Ed Miliband is trying to wrestle back the political initiative in Manchester. The leader of the opposition must avoid becoming mired in deeply complex constitutional questions of devolution at his party’s annual conference – and top of the agenda right now seems to be regaining public trust in Labour’s ability to run the economy.

Ed Balls sought to do that with a keynote speech on Monday which borrowed some of its language on cuts from the coalition government, and there has been a conscious effort to distance the current leadership from the so-called “mistakes” of the past. The problem is that the argument doesn’t stand up to scrutiny, however much it might make electoral sense.

According to Chuka Umunna, Labour shadow minister for business, the UK’s 2010 general election was lost because Gordon Brown failed to make the promise of cuts. Umunna reckons Labour is still struggling to shake off Brown’s Labour legacy of being an anti-cuts party. In Umunna’s opinion, Gordon Brown should have said that the election would be “between Labour cuts and Tory cuts”.

In a recent speech Umunna said:

Gordon Brown dealt a blow to Labour’s economic credibility by wrongly giving the impression in his final year as prime minister that the party failed to understand the importance of tackling Britain’s unprecedented peacetime budget deficit.

Major precedent

Umuuna’s economic analysis requires some factual clarification. First, the budget deficits during the last two years of the Brown government were not “unprecedented” in peacetime. A quite similar fiscal outcome occurred under the government of John Major in the first half of the 1990s, and highlight how much better Gordon Brown handled the situation.

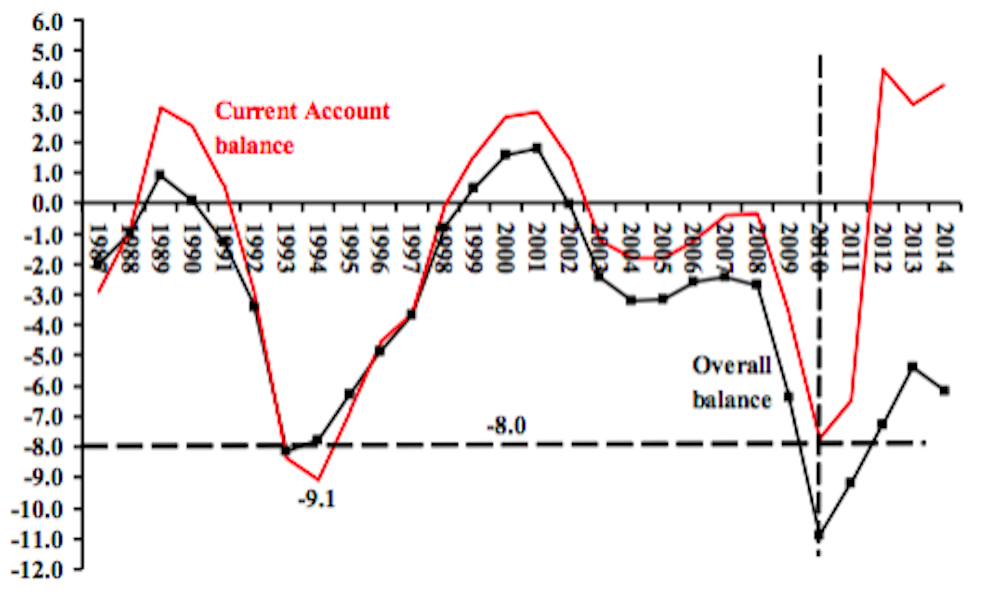

Let’s take a look at the numbers. Which of these deficit experiences was “worse” – 1992-94 or 2009-11 – depends on how you measure the fiscal balance. The chart below traces the values of two fiscal balance measures, the overall balance and the balance on the current account. The difference between the two is expenditure for public investment. The chart shows that for fiscal year 1992-93 the overall balance reached minus 8.1% of GDP, compared to minus 10.9% in 2009-10.

No one can dispute that -10.9% was a larger deficit in GDP than -8.1%. But during the 1992-93 fiscal year the UK economy grew, at an annual rate of more than 2%. In contrast, during 2009-2010 the UK economy contracted by more than 2%.

Relative values

You do not need deep knowledge of fiscal policy to infer that overseeing a large deficit when the economy expands is a considerably worse record that suffering a similar deficit when the economy contracts. Growth should increase revenue, while contraction reduces it. Viewed in context, the fact that the overall deficit in 2009-2010 was just 2.8% greater seems a better than expected outcome.

As any business person knows, borrowing is the rational way to finance investment. If the investment is profitable, the output it generates covers the servicing of the loan taken to finance it. If it is not profitable, the investment should not be undertaken, however it would be financed.

