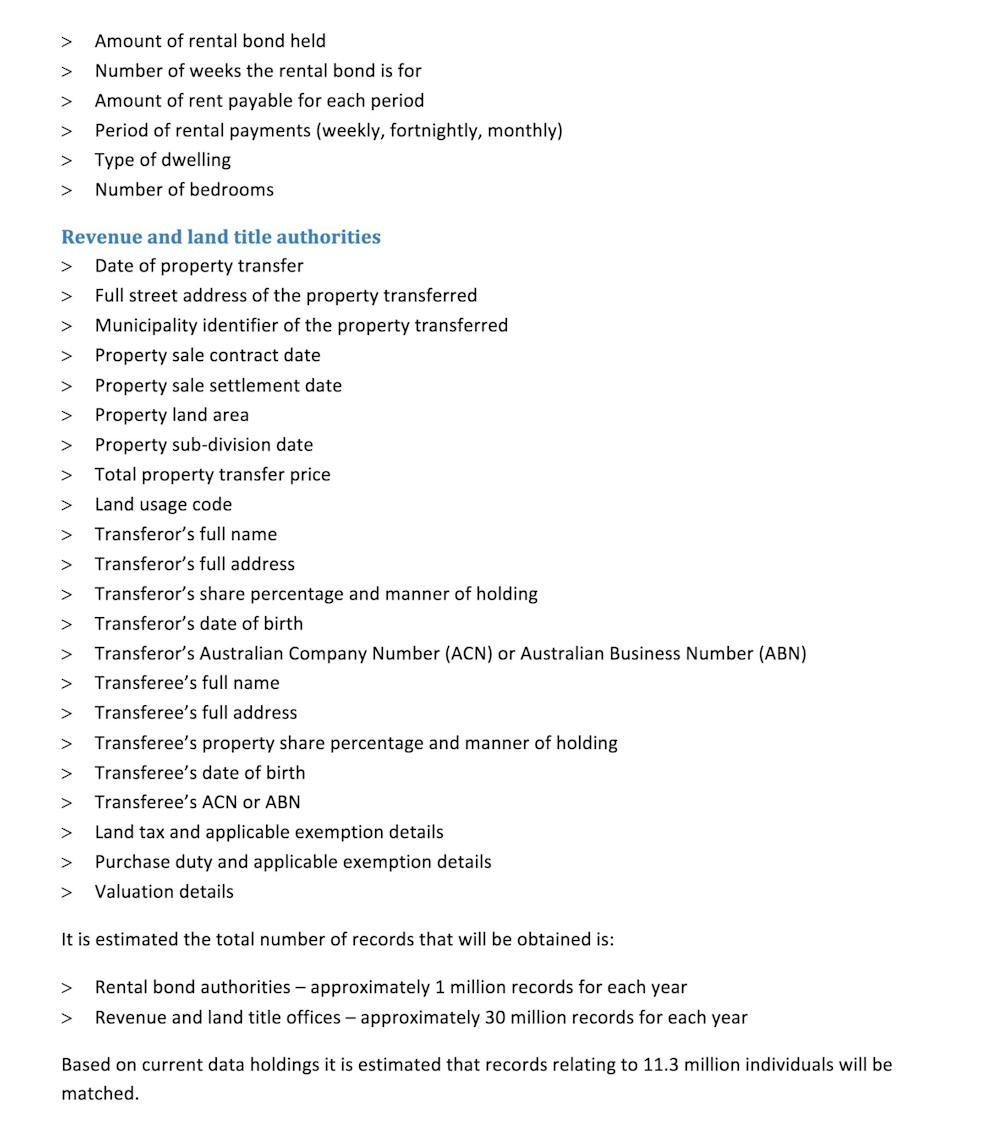

The Australian Taxation Office (ATO), for instance, reportedly data-matches some 600 million pieces of data. It shares the results with state revenue offices (which are responsible for land tax). These offices aggregate the ATO data with their own records along with data from other agencies, such as rental bond authorities, electoral rolls and apparently publicly available information.

