After more than a century of a “life of plenty” with its lion’s share of a seemingly ever-growing advertising market, newspapers have fallen on hard times. The turmoil in the news media is not confined to print ventures, but it is newspapers whose future is most in doubt.

Although the signs had been present for some time, it wasn’t until the global financial crisis hit in 2009 that concerns about the industry’s future began to emerge. Although wary, industry leaders were optimistic that the downturn would be short-lived, just as had happened in the past. While overall advertising did rebound the following year, for newspapers the recovery was weaker than for other media and short-lived.

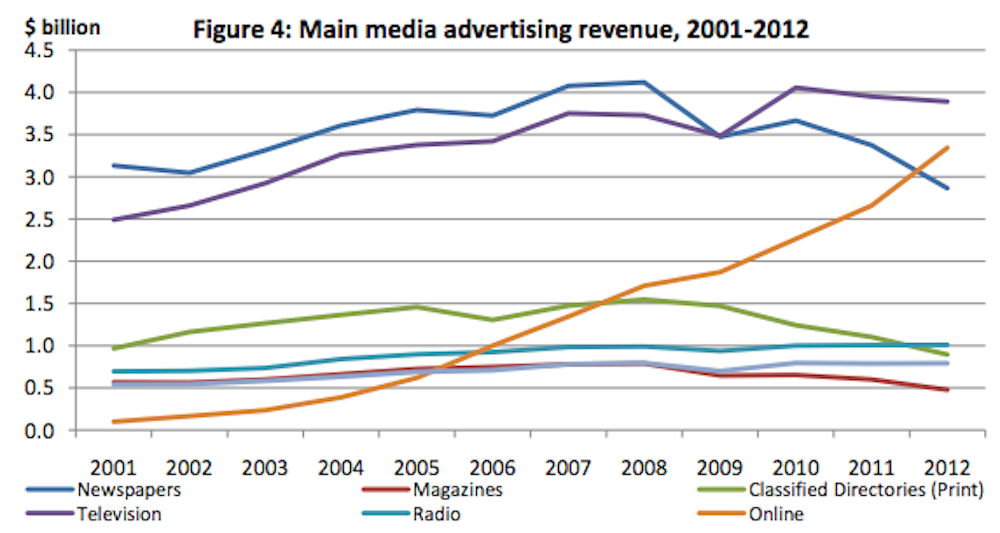

As a result, for the first time ever, the newspaper industry was displaced by television as the medium with the largest share of the advertising market. Newspapers continued to lose ground thereafter. In 2012, the industry was relegated to third place in market share by online advertising, which was clearly surging towards gaining the top spot.

The State of the Newspaper Industry in Australia is a recent research report released by the News and Media Research Centre (NMRC) of the University of Canberra. The study examines developments in the industry’s structure and performance from early 2000 to the present to give context to newspapers’ current economic situation and future prospects.

Although the report is concerned primarily with the industry as a whole rather than individual newspapers or firms, it presents an illustrative case study that highlights Fairfax Media’s response to online developments during the period of review.

Online threat underestimated

The industry clearly underestimated the threat posed by the development of online competition. Although several newspapers moved early to establish an online presence, the initiatives were largely pursued to complement traditional activities rather than strategic actions to reposition their operations and bolster their competitiveness in the rapidly changing environment.

More recently, once the magnitude of the threat became evident, newspapers have scrambled to restructure in an effort to contain its impact. Their efforts so far have been concentrated in two broad areas: restructuring of publishing operations to re-align production costs with lower revenues; and seeking to convert their online readerships to earnings.

The increasing range of news and advertising services accessible on the internet is changing the relative comparative advantages of established media. The adjustment process is having a significant impact on established structures. The impact on newspapers has had both positive and negative implications.

Newspaper websites are very popular, giving them an online following much larger than their offline readership. But newspapers have not been able to capitalise significantly on their online popularity. Moves to charge frequent visitors for online content have had some limited success: early indications suggest slow growth in online subscriptions.

Also, because the internet has largely unbundled advertising from other content, the popularity of online newspaper websites has not produced commensurable gains in advertising earnings. The unbundling has helped specialist online advertisers make significant inroads in markets such as classified advertising in which newspapers were once dominant.

More readers, less value

The internet has become a very important source of news and information and newspaper sites are among the most popular. Yet visits to news sites tend to be fleeting. Australian data on time spent on news websites are very scarce, but there is no suggestion that the local experience differs significantly from that in countries like the US and UK.

For the US, Google’s chief economist Hal Varian noted in 2010 that on average a person spent 38 minutes a month on online news consumption. That is little more than 70 seconds a day. In contrast, the average time spent reading a newspaper in the US is about 25 minutes per day.

In other words, the average offline reader in only two days spends one third more time on reading a newspaper than an online reader does in a whole month. A more recent ComScore report paints a similar picture for the UK. The average time visitors spent on newspaper websites was also reported to be 38 minutes a month.

The small average time spent on online news consumption reduces the appeal of online newspaper readers for advertisers. This is the core of the reason why rates for online newspaper advertisements are a small fraction of print advertising rates.