This guideline should apply to governments as well as the private sector. It should certainly be endorsed by those who think that the public sector should act more according to “business principles”. Brown stated his commitment to the borrow-to-invest principle in his first budget speech of 1997, which became known as his “Golden Rule”. To my knowledge no prominent politician in Britain took Brown to task for applying this rule to his budgets.

As the chart shows, the Conservative government during the ten years 1988-1997 were not trying to keep to Brown’s Golden Rule. During the fiscal year 1993-94 the deficit on the current account (omitting investment) reached more than 9% of GDP, compared to 7.7% in 2009-10. The earlier deficit was associated with the economy growing by more than 3% (during 1993-94), while it contracted during 2009-2010.

Finally, when considering which the two deficit experiences, we can consider the implication of the current account deficit exceeding the overall deficit in the mid-1990s. By definition, this means that public investment under John Major’s government was negative (less than the depreciation of public assets). It was not until about 1998 that public investment turned positive. This performance on public infrastructure may explain why Gordon Brown in 2010 would have posed the dichotomy, Tory cuts versus Labour investment.

Heading for a fall

Umunna’s call to “tackle the deficit” by implementing budget cuts implies that if public expenditure falls, the deficit will fall. While this may seem obvious, it is an invalid inference that calls to mind the famous one-liner from US economist Stuart Chase: “Common sense is that which tells us the world is flat.”

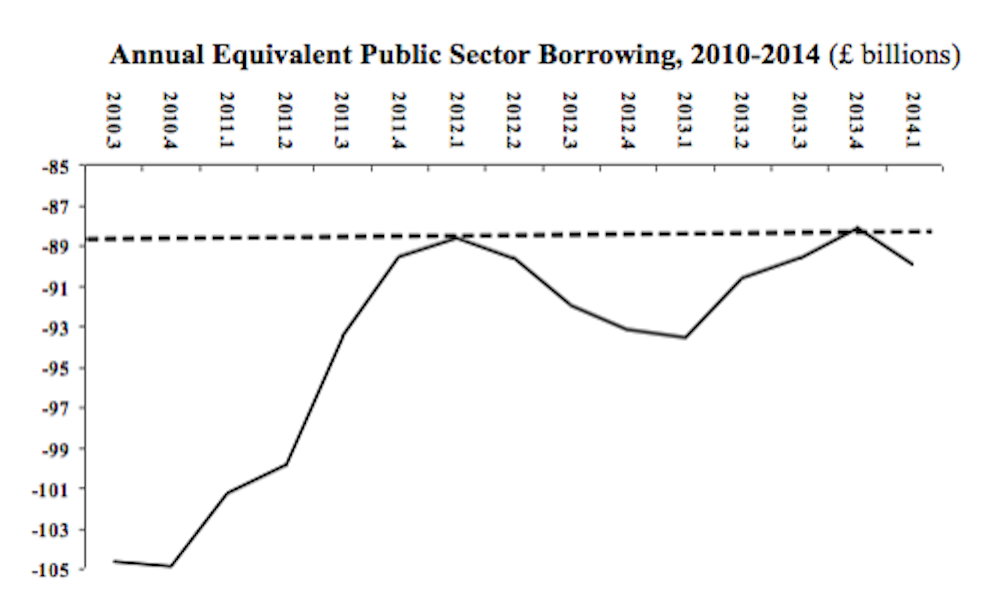

The chart below shows that borrowing declined substantially over the seven quarters from Q3 2010 to Q1 2012. Subsequently, as current chancellor George Osborne’s budget cuts have worked through the economy, there has been no sustained reduction of borrowing.

The Office of National Statistics commented on the stagnation of public borrowing in its March report on public finances:

For the financial year 2013/14, public sector net borrowing excluding temporary effects of financial interventions … was £95.5 billion. This was £14.8 billion higher than the same period in 2012/13, when it was £80.7 billion.

Tax inefficient

The persistence of public borrowing at about £88-95 billion can be explained with the argument Labour had been using: expenditure cuts achieved an initial reduction in borrowing, which killed a nascent recovery that began in 2009 and as a result, the economy stagnated for three years. It boils down to the idea that reducing public expenditure is an inefficient way of reducing public borrowing, because of its feedback effects on the private economy that reduce incomes and tax revenue.

Many commentators have suggested that Gordon Brown was not effective on the campaign trail, which I tend to agree with. But Brown knew his economics, which is why he has consistently disparaged Tory promises of fiscal cuts.

The coalition government implemented the promised cuts, recovery came later than any on record and borrowing flat-lined for two years. However much they want the electorate to trust them with the cash once again, Labour politicians should restrain themselves from contributing to the current chancellor’s PR by suggesting that his cuts will eliminate borrowing. They will not.