You might have missed it, but last month something unusual happened in Australia’s eastern gas market. Gas in a major pipeline that normally flows from north to south started flowing in the opposite direction for the first time.

This seemingly small change reflects big upheavals in Australia’s gas market as exports expand significantly.

At Gladstone, Queensland, coal seam gas companies have invested around A$80 billion in equipment to chill gas to -160°C and convert it to liquefied natural gas (LNG). This liquefied gas is then loaded onto ships and sold to overseas customers. Exports are well underway with over 80 70,000-tonne LNG cargoes loaded in 2015.

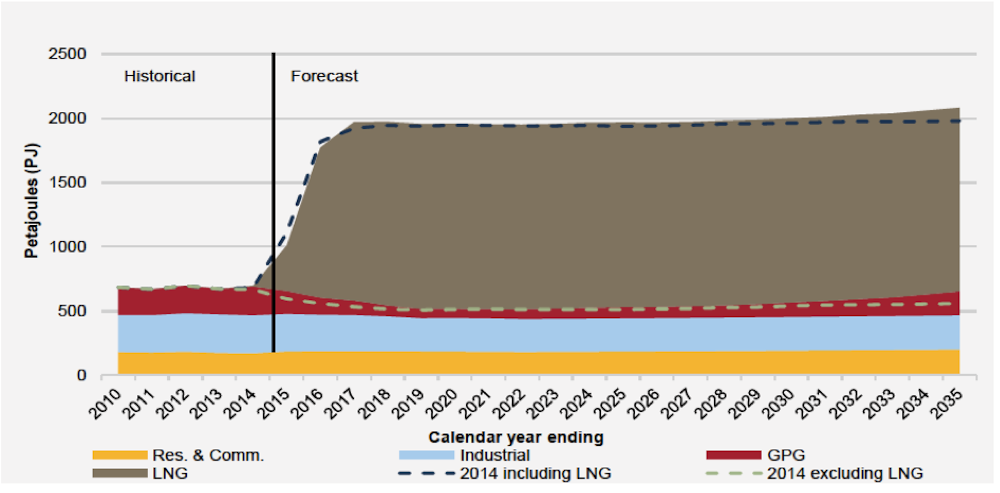

As shown in the following chart, eventually three times as much gas will be exported from Queensland in the form of LNG each year as has historically been used in all of eastern Australia.

The gas vacuum

In 2012, the head of a major Australian gas retailer famously referred to the planned Queensland coal seam gas export projects as “a giant vacuum cleaner for the East Coast gas market”. This vacuum has now been switched on – and it’s sweeping up gas not just from coal seam gas producers, but conventional gas producers too.

Domestic gas consumers – renters, homeowners, commercial building managers and industry – were warned they would see gas prices rise as the attractive Asian market opened up for previously landlocked eastern Australian gas.

Producers such as British Gas, Conoco Phillips, Origin and Santos pioneered coal seam gas technology to liquefy gas liquefaction-and-export as a way to monetise their vast resources in Queensland and New South Wales.

A second goal was gas producers’ long-held dream of linking eastern Australian domestic gas to higher overseas prices. Until recently, the people and businesses of eastern Australia enjoyed some of the cheapest gas in the developed world. Those days are gone.

Producers have successfully converted coal seam gas to LNG, gas prices are climbing, and long-term industrial gas customers are struggling to agree acceptable commercial terms with a limited number of gas suppliers.

Unexpected winners

An intriguing side-effect of this new coal seam gas export industry are the benefits flowing to companies such as Esso Australia and BHP Billiton that produce gas from conventional sources and, at this time, have no direct role in Australian coal seam gas.

Of course these conventional gas producers benefit as wholesale gas prices rise. But there are other, possibly even more profitable, effects.

From last month, the gas filling the new LNG plants wasn’t just coal seam gas. Coal seam gas companies are finding it difficult to cost-effectively produce their own gas and meet export contracts. The reasons include local landholders and communities, the weather, and/or challenging geology and complex drilling techniques.

To meet these contracts, gas from conventional oil and gas operations such as at Moomba (northeastern South Australia) and the Bass Strait (offshore southern Victoria) is now travelling north.

On December 14, for the first time in its 40-year history, the Moomba-to-Sydney gas pipeline began to run in reverse. Last September, pipeline operators APA Group completed minor modifications to allow reverse flow. A name change to Sydney-to-Moomba pipeline may now be in order!

This remarkable gas market transformation means companies such as Esso and BHP Billiton are enjoying benefits from the export boom beyond just increased gas prices.

Traditionally, conventional gas production facilities were under-used in summer when domestic gas demand was low. Now summer sales are up as gas flows north to Queensland.

Beyond that, an even more significant cash benefit results from increased production of the valuable liquids found alongside gas: LPG (liquefied petroleum gas) and condensate. These co-products, often more valuable than the gas itself, have had to lie dormant in the ground until this new gas market appeared.

Rising costs for domestic gas users

Clearly, eastern Australian domestic gas users see something wrong with this success story. They must now compete on price with gas exporters who have an overriding need to fill long-term export contracts.

Even traditional domestic gas retailers such as AGL have decided to sell gas to the exporters. Thanks to the interlinkages of our gas market, no eastern Australian gas consumer will be left unaffected.

Some will find it pays to fuel-switch to other energy sources, potentially driving a crash in domestic gas use.

How not to make LNG

Gas flowing north is new evidence that the economic challenges for the direct players in this new industry are mounting. Around the world over the last 40 years, LNG export projects were built where four criteria could be met: the gas destined for conversion to LNG must be easy to produce, come with valuable liquid co-products (such as LPG), have no viable domestic market, and require little in the way of pipeline transport prior to conversion.

Western Australia’s Northwest Shelf project is one example where these criteria were met and investors profited. On the other hand in Queensland, exporting coal seam gas started with one strike against it: coal seams produce no valuable liquid co-products. Never mind that, the project developers hoped to score highly with some of the other success criteria.

Strike two is the learning that coal seam gas isn’t easy nor cheap to produce. As a result, expensive gas must be drawn from 3,000 kilometres away. This is new evidence that the Gladstone LNG projects face ongoing economic challenges to add to past billion-dollar write-downs.

The biggest winners from eastern Australian coal seam gas may turn out to be those gas producers that opted to play a role – but kept a safe distance.