Corporate inversions have been front page news in the US for months with everyone from President Barack Obama to the man on the street expressing a view as their usage has surged. Unfortunately, many of these views are not well informed.

For example, most news reports cite the 35% US corporate tax rate as a major cause of inversions. While it is true the US has the highest corporate tax rate in the developed world, it is not causing inversions.

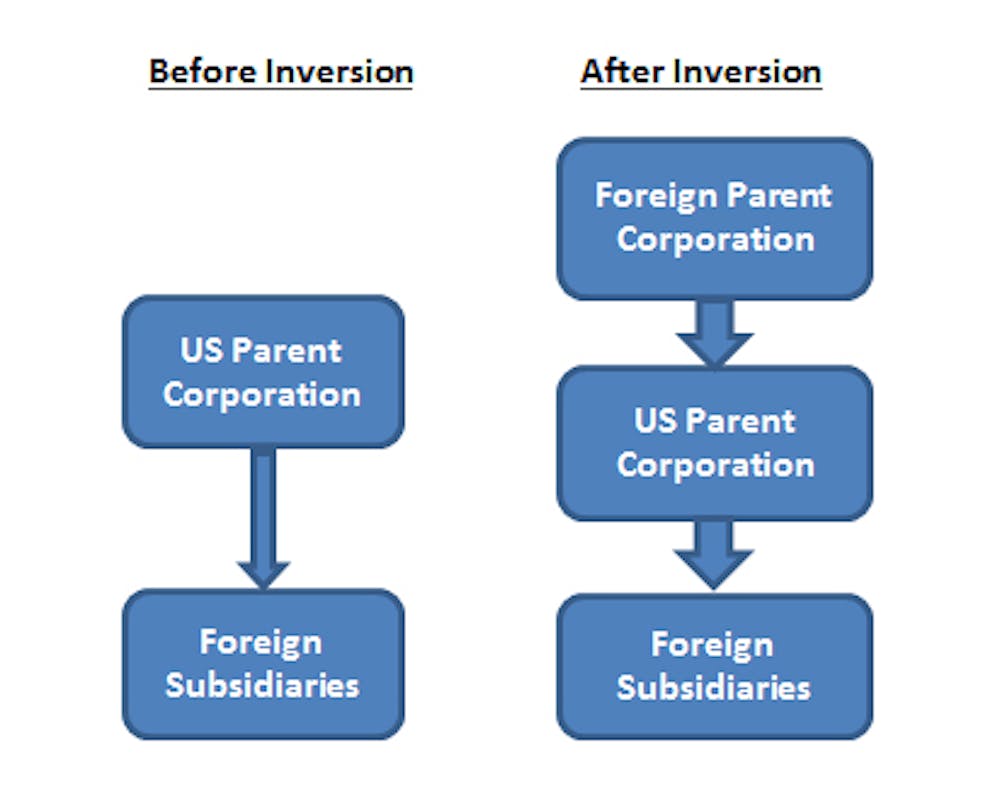

What is an inversion?

Although corporate inversions can take many forms, the end result is that a business previously owned by a US parent corporation is now owned by a foreign parent, as the chart below shows.

In most cases, the foreign parent is an entity with few employees. Thus, an inversion is effectively a legal change of ownership.

It does not mean a business will move its headquarters and employees out of the US – though there is justifiable concern that over time jobs could leave the US.

At least 13 companies that used to be based in the US have completed inversions since the beginning of 2012, compared with six in the previous three years, according to Bloomberg. Six more inversions are pending.

Why companies are inverting

Many have argued companies are pursuing inversions to avoid the bite of the US’s 35% corporate rate, but international tax planners know better. Even if it were miraculously reduced to 15%, US corporations would still invert.

The real reason is that they need access to their cash. Specifically, companies have shifted so much income to offshore tax havens that the US parent needs the cash from foreign earnings to pay dividends and buy back stock.

But there is a major problem: the US parent cannot access the foreign earnings without incurring domestic tax. Tax planners and Washington politicians refer to this as the “lock-out effect.”

Some believe corporations have been hoisted on their own petards because they have shifted so much income overseas. Others argue that they need to do so to remain competitive with foreign corporations. Both views have merit.

Regardless, the bottom line for US corporations is that foreign earnings are needed back at the US parent and they don’t want to pay any meaningful domestic tax on such earnings. Thus, it is the lock-out effect that is driving corporate inversions, not the high US corporate tax rate.

Territorial tax systems

In order to eliminate the lock-out effect, US companies have vigorously lobbied for a “territorial” tax system so that dividends from foreign corporations are not taxed in the US. Since the US is the only major country that has not adopted such a system, companies were initially optimistic their lobbying efforts would be successful.

However, many politicians have been unwilling to adopt a territorial tax system unless there are significant safeguards against shifting their income to other countries. Their fear is that without such safeguards the US corporate income tax could effectively become optional.

The end result is the lock-out effect will not be addressed until there is major corporate tax reform. Such reform could be many years away, assuming it ever takes place.

The lock-out effect?

Inversions are effectively a self-help measure for US corporations to obtain a territorial tax system. Instead of waiting for the US tax law to change, they can invert and access their foreign cash.

For example, assume a US corporation has a foreign subsidiary with US$1 billion of previously accumulated earnings and $2 billion of projected earnings over the next ten years.

First, immediately after the inversion, the new foreign parent could borrow US$1 billion from the foreign subsidiary and incur no US tax. The foreign parent could then use the US$1 billion as it wished.

Second, the new foreign parent could also access the US$2 billion of future earnings without US tax cost. Absent an inversion, the US parent would not be able to access either the US$1 billion of accumulated earnings or the US$2 billion of future earnings without incurring US tax.

The US Treasury, however, stepped into the fray in September and issued new rules intended to give pause to corporations contemplating an inversion. The regulations make it substantially more difficult for the new foreign parent to immediately borrow that US$1 billion from the foreign unit without incurring US taxes.

And in at least one case it succeeded. The US drug company AbbVie, for example, last week canceled its US$54 billion acquisition of Irish-based Shire in what would have been the biggest ever inversion.

Treasury rules will not stop the flow

Although the Treasury rules may stop companies from immediately borrowing the $1 billion in the above example, the potential long-term benefits of exempting $2 billion of future earnings from US taxation are significant.

The bottom line is that as long as a US corporation can materially benefit by inverting, we should expect them to continue. Admittedly the Treasury’s intervention will slow the pace of inversions, but assuming the US does not take any other action, it is reasonable to predict that after 10 to 20 years a substantial number of US corporations will have inverted by one method or another.