The European Central Bank’s decision to spend 60 billion euro a month to buy sovereign debt in order to fight deflation and revive the crumbling eurozone coincides with a snap Greek parliamentary election on January 25.

If Syriza wins, as all polls indicate they will, this might be a serious setback for Greece, just at the time when the Greek economy was emerging out of a five-year deep recession.

Economic turmoil is expected, primarily because Syriza insists on achieving a cut to Greek sovereign debt. Germany and other eurozone countries consider this unacceptable.

A parade of ex-prime ministers

The threat of a Greek breakaway is not considered serious by some analysts. After the Greek elections, they expect a compromise, even if Syriza wins. Since 2009, Greece has had five prime ministers: three elected and two appointed. None lasted for long, primarily because they did not live up to their unrealistic promises.

Is this the fate of Syriza leader Alexis Tsipras? Probably. If he becomes the next prime minister of Greece he will face the leviathan he created: a mass of people who want more jobs in the public sector (more than 300,000 are waiting) and a considerable raise in private and public wages. He simply cannot do it. Nobody will give him the money to start a new public spending spree.

But if he does not deliver, then he will be forced to confront not only public anger, but his numerous clans inside his own party. He is doomed to fail. The sooner the better. The longer this lasts, the longer political uncertainty reigns, not only in Greece, but in the eurozone countries as well. It seems that if nothing else, the recent crisis has been successful in producing ex-prime ministers.

Taking on the tax evaders

Tsipras, along with the many political leaders before him, thinks he will find the money in the notorious Greek “lake” of tax evasion. In Greece, tax evasion and tax avoidance is an art, which the majority of Greek taxpayers have learned to perform well over the years. Ingenuity and practice is the secret.

Tsipras thinks he would succeed where others had failed. He is daydreaming. Nobody can beat tax evasion in Greece. Greece has one of the highest concentrations of small businesses in the world – close to 2.5m. There are 1.5m self-employed people in Greece, representing a third of all Greek employment. They are also the source of most tax evasion in Greece. They do not pay any Value Added Tax and “naturally” they do not pay income tax. The cost of auditing them exceeds any tax revenue benefit. If the political cost is added, then it is impossible to reduce tax evasion. Most of these self-employed vote for Syriza.

Good news, bad timing

This is too bad because under tranquil political conditions, the ECB announcement on quantitative easing would have been wonderful news for the Greek economy. Greece needs this more than any other country in the eurozone for at least four reasons.

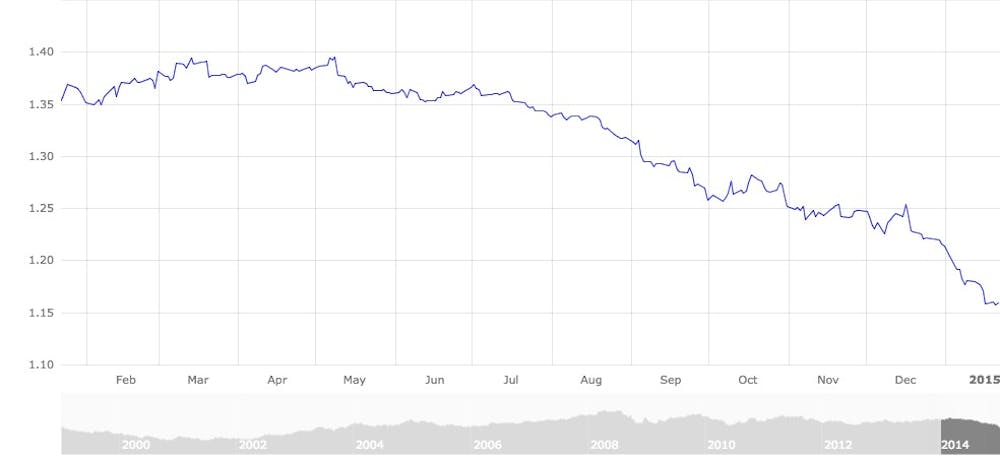

First, an expansionary monetary policy will keep the euro exchange rate low and this would be more than welcome in Greece, which depends on a low value of the euro to boost its international tourism receipts. The chart below shows that the value of the euro relative to the US dollar is much higher than its 2002 value, the inaugural year of the euro.

A devaluation of the euro is what Greece needs. And it comes at the right time because many European tourists are now deciding where to spend their summer holiday.

Second, the ECB’s policy of buying sovereign debt comes at the moment where the whole debate on the Greek debt has resurrected the speculation about Greece leaving the euro. If monetary policy becomes more accommodating, the risk of Greece defaulting on its debt and exiting the eurozone becomes infinitesimal small.

Third, and most important, is the impact of ECB’s initiative on the borrowing rates for the private sector. Greece faces the highest nominal interest rates in the eurozone. Real borrowing rates are even higher because Greek deflation is also the highest in the eurozone. With such rates hardly anybody would want to invest in Greece. But if interest rates are brought down and the cost of borrowing diminishes, the private sector can invest again, creating jobs and growth.

Finally, the ECB’s policy would bring down the interest rates in all eurozone countries. Private investment will pick up, generating more jobs and more income. This will have an additional positive impact on the Greek tourism industry since many international tourists come from the eurozone countries.

For all these reasons, the Greek elections this coming Sunday are crucial for the future course of the Greek economy. Whoever becomes the next prime minister must balance citizens’ overwhelming desire to stay in the eurozone with their insatiable hunger for more debt financing public spending. A herculean task indeed.