Germany’s strategy for export-led growth has set the Eurozone up for a fall. Plans to introduce minimum wages in 2015 might be too little too late for European countries locked in a futile game of beggar-thy-workforce.

At its heart, Europe has a fundamental problem – in fact, the world has a problem – there are too few good jobs: an global estimate of 1.8 billion too few. This is not news. There have been insufficient good employment opportunities since the Industrial Revolution. Simple economics indicates that too few jobs means, other things being equal, declining living standards for the working class. Many economists expect new technology to exacerbate this problem.

For centuries the industrialised economies put their faith in continual growth to distribute the benefits of capitalism. Moreover, in the mid-20th century, economic policies were adopted such that national prosperity would be enhanced through markets constrained to serve society, rather than vice versa. This ushered in the golden age of capitalism — the rich got richer of course, but with low unemployment and decent wages, the poor became better off as well.

Sadly, since the early 1980s, it has become clear that there are limits to growth – even state-funded growth. In response, the doctrines of classical (market) economics were reasserted, even though history indicates such policies exacerbate crises and inequality. The average American, for example, has seen real incomes stagnate for three decades.

Knowing me, knowing euro

Fast forward 20 years and we see in the current Eurozone crisis a playing out of the struggle between the progressive and the classical economics, as embodied in the French and German governments’ labour market policies.

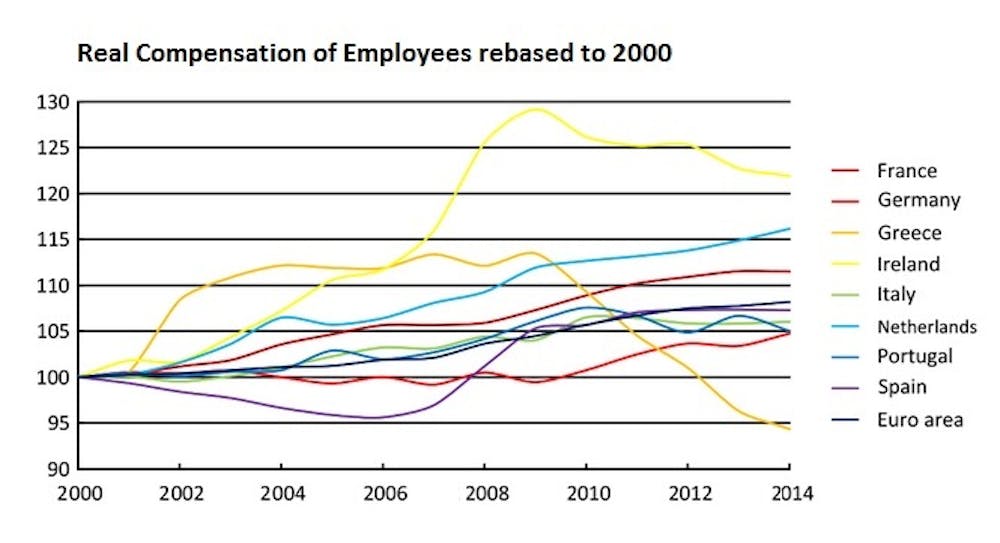

In the first decade or so of the euro, German labour policy was based on wage restraint. So strict was the austerity imposed on the workforce, many eastern Germans were of the opinion they were better off under communism.

When a nation is in a fixed exchange-rate regime, relative deflation is equivalent to devaluation. Despite fair-to-middling growth in productivity, Germany’s policy of wage restraint gave it an increasing competitive advantage in Europe. Globally, the relative weakness of the other Eurozone nations kept down the euro/dollar exchange rate, thus helping German exports to the rest of the world. The size of the trade surpluses generated transformed Germany from the sick man of Europe to a so-called economic powerhouse. To sterilise the inflationary effects of the trade surplus, Germany re-exported excess capital through loans and transfer payments, notably to the Eurozone periphery.

All good things must, however, come to an end. Germany’s trade imbalance could only persist so long as other nations continued to demand both her goods and the loans with which to pay for them. Once it became clear the European periphery had taken on unmanageable debt, the “system” (for want of a better word) collapsed into crisis.

Voulez-vous

The question now (as then) is how to restore equilibrium. Naturally enough, Germany is disinclined to depart far from its domestically successful low-pay policy, despite some heartfelt calls. Therefore deficit nations have been forced drastically to drive down their own labour costs: simultaneously, governments have been forced to reduce spending to meet the costs of restructuring the aforementioned debt: in sum, to impose austerity.

Which brings us to France. Officially France has chosen to respond to the reduction in demand for labour by reducing the length of the working week, obliging workers to ignore work-related e-mail after 6:00 PM and decreasing the retirement age for many. If there are too few jobs to go around, it makes sense for people to work less – a 30-hour week has been suggested by some economists – though there is no evidence to support the theory that elderly workers crowd younger people out of labour markets. Notwithstanding, despite Europe’s greying population, our shortage of youth is more than outweighed by a shortage of jobs in which they might be employed.

France has done better than most nations at weathering the Eurozone storm. Her real per-capita GDP is back to 98% of pre-crisis levels (in contrast, the UK managed 96% and the Eurozone as a whole managed 97%). France has engaged with austerity to some extent, but her economy remains sluggish and unemployment is on the rise.

If France remains in the euro, her relative competitiveness will continue to decline. In the long-run, either she must fully embrace austerity or Germany must abandon the policy. The recent resignation of the French government is an indication the debate is by no means ended.

Winner takes it all

Ultimately, it is an open question whether Europe can cut her way out of recession by equilibrating austerity. In practice it is more likely every cut will set off a downward spiral of further competitive deflation as each nation seeks to out-compete the rest. No state can win this game..

More realistically, the choice is whether to abandon the euro as a failed experiment, or for the Eurozone to put an end to the pursuit of nationalist polices and focus on what is best for the continent as a whole. Bonne chance!