Suppose, a litre of cola costs US$3.15. If you buy one third of a litre of cola, how much would you pay?

The above may seem like a rather basic question. Something that you would perhaps expect the vast majority of adults to be able to answer? Particularly if they are allowed to use a calculator.

Unfortunately, the reality is that a large number of adults across the world struggle with even such basic financial tasks (the correct answer is US$1.05, by the way).

Using Organisation for Economic Cooperation and Development (OECD) Programme for International Assessment of Adult Competencies (PIAAC) data, my co-authors and I have looked at how adults from 31 countries answer four relatively simple financial questions.

As well as the question above, participants were asked questions such as: “Suppose, upon your trip to the grocery store you purchase four types of tea packs: Chamomile Tea (US$4.60), Green Tea (US$4.15), Black Tea (US$3.35) and Lemon Tea (US$1.80). If you paid for all these items with a US$20 bill, how much change would you get?”

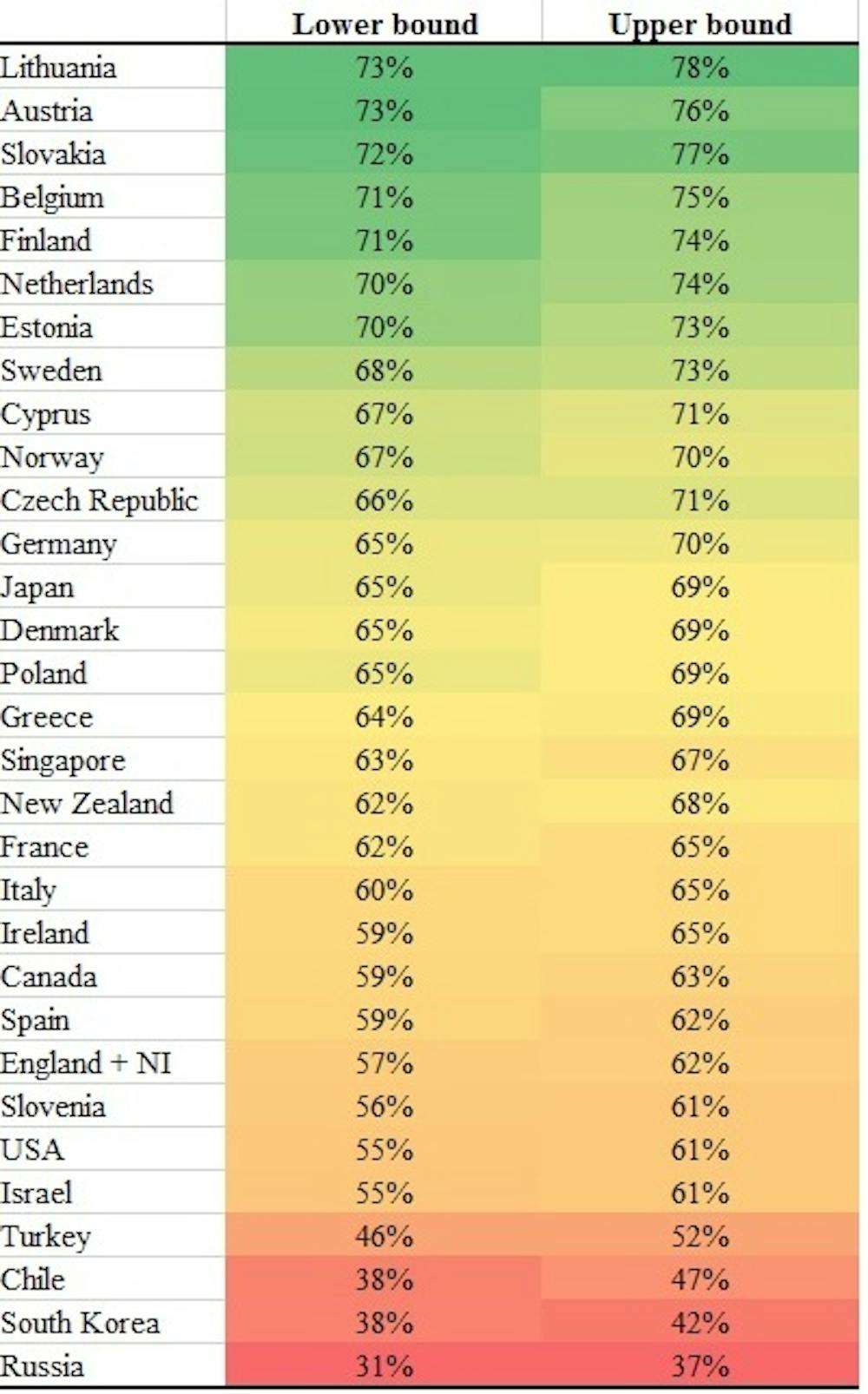

The results (as seen in the table) allowed us to create an estimated range for the percentage of the adult population who would be able to answer the cola question correctly. These results are based upon a random sample of adults from each country.

We found that Lithuania, Austria and Slovakia were the most successful, but even in these countries, one in four adults failed to give the correct answer.

In many other countries, the situation is even worse. Four in every ten adults in places like England, Canada, Spain and the US can’t make this straightforward calculation – even when they had a calculator to hand. Similarly, less than half of adults in places like Chile, Turkey and South Korea can get the right answer.

Basic calculations

Of course, not all groups within each country perform quite so poorly, and there are notable differences in financial literacy skills between different demographic groups.

Across the four financial questions adults were asked, in most countries, men tended to perform slightly better than women. The young (particularly 25- to 34-year-olds) were also found to perform better than the over-55s.

The starkest differences were seen by education group. Returning to the first question given above, in many countries adults with a “low” level of education (the equivalent of completing secondary school) had less than a 50% chance of getting the question correct. In places like Canada and United States, this fell to as low as 25%.

Financial headache

Our results clearly highlight how many adults are ill equipped to make key financial decisions. And how in fact, many struggle to cope with even very simple financial tasks.

In the long term, this highlights the critical need for financial literacy to be taught in schools, to ensure young people are equipped for the complex financial decisions they will face in the real world.

More immediately, though, given the low level of financial skills among many adults, it is vital that the information provided with financial products is as simple and straightforward to interpret as possible. And in the age of payday loans, and high interest credit cards, adequate advice and guidance must also be available where needed. Because otherwise, there is a real danger that a large proportion of the population is at risk of making serious financial mistakes.