The rapid escalation of the situation in Crimea has led us faster than we might have thought to consider if and how Russia might unleash energy policy as part of its geopolitical strategy. President Vladimir Putin has a powerful weapon at the ready, and may feel he already has enough justification to put it to use.

This tactic is easily characterised with the image of a gas pipeline valve being turned off in a Cold War drama – or in the opening credits of a long-running satirical TV panel show. In reality of course it’s not as simple as that. For a start, the Russian economy would be put under significant pressure by the loss of sales from a source that provides around 14% of the country’s export revenues and 5% of budget revenues.

It could end up as a question of timing. Paolo Scaroni, the CEO of Italian oil and gas giant ENI, has pointed out that the short-term impact would be felt rather more severely in Europe. The continent needs Russian gas today whereas Russia can survive without our money for weeks if not months.

A key question must be whether Russia would be at all motivated to pursue a gas war by turning off the flow of exports proactively. It would perhaps be more likely, and more subtle a tactic, to use the commercial rights in its 2009 export contract with Ukraine to put the blame for any gas crisis on someone else. It is an uncomfortable fact for both Ukraine and the EU that the contract has already been breached, offering Gazprom every opportunity to create problems if it so desires, or if it is encouraged to do so by the Kremlin.

Contract wrangles

Under the terms of the 2009 agreement not only was a high gas price agreed but Ukraine was also obliged to accept a take-or-pay clause and to guarantee prompt payment. It is now in breach of both these clauses, allowing Gazprom to take action if it wishes. The deal stipulates that Ukraine must take (or pay) a minimum of 80% of the contracted annual volumes of 52 billion cubic metres (bcm), implying a minimum purchase of 41.6 bcm that was clearly missed by a huge margin in 2013, when 27 bcm was bought. Although the clause was removed in December, when a new much lower price deal was signed, it could return if the original terms are enforced again.

More urgently Ukraine has a US$1.8 billion debt to Gazprom for gas purchased in 2013 and the first quarter of 2014 that is set to rise further as more gas is bought. Ukraine has made some repayments this year but the remaining total remains well beyond its ability to repay in the short term.

In terms of the price Ukraine must pay, Gazprom has already made it clear that it will revert to the arrangements under the 2009 agreement, removing the discount agreed in December. It has also stated that it will no longer offer a further discount for the lease that allowed Russia’s Black Sea fleet to remain at Sevastopol.

This combined change would see the price more than double to about US$475 per one thousand cubic metres from 1 April, lifting Ukraine’s monthly bill to around US$0.5 billion for every billion cubic metres purchased. Ukraine could try to restrict its imports by using gas in storage, but this would only delay any shortages for a few months until winter approaches, by which time storage levels should have been increased, not reduced, if a crisis is to be averted.

All this means that if Gazprom insists Ukraine must reduce its debt and pay for current purchases more promptly, it could force a financial situation which offers the commercial and legal justification for halting gas supply. That in turn would leave Ukraine with very limited options, one of which would be to take gas that is destined for European customers, as happened in 2009.

Europe under pressure

Indeed, Gazprom CEO Alexei Miller has hinted at this strategy already, stating in early March: “we can’t supply gas free of charge. Either Ukraine repays its debt and pays for current deliveries or the risk of returning to the situation at the beginning of 2009 will appear.”

Clearly the problem could be alleviated if the EU or IMF come up with a financial package to support Ukraine, or if a rapid resolution can be found to secure gas via reverse flow from Europe, but at the very least Russia would have forced some awkward political and commercial questions to be asked, while arguing that its stance is based purely on commercial agreements.

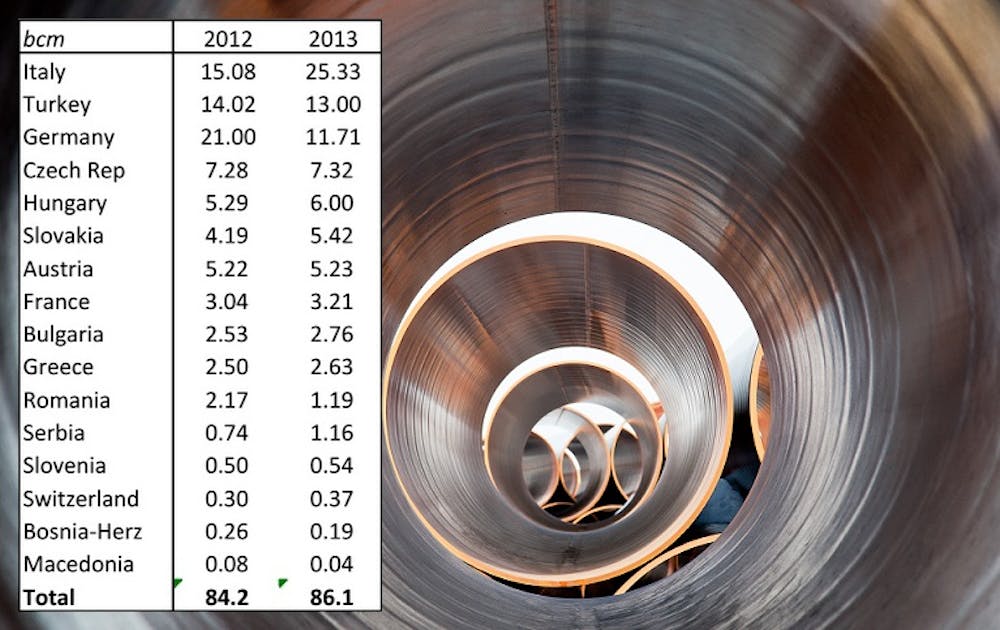

As the table above helps to show, the impact of any interruption to Ukrainian transit, were it to occur, would mainly be felt in south-east Europe. Supplies into the north of the continent could, to some extent, be re-directed to alternative pipelines.

Nevertheless, Europe overall has become more reliant on Russian gas in 2013 thanks to a tightening of the liquefied natural gas (LNG) market and a fall in North African exports on the back of political crisis in the region. About a third of Europe’s gas supply, or 162 billion cubic metres of gas, was purchased from Gazprom last year, up from 139 bcm the year before. With no significant new LNG likely to be available before the end of 2015 at the earliest (when the first US LNG is exported) it would seem that Europe’s dependence is set to continue.

At the very least, therefore, any interruption in supply would cause a price spike for all consumers, but it is Greece and Romania that would appear to be particularly exposed to a disruption in Ukraine. They have no reported storage, although Greece at least could increase LNG imports. Bulgaria and the Czech Republic have sufficient gas to cover only around 50-60 days of lost Russian gas imports, while Hungary and Slovakia are better placed and could cover more than 100 days. Italy is also relatively secure in the short term as not only does it have adequate storage but it is also now well connected with the main European pipeline systems and also has spare LNG regasification capacity that could also be used to supplement supplies (although at high global LNG prices).

As a result, although an interruption would be serious it could be managed, at least in the short term. The major concern, though, would be that stocks would need to be drawn down at a time when they would normally be replenished ahead of the winter, meaning that in reality a crisis would not be averted but rather postponed until the autumn.