Scotland will receive major new fiscal powers from the Scotland Bill working its way through Westminster. Holyrood will get more control over income tax, some welfare powers, and will be assigned half of VAT receipts – all the result of the Smith Commission agreement by the five leading Scottish political parties that followed the independence referendum that saw Scots vote to remain in the UK.

A key element of the bill is the fiscal framework, which will set out how the new fiscal powers will function. One crucial part is how the transferred powers and benefits will affect the block grant which the Scottish parliament receives from London. The Smith Commission agreement was clear that this grant should continue to be calculated using the Barnett formula, which allocates funding to the devolved nations of the UK according to their population size.

The block-grant determination should satisfy two “no-detriment” principles that were also part of the agreement. First, there should be “no detriment [to Scotland or the UK] from the decision to devolve” additional powers. Second, there should be “no detriment [to Scotland or the UK] from subsequent policy decisions of the other government”.

Adjusting the block grant in a way that satisfies these principles is difficult. The first principle suggests that the devolution of new powers should not disadvantage Scotland – meaning it has to encourage the Scottish parliament to grow its tax base, for instance. In other words Holyrood should gain funding if Scotland grows its tax take faster than the rest of the UK, and lose funding if it falls behind.

The second no-detriment principle suggests that if the UK or Scottish governments alter any taxes this should not have knock-on consequences for the other jurisdiction: a difficult hurdle given that any spending or tax decisions will impact on other areas of spend and revenue.

The adjustment debate

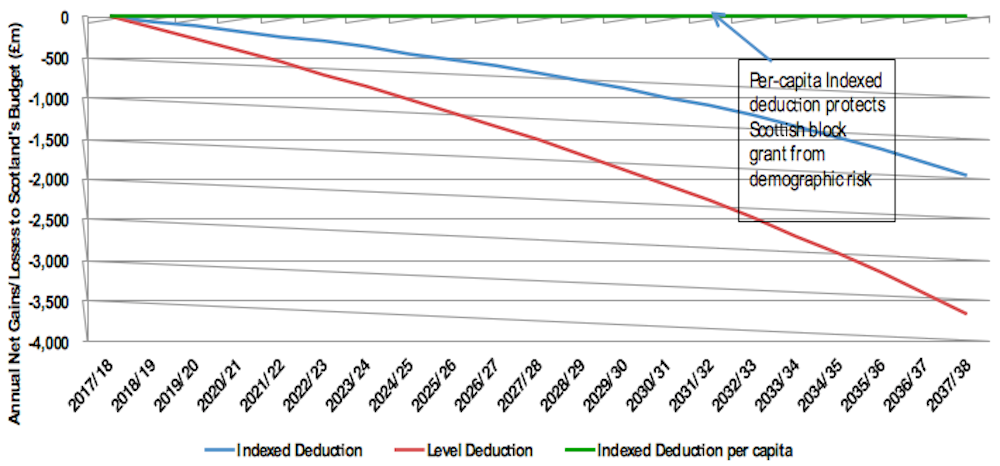

How best to adjust the grant is still up for discussion. I recently suggested we should use a method called per capita indexed deduction. This would encourage the Scottish parliament to grow its tax base without exposing Scotland to the risk that its tax take falls behind because its population is growing more slowly than the rest of the UK. This is exactly what the Office for National Statistics (ONS) is currently forecasting. If the grant is instead adjusted using one of the other two options on the table – levels deduction and indexed deduction – Scotland would have less protection. In the case of levels deduction this happens because the block grant is linked to a population share of changes in UK taxes, which is less than per capita receipts in Scotland. Hence the block grant adjustment takes out more from the budget than is being added back in devolved taxes.

The graph below shows how each method could affect Scotland’s block grant. It assumes that Scotland matches the rest of the UK’s economic performance and that populations grow in line with current ONS projections. In this scenario, Scotland would lose approximately £7bn from its block grant at 2017-18 prices in the first 10 years of the new powers if the levels deduction method were used; or almost half that if it used indexed deduction.

The reason why per capita indexed deduction should be adopted is that Scotland doesn’t have the powers to control its net migration. It would be unfair to expose it to risks that are managed by the UK government, especially as UK demographic trends are so dominated by London and south-east England.

One common counter-argument is that the method would be unfair to taxpayers in the rest of the UK and would therefore violate the second no-detriment principle. For example, suppose the UK government wanted to increase spending in an area like health which is devolved in Scotland, and funded this entirely by increasing income tax south of the border. Using the method, Scotland’s grant would rise even though Scottish taxpayers were not paying for any of it. This is because the method would cut the Scottish block grant by less than the increase it received at the same time under the existing “Barnett consequentials” rules that determine how devolved nations’ grants are affected by budget changes in London.

But the second no-detriment principle is almost impossible to satisfy. It would sometimes be violated even with the other adjustment methods, because of complex interactions between UK government actions on reserved and devolved taxes and taxpayer behaviour. Suppose for instance the UK government was to fund a cut in a reserved tax like corporation tax by raising the rate of income tax south of the border. The Scottish block grant would shrink under all three adjustment methods, reducing the Scottish government’s spending power – unless the consequences of each action are measured and offset separately.

Furthermore, even though the per-capita indexation method doesn’t address the second no-detriment principle fully, it gets close to doing so. It does not induce a systematic gain in the Scottish budget (Scotland would lose in the above health spending example if the reverse happened and the UK government were to cut income taxes and health spending).

Making the new system viable

There are other issues to be dealt with in the fiscal framework, not least the borrowing powers which the Scottish parliament should have to smooth tax revenues and fund capital spending. There are also issues around how Scotland’s share of VAT revenues will be estimated; how the initial adjustment in the first year of the new powers should be made; and how the block grant should be adjusted in response to the additional welfare powers – do you use a similar method as for the tax powers, or a different one?

Getting the fiscal framework right is as important as the Scotland Bill itself. If we get it wrong it could seriously penalise the