The paywall experiment

Newspaper initiatives and strategies to monetise online popularity have had mixed results. The main approach so far has been the installation of paywalls to access content. Some major newspapers overseas have established successful models. Locally, Fairfax and News Corp Australia have recently placed much of their news content behind paywalls but few data on their experiences are publicly available.

The Finkelstein Inquiry received some interesting information on willingness to pay for online access to news, which is a major problem for newspapers’ prospects. According to a submission by Scott Ewing and Julian Thomas at the ARC Centre of Excellence for Creative Industries and Innovation, seven in ten respondents to their surveys said they would not consider paying for an online version of a newspaper.

Of those prepared to pay something, fewer than one in ten were willing to pay the suggested typical hard copy cover price of $1.50. More than half indicated an amount of 50 cents or less.

Much of the traffic to online news sites is made up of casual visits by readers primarily in search of one or a small number of items of interest. Often the interest is likely to be in contemporary news items not exclusive to the site visited. In such cases, the individual simply goes elsewhere if a site seeks to charge for access.

Many free sites are readily available for undifferentiated news stories, including the ABC, ninemsn, Yahoo!7 and other established news media. Less casual readers seeking access to more differentiated content are likely to be more predisposed to pay an appropriate price to get it. These readers offer greater prospects to newspapers as potential digital subscribers.

But the size of the market will be limited and will be highly dependent on the price charged. There are some broad parallels here with the large differences in demand for free-to-air and pay TV.

Current print edition subscribers are at the other end of the scale of interest and willingness to pay for access to newspapers. They are often loyal habitual readers of particular newspapers and are unlikely to discontinue their subscriptions, at least in the short term.

In between, the situation is more complex. There are “marginal”, price-sensitive, print readers who may be attracted by the lower cost of online access, and current frequent visitors to online news sites who are willing to pay something less than a print subscription to read a newspaper online. These latter readers are the main focus of the online paywall strategies.

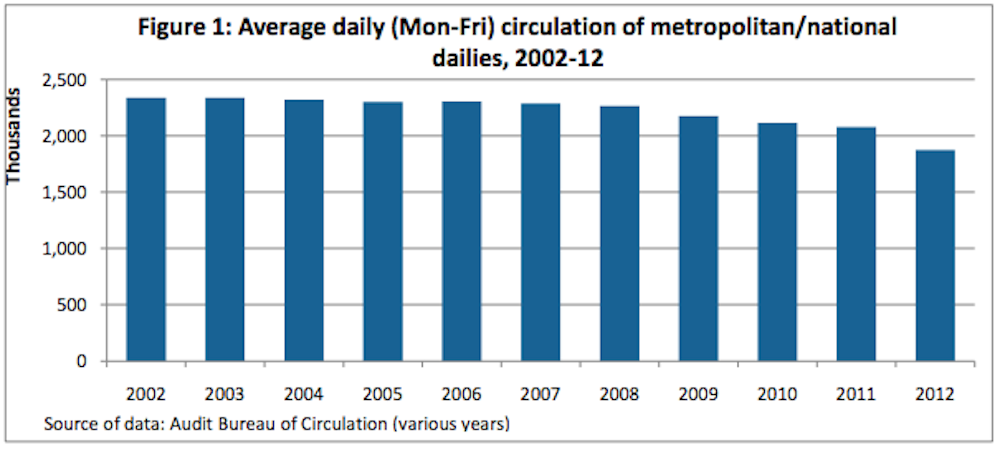

The Audit Bureau of Circulations introduced auditing of digital newspaper sales in the June quarter of 2012 using a process that became compulsory for all its members from July 2013. The circulation data for the 12 months ending June 2013 show continuing contraction of total weekly print sales amounting to 10.9%. While there has been some healthy growth in the digital sales of some newspapers, it has not been sufficient to offset the decline in print revenue.

Whither the Fourth Estate?

Overall, the NMRC analysis depicts a depressing picture of an industry being overwhelmed by enormous pressures and struggling to adjust to the new competitive environment. It’s not surprising that some commentators have been predicting the demise of newspapers or serious problems for democracy from a weakened industry unable to perform the important public interest role of holding governments and institutions to account.

The changing structure of the industry and its capacity to perform its public scrutiny functions received extensive consideration by the Finkelstein Inquiry. While the inquiry expressed “moderate concern about the ability of newspapers to adjust to the changed market environment”, it noted there was “reason to believe that newspapers are well placed to adjust their operations”.

Still, the inquiry warned:

The necessary restructuring to adjust to the digital environment will not be smooth sailing. Both threats and opportunities are present. Much will depend on the ability of established newspapers to develop viable business models that will enable them to continue playing a major role in the industry.

Developments since the Finkelstein Inquiry report accentuate the deep structural changes that are taking place. The declining trend in print circulation has quickened, forcing major publishers to re-align operating costs with lower revenues and implement strategies to expedite transition to fully digital operations.

Gains from digital subscriptions and digital advertising, although growing, continue to be insufficient to make up for the loss in print circulation and advertising. It will be many years before they reach balance. The transition of newspapers to a digital market is expected to be a hard and drawn-out process.

When the market eventually settles down, the industry will likely be significantly reduced in size and influence, particularly in the advertising market. In the “news” market, the reputation of the established mastheads should provide the industry with a solid base to retain and build its influence in the new environment.