Figures released last week by the Future Fund revealed it was outperforming the most aggressive of Australia’s pool super funds and was on track to reach its target of $140 billion a year early, in 2019.

The Australian reported the fund – intended to pay for defined benefit pensions to commonwealth public servants – “had beaten conventional super funds holding 100% growth assets by a handsome margin, even though it is widely invested in longer-term assets such as infrastructure and timber plantations”.

But does the Future Fund actually have higher returns? It does, but the picture is more complex.

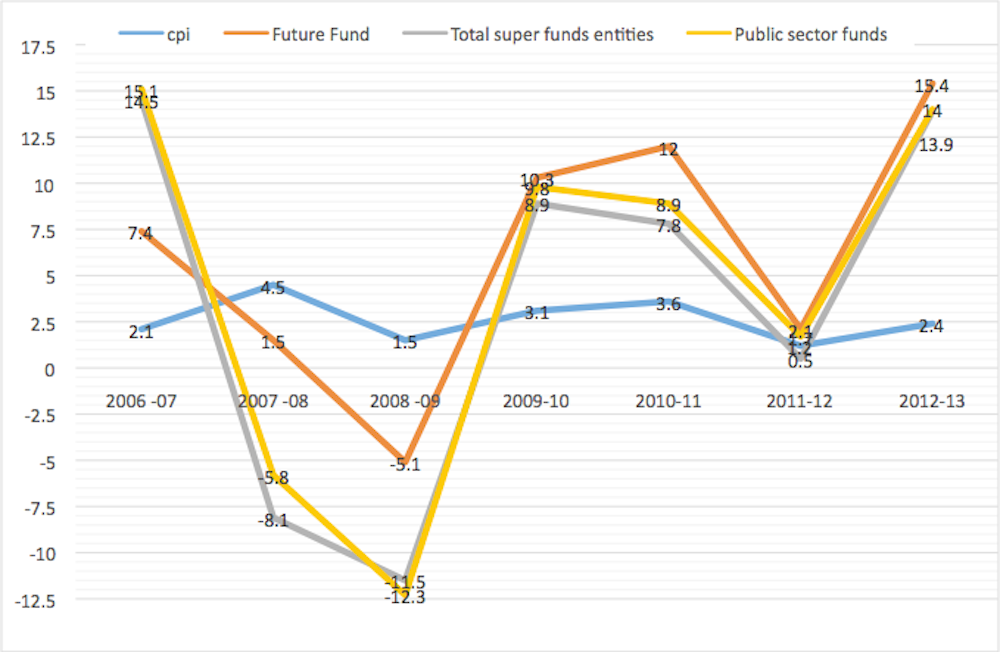

The following chart shows the CPI and the nominal rates of return per annum for the seven years 2006-07 to 2012-2013 for the Future Fund (established May 2006) compared with the average for total super funds reporting to the Australian Prudential Regulation Authority (APRA).

The public sector super fund figures from APRA are also shown, as the Future Fund is intended to provide for future pension liabilities in the public sector.

The rates of return for the super funds show volatility due to the global financial crisis (GFC) and recovery, compared with the relative stability of the Future Fund at that stage. In fact, the rates of return are closest for 2012-13.

The five year average annual rates of return and CPI for the periods to June 2012 and June 2013 are shown in the following table. The comparison shows the importance of the year 2012-2013 in improving the average rates of return in all cases and some convergence is indicated. They also demonstrate higher rates of return for the Future Fund:

Within these figures, rates of return are widely spread amongst individual funds.

The Future Fund’s five year annual average rate of return to 2011-12 of 4% is within the range of the top five individual funds: Challenger Retirement Fund the highest with 4.7% and Macquarie ADF Super Fund the fifth with 3.1%.

But the Future Fund and super funds are quite different, so like is not being compared with like.

The rate of return of the Future Fund appears less volatile than the others in the earlier years. Less volatility might be expected in the Future Fund as it has been argued to have more discretion in its operation, assuming stability is a goal.

The Future Fund has large numbers of analysts managing its portfolio relative to other funds. And the government is an implicit significant stakeholder from which the Future Fund can access funds without cost via transfer. It has done this quite a lot.

The Future Fund has relied extensively on transfers of revenue from privatisations (like Telstra) and budget surpluses arising from those, particularly in its early days. This meant relatively low rates of return to the Future Fund initially as the cash was gradually dispersed to assets with yields, at the same time as immediate access to costless funds.

Once the cash transfers from the government to the Future Fund were dispersed, its rate of return increased, also boosted by access to high yield infrastructure investments.

Most of the super funds do not have the kind of access to funds available to the Future Fund. Super fund members’ contributions are not costless, and automatically carry a liability.

The Future Fund’s liabilities are likely to be more predictable, as public sector employment is more stable and predictable than private sector. The cost of capital for super funds would be expected to be higher than the Future Fund as the super funds are more constrained in terms of source of assets and liabilities which are member based and this needs to be taken into account.

The higher rate of return to the Future Fund for 2012-2013, 15.5% compared with 14% average for super funds, amounts to a differential of 1.4%. The Future Fund’s higher rate of return for this year has been attributed to a change in investment strategy and portfolio structure which is in contrast with that of the super funds. This is mainly evident in the increase in the share of international equity in its holdings from about 23%, similar to that for super funds, by about 50% to nearly one third of its total assets.

This enables it to hedge via the foreign exchange market and foreign assets transactions. However, this strategy involves a higher and increasing foreign exchange risk than for the super funds which have held a bigger proportion of Australian equity and have less international exposure.

The Future Fund’s rate of return would increase due to a fall in the Australian dollar. If the Australian dollar does not move as predicted this can have an immediate and profound impact on the rate of return. A higher risk portfolio is likely to increase volatility in the Future Fund.

Yes, the Future Fund has shown a better rate of return than the super funds average. This includes less damage during the GFC. But the Future Fund and the super funds are not strictly comparable beasts. At least part of the difference must be attributable to the role of government in managing the Future Funds, including access to funds from privatisations and high return infrastructure investments.

The recent shift into international equity in the Future Fund may yield high returns currently but is dependent on exchange rate expectations. Volatility could increase.