The volume of data is massive, and limited only by the power of the computers used to identify target behaviour.

It is very likely, however, that state revenue offices can identify (see, for instance, here, here and here) when houses are being used for income-generating purposes (especially when owners declare that income as required to the ATO).

What’s the problem with this?

The problem is that the law is hardly certain on whether homeowners do owe land tax on short-term lodging arrangements like Airbnb. While each state and territory differs in the approach to land tax, the general rule is that a person’s principal place of residence is exempt. Land tax generally applies only to investment/second properties or commercial premises.

A landowner can do a number of things with their property – including generating revenue there – without turning it into a commercial premise. To think otherwise would mean parents who charged their adult children board would suddenly see their home treated as a business operation – and so would people receiving compensation for hosting home-stay students, or allowing a house cleaner or au pair to live in the house in exchange for reduced wages.

In fact, current laws are relatively nuanced when it comes to working out when a house is being used as a “principal residence” and when it is a “residential tenancy” or commercial premises. It requires looking at a range of factors, weighing them up, and ultimately working out if the owner is in exclusive occupation of the property for their own domestic purposes (even if they make some money there).

If a person staying in the house does not undermine the exclusive occupation and control of the overall property, then they are a lodger and the home is a principal residence.

If they do (for instance, because they have a separate lock on the door and can exclude the landlord), they are a residential tenant. The part of the property they occupy is then not the principal residence of the owner.

Data matching struggles with nuances

Such nuances are beyond the current scope of automated computer data-matching systems. And the problem with Airbnb is that every single home-stay arrangement is different.

In some circumstances, a guest may stay only a day or so, sharing common areas, probably not getting a lock on their door (maybe even staying on the fold-out bed in the living room). In other circumstances, the relationship may resemble more of a residential tenancy, taking possession of the whole house for much longer periods.

The other problem is that many landowners will have been operating under the assumption that they do not owe land tax on their homes. As a result, state tax offices face a dilemma: leave Airbnb alone until the law catches up, or make judgments on thousands of home-sharing arrangements to determine whether they are lodging arrangements or residential tenancies.

Some revenue offices appear to have opted for the latter course. And they have dealt with the logistical problem, as Centrelink has done, by employing robo-debt-like approaches.

Caught in the data dragnet

As an illustration, in Tasmania, the approach involves using evidence from the dragnet for information that the property is being advertised for accommodation, or that it is generating income. If this is the conclusion, the homeowner is issued with an investigation notice.

The investigation notice requires, under the force of statutory penalty, that the homeowner provide information relating to current and prior home use. Based on the information from these sources, it is then suggested that the principal place of residence of the titled and resident owner was only part of the building. This leaves the remainder of the property valued for land tax purposes, with the owner then potentially liable.

We suspect that many homeowners receiving the letters do not choose to contact a lawyer. Instead, they pay fines ranging from thousands to tens of thousands of dollars. Those who do challenge the assessments face extended uncertainty and expense.

An additional problem in this area is that state revenue rulings are not recorded and publicised like Australian Tax Office rulings. This means we don’t know how many successful or unsuccessful challenges there have been. It also means many tax lawyers and accountants may be unaware of the risk to homeowners who provide home-sharing arrangements.

What should Airbnb hosts do?

People who have received such letters should definitely consult with a lawyer with expertise in state tax.

Those who haven’t received notices but who are hosting Airbnb guests, or intend to, should still seek tax advice, preferably from someone legally trained. Given the ease with which people can advertise parts of their homes on Airbnb, it can be easy to forget that you are entering into a business transaction and generating income. Homeowners should protect themselves in advance.

State governments should reflect on this too. While it is legitimate to earn revenue from the sharing economy, the inherent unfairness of retrospectively penalising people who reasonably believed that their homes didn’t attract land tax is palpable.

Using automated software to “efficiently” achieve this aim by removing the human element is even more unfair. The practice really should stop until the law is modified to make the system more transparent, fair and, it might be argued, human.