Fears are rising of a recession in Germany, Europe’s biggest economy and long-time powerhouse of the eurozone. The latest data does not look good – the following eight charts show why a recession looks likely and why Germany must act to avoid a prolonged downturn.

The first reason that economists fear an oncoming recession is that Germany’s GDP has been going down since roughly mid-2018, painting a rather dark picture of the economic performance of Europe’s largest economy. Technically, a recession is two consecutive quarters of negative GDP growth in a row. The economy shrank by 0.1% in the second quarter of 2019 so all eyes will be on September’s data.

1. German GDP growth

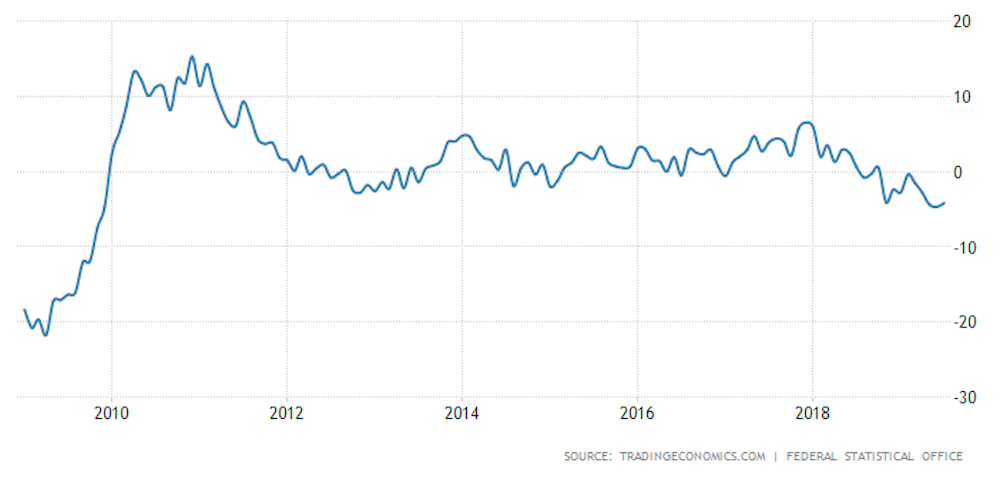

The second, and probably more significant, reason that a recession looks likely is that Germany’s latest figures for industrial production don’t look too good either. The overall decline we can see in the past 12 months has been at its longest since 2012-13.

2. Industrial output 2009-19

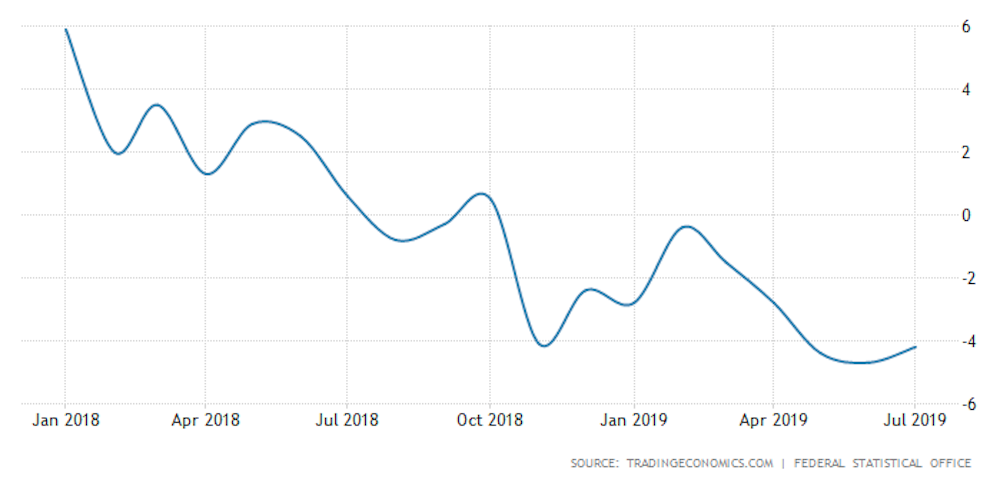

In fact, since October 2018 German industrial output has been continuously negative, with up to 4% decline over summer 2019, meaning Germany has performed worse than France, Spain, Italy and even Greece so far in 2019.

