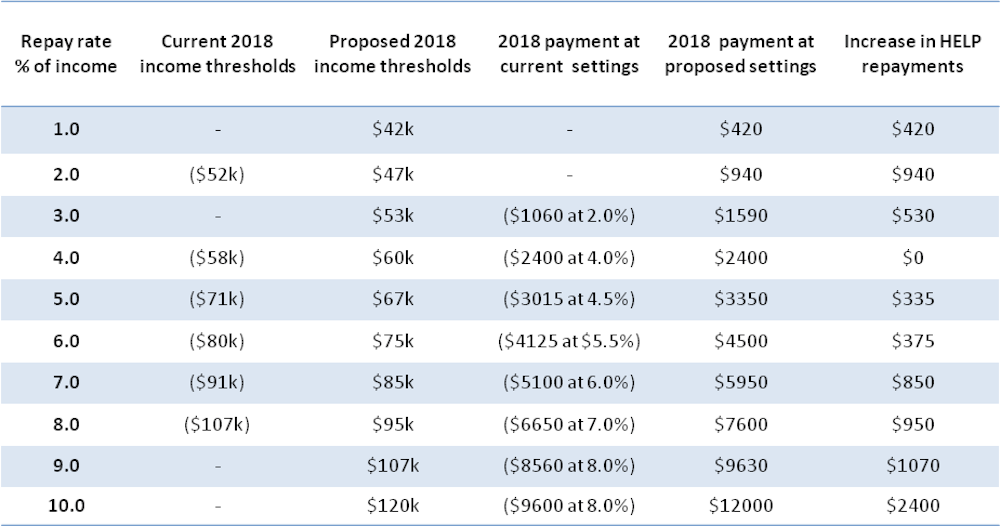

If the Senate passes budget reforms for higher education, Higher Education Loan Program (HELP) repayments would start earlier, with a wider range of rates: 1% of income for those earning A$42,000, rising to 10% at $120,000.

To put this in context, in 2017 the Australian minimum full-time wage is about $35,000 and the average full-time wage about $80,000.

This is an alternative to the government’s 2014 plan to charge real interest on HELP loans, and a 2016 Grattan Institute proposal to apply a 15% loan fee to new HELP loans.

The Grattan Institute has mapped the overall effects of the government’s 2017 proposal.

Grattan’s Andrew Norton supports it, as does the Mitchell Institute’s Peter Noonan. The new settings will curb the rising public cost of over $50 billion in outstanding debt.

Against this, Sharon Bell of the Australian National University warns of more financial stress for students with other debts to manage.

Cash effects of new HELP settings

If passed in the Senate (where views range widely), the changes would apply to existing HELP debtors already in the workforce.

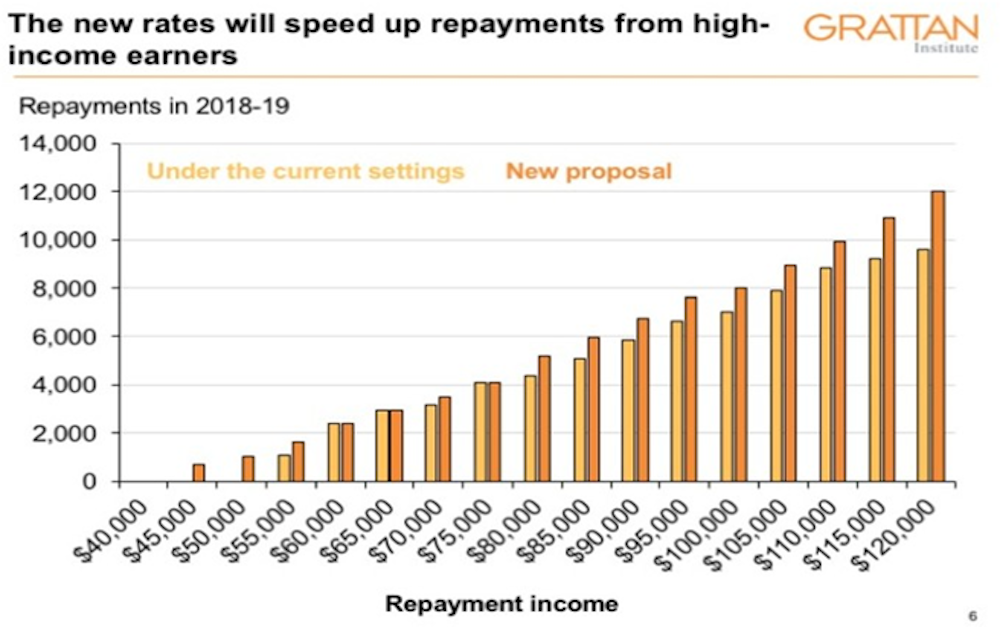

The chart below shows the effect in round figures of these “tax increases” in 2018. It compares minimum annual repayments under existing and proposed settings.

There would be new payments at lower incomes in the $42,000 to $52,000 range.

In the $52,000 to $57,000 range, payments would be 1-2 percentage points higher. The same would apply in the $107,000 to $120,000 range. As the chart above shows, an increase from 8% to 10% at the $120,000+ level has significant cash effects.

The changes are both regressive and progressive.

At lower incomes in particular, a concern for many will be the cash-flow effect of new or larger repayments. Education Minister Simon Birmingham notes that the cash impact at the $42,000 threshold is about $8 a week. But at $47,000 a 2% repayment would cost about $940 in a tax return, compared with zero at current settings.

Should the government consider a super payment option?

The lower thresholds may change in Senate negotiations. But if these are adopted the government should consider adding a “super payment option” that allows graduates to redirect up to 20% of compulsory superannuation contributions into HELP repayments.

This would help graduates manage the cash effect of higher HELP repayments. And those taking it up would confirm that their employers are complying with Superannuation Guarantee obligations.

The background here is that the recent Senate committee inquiry estimated that 2.4 million workers miss out on super entitlements due to underpayments by their employers.

And the Financial Services Council noted recently that many super fund managers assume younger workers are “chronically disengaged” and neither know nor care about their super balances.

Thus the “gig economy” meets the Super Guarantee. Financial Services Council CEO Sally Loane says that changes are needed for an “Uber-ised” millennial workforce:

The competitive superannuation model the Financial Services Council has proposed – which we call Super 2.0 – offers consumers choice between funds, is competitive, flexible and fit for purpose for young Australians entering the workforce. This model can be contrasted with the status quo – our industrial model that encourages disengagement.

Cash-flow effects of super-HELP repayments

The chart below shows the cash effect of letting graduates tap up to 20% of their 9.5% employer contributions under the Superannuation Guarantee to meet HELP debt obligations.

In most cases, doing so would more than cover the increase in payments under the new HELP settings. Graduates could repay debts faster as proposed, but with better cash flow than under the current repayment settings for 2018.

At an income of $42,000 a graduate could choose to meet their full HELP debt obligation that year with just over 10% of the superannuation contribution their employer should pay into their super fund.

At an income of $47,000, tapping 20% of employer contributions would not quite cover the HELP debt repayment increase. Nor would it do so at $120,000.

But at many income levels in between, graduates would actually be better off in cash terms than under the existing HELP settings for 2018.

Should super contributions be used this way?

Using super to repay HELP loans is not a part of the budget measures now making their way through parliament.

The design risk is that such a policy may undermine the aim of compulsory super. Lower contributions translate to lower super balances on retirement. However, those under the age of 30 can reasonably expect to be in the workforce until the age of 70. There is ample time to reinvest in super.

For younger or cash-poor graduates, meeting HELP payments may be a better use of part of the super contributions made on their behalf. It would mean more flexibility to invest in other priorities: credit card debt management, business start-ups and home loans.