France and Germany, along with other European countries, have been increasing the share of renewable energy (RES) in their electricity mixes. In France, the share increased from 14% to 19% between 2006 and 2016, while In Germany it grew from 12% to over 32%. While France is behind schedule, by 2020, more than a quarter of its electricity consumption should come from RES, rising to 40% by 2030. Germany, reached its 2020 target early and decided to raise its 2030 target to 65%.

A major technological and economic problem of this transformation of power generation is the integration of intermittent RES into the grid and the power system. Solar (photovoltaic) and wind power depend on local, variable weather conditions. The system needs to be flexible enough to handle their variable and relatively unpredictable influxes. Techno-economic solutions can provide the required flexibility, including demand response, power-to-gas, and storage technologies.

In the short term, new storage capacity may not be required as controllable power plants, demand response, and cross-border power trading may be sufficient and more cost-effective. However, to stay in line with the Paris Climate Accord, CO2 emissions from the power sector are to be further reduced beyond 2030. Therefore, the growth of RES can be expected to continue in all European countries. So, if not today, it is generally recognised that new storage capacity will become necessary between now and 2050. What needs to be done?

This summer, Grenoble Ecole de Management (GEM) and the German Centre for European Economic Research in Mannheim (ZEW) surveyed energy experts in France and Germany about their expectations regarding the future need for and development of electricity storage technologies.

Electricity storage considered key to a flexible electricity market

EU governments recognise that a lack of power system flexibility can jeopardise their ambitious renewable energy goals as well as the power system’s reliability. Electricity storage has, however, played a minor role in the power sector so far. Currently, 97% of global electricity storage capacity consists of pumped hydro energy storage (PHES). France and Germany both have close to 7 GW of PHES capacity installed. This compares to roughly 5% of the total installed power generation capacity in both countries.

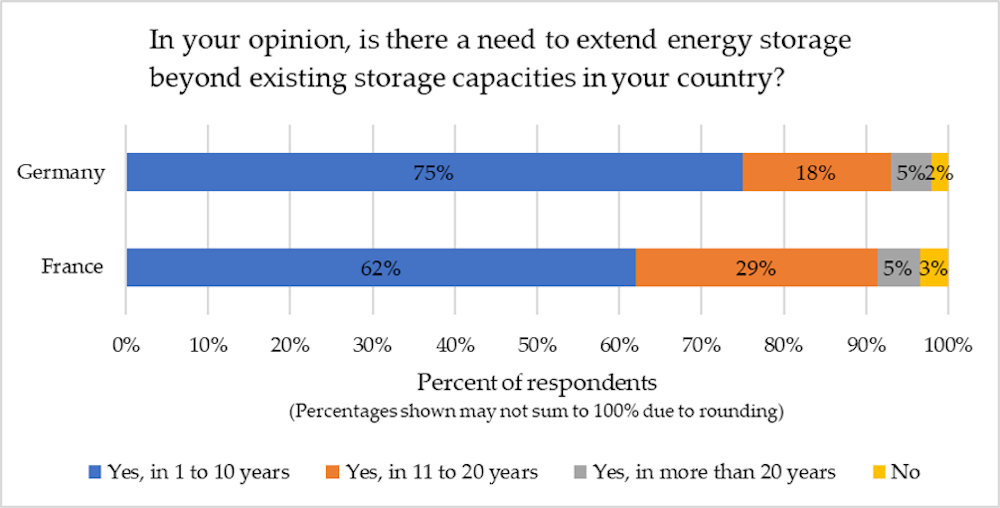

Of the energy experts we surveyed in Germany and France, a clear majority in both countries (75% and 62%, resp.) believes that the national energy storage capacities need to increase in the short to medium term already (1-10 years). Less than 10% see a need for expansion only in more than 20 years from now and a similar number think that the current capacity will suffice indefinitely.

The business case for storage technologies depends on technological innovation and electricity market reforms

A range of electricity storage technologies exist. Besides mechanical storage technologies as PHES and compressed air energy storage (CAES), there are electrochemical (batteries), chemical (e.g., hydrogen), thermal, and magnetic storage systems. Except for the mechanical systems, none are ready yet for large-scale deployment in the power system.

Lithium-ion batteries have experienced dramatic cost reductions and the technology is the fastest-growing storage technology. They typically find their application in consumer electronics, electric vehicles, and decentralised storage systems, making use of the high energy density afforded by the technology. It is now crowding out other battery chemistries and finding application in utility-scale systems. The cost-effectiveness of lithium-ion and other batteries, however, remains low and a barrier that partly explains their still small role in the power system.

In addition to cost-effectiveness, other barriers to their diffusion may include technical hurdles, social resistance, unpriced environmental impacts, or a lack of viable business models. Indeed, experts in both Germany and France mentioned high costs and a lack of incentives to invest in storage as the two major barriers, followed by technical hurdles as a distant third. Neither panel regarded social acceptance a reason for concern at this stage. However, resistance tends to emerge when concrete project plans materialise.

Governments are recognising these barriers and have implemented programs and processes to address them. The European Commission (EC), as part of its Clean Energy for All Europeans package, is drafting market reforms to make the market facilitate and reward flexibility. Proposed reforms include integration of intraday markets, allowing for dynamic retail pricing, and the right of consumers to produce and consume their own electricity. The EC also proposes a common definition of storage to resolve regulators’ confusion on whether to classify storage into consumption or production or both, with implications for which rules and levies apply. Furthermore, the EU is promoting technical innovation in storage through its strategic energy technology plan and the Horizon 2020 framework. Last year, it launched the European Battery Alliance to boost the European battery industry and fend off Asian and American market dominance.

Germany has supported the R&D of a spectrum of non-PHES storage technologies with 200 million euros since 2012, intending to bring down costs and better understand the value these technologies can bring to the power system. In addition, it has supported the deployment of decentralised battery systems to make decentralised solar-PV systems more grid-friendly. France has established a research network focused on electrochemical storage technologies, in which public research institutions and industrial partners collaborate to, in the end, develop a home-grown industry.

The German and French experts we surveyed seem to agree with the public support for R&D of storage technology. In both countries, more than 85% regarded the investment costs as an important or very important criterion when considering investing in large-scale deployment of storage technologies. In addition, at least 60% of the experts in both countries think that capacity and energy density are important criteria for deployment, both of which contribute to getting more storage value for money. Scalability is more widely considered important in Germany than in France. Furthermore, in both countries, a majority, though larger in Germany than in France, regards the ability to respond quickly to power demands and environmental friendliness as important or very important. Ecofriendliness can become a hurdle when a storage technology’s production or usage phase is environmentally harmful. Batteries, for instance, require rare earths, the mining of which has substantial negative environmental impacts. Hydro-electric projects can also often count on resistance from local communities and environmentalists. Interestingly, however, the one criterion that is most often cited as unimportant by the French experts is social acceptance. For 52% of German experts, however, it is still an important criterion.

As technologies improve, market reforms still at risk

These criteria, in combination with the dramatic cost reductions discussed above, may explain why both the German and French experts we surveyed expect that batteries will see the largest growth in terms of absolute capacity over the next ten years. Batteries provide flexibility and good scalability. A significant share of respondents in both countries expect an expansion of power-to-X (power-to-gas, -liquid, or -heat), which converts electricity to other energy carriers, such as hydrogen, methane, ammonia, or hot water. Power-to-X enables so-called “sector coupling”: the exchange of energy between previously disconnected energy systems, such as the between the gas and electricity grids, or between the electricity grid and district heating networks. Still a considerable minority of the German and French experts (11% and 13%, respectively) expects PHES to see the largest absolute growth. None of the survey participants expect much expansion of flywheel and magnetic storage capacity.

In conclusion, governments, grid operators, and research institutions are well aware that the power system requires more flexibility to realise the medium- and long-term goals for electricity from renewable sources and to facilitate self-generation by consumers, while maintaining the level of reliability and affordability consumers have grown used to. Energy storage technologies are widely considered an indispensable group of flexibility solutions. They need to be developed along two major axes. First, the capital costs of storage technologies need to come down. And second, the rules governing the power markets need to be revised so that markets value flexibility and let various flexibility technologies compete on an equal footing. The governments of Germany and France are both funding coordinated R&D programs for storage technologies, as is the EU.

New rules for the EU internal electricity market are currently on the table that would provide for better integration of storage services. However, several member states, France included, assert that the new rules would render their current capacity markets illegal. If the reforms are not adopted at the European Council meeting in December, the development of storage services might be hindered, which could render future integration of RES unnecessarily costly.