3. Industrial output 2018-19

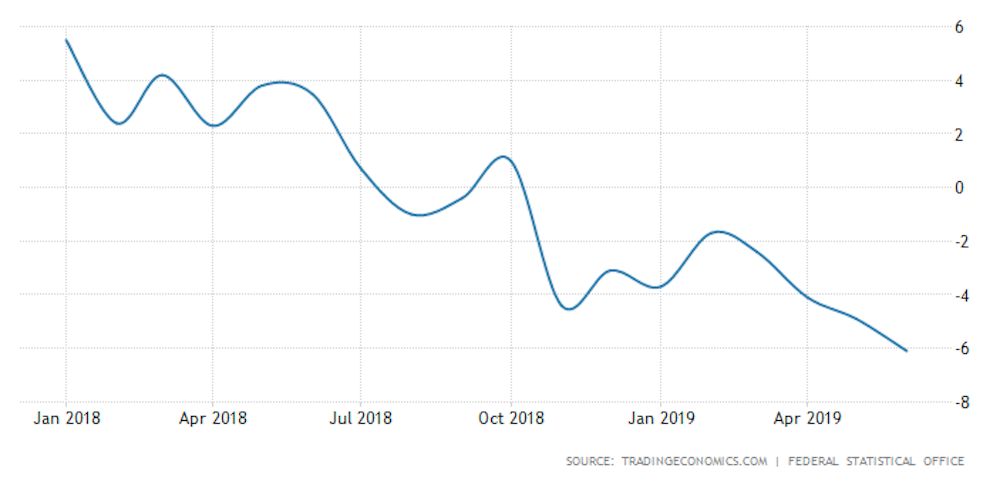

A closer look at manufacturing (cars, machinery and others), which makes up almost 80% of Germany’s total industrial production, paints an even worse picture with a negative growth of -6%.

4. Manufacturing production 2018-19

This is particularly concerning as the business confidence indicator of the German Institute for Information and Research also moved to its lowest value since November 2012 (94.3 points), indicating that German industry is anything but confident it will overcome this negative trend anytime soon.

Reasons for the decline

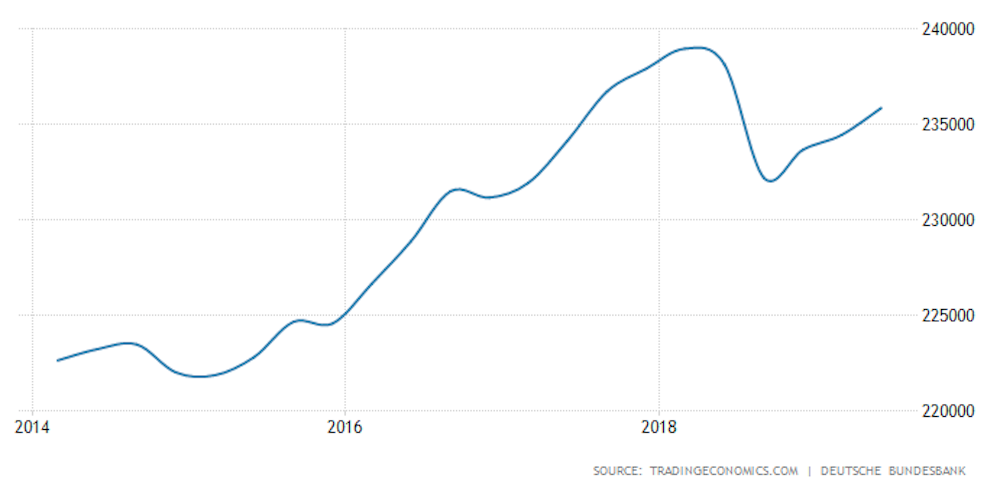

One of the main reasons why German industry is struggling so much is the country’s famous export dependency. Germany’s balance of trade, the difference between exports and imports, has seen some seasonally adjusted decline since the beginning of 2018 and only recently experienced what seems to be some kind of small recovery.

5. Balance of trade

Global growth in the past year has declined due to the ongoing trade war between the US and China, as well as US tariffs on EU exports like steel, aluminium, clothes, cars and food. This, along with the continued weak performance of European export markets, makes it difficult for the German industry to export and, hence, perform better.

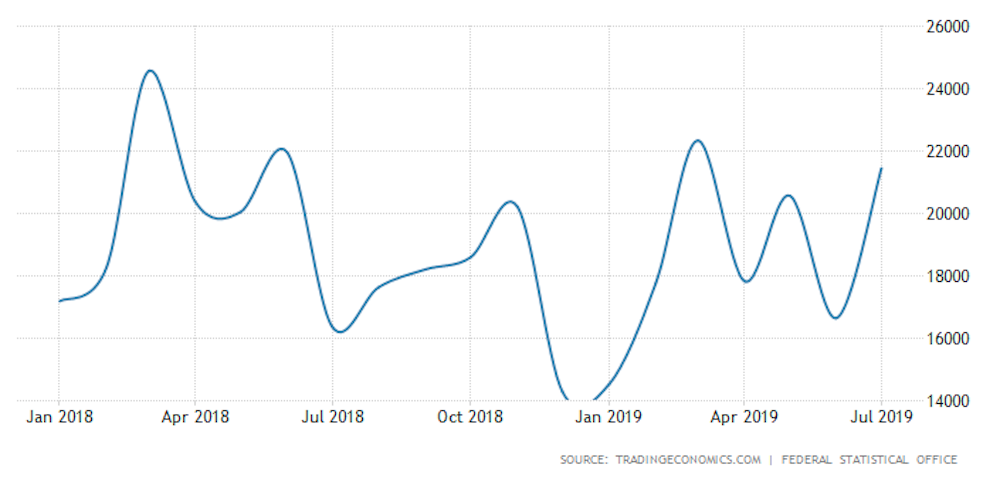

Moreover, domestic consumer spending in Germany has seen rather slow growth in the second half 2018 and just recently picked up a bit again. This may explain the recent recovery in industrial output as well.

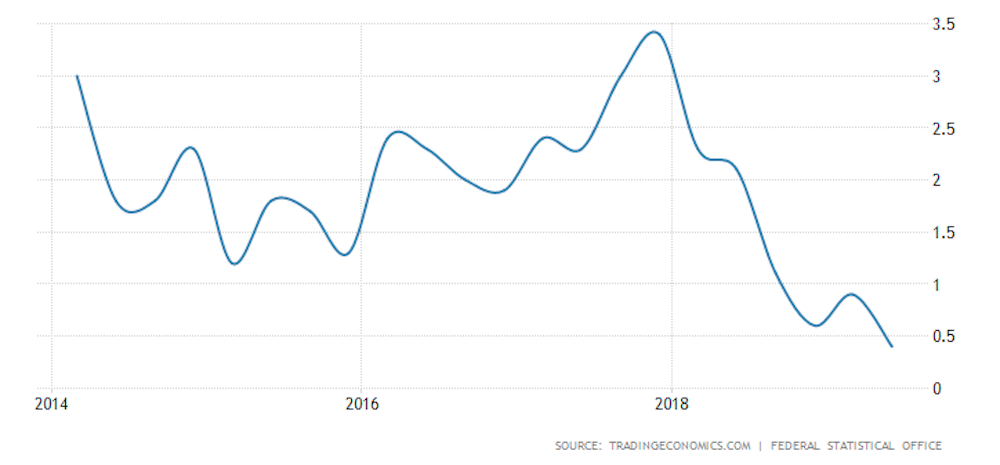

6. Consumer spending 2014-19

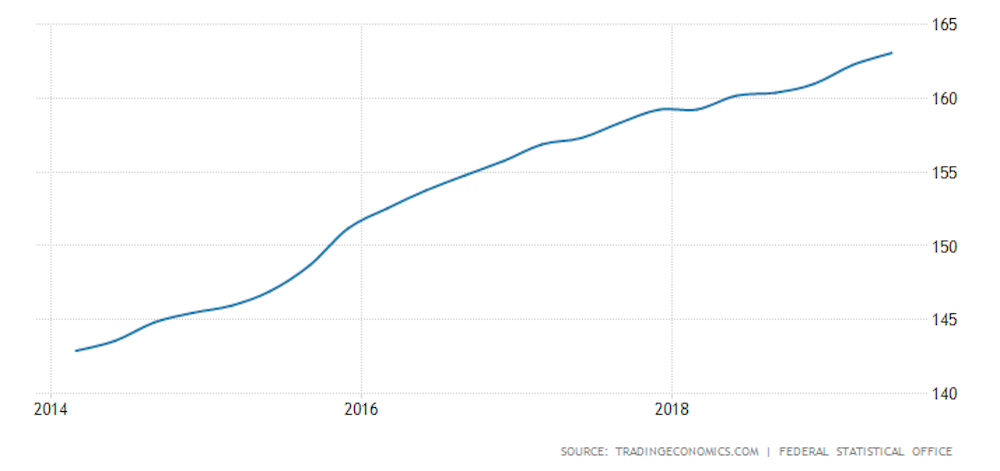

The reason for the stagnation of consumer spending during the second half of 2018 and the beginning of 2019 seems to be correlated with the decrease in consumer credit and a continued increase in household disposable income both around July last year, meaning Germans, for a short period of time, preferred paying off their debts to spending their money on consumption.

7. Consumer credit 2014-19

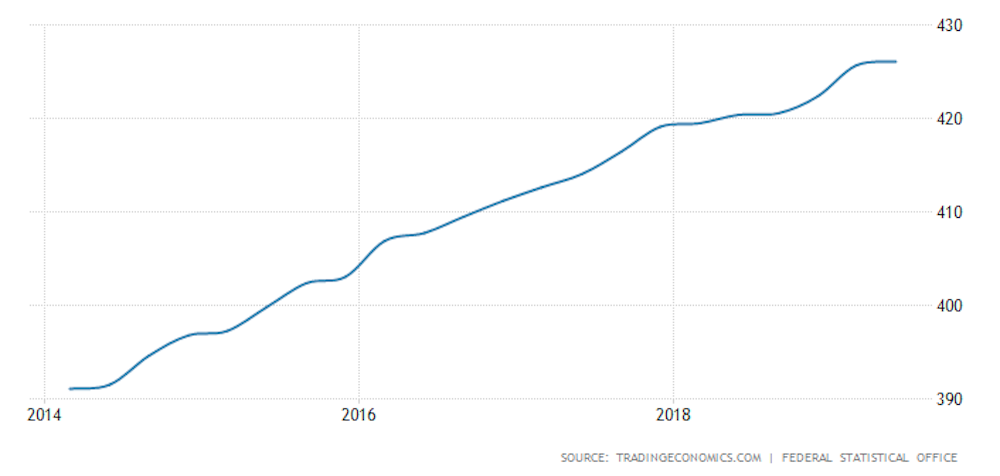

Finally, it is worth looking at government spending, which, in a similar fashion to consumer spending, was relatively low in the second half of 2018 and only recently picked up again.

8. Government spending 2014-19

So weak global demand for Germany’s exports, as well as low domestic demand, both from the private and public sector, means the economy shrank by 0.1% from April to June 2019. While private and public spending has seen some growth recently, the question remains whether this is too little too late to avoid a recession.

What’s needed

Germany is a big contributor to the economic performance of the euro area and EU as a whole. It is the largest trade partner, for many EU countries, including France, Italy, Belgium and Sweden. Given this, a recession in Germany will likely be felt across the continent, especially by those that form part of German supply chains.

The major factors outside of Germany’s control – US trade wars and tariffs – are unlikely to change anytime soon. Demand across the continent, which could improve German exports, is also likely to remain weak.

What Europe, and especially Germany, needs is a state-funded investment programme to spur innovation and domestic demand. So far, this kind of programme has proven extremely difficult. Most European states are fiscally conservative, with the narrative of austerity (not spending beyond your means) dominating the eurozone and Germany in particular.

But there are signs this could be changing. Reports are surfacing that Germany – in recognition of this looming downturn – is looking for ways to take on new debt to invest in economic growth and take advantage of the fact that borrowing levels are at an historic low. Hopefully this investment will not come too late to avoid a prolonged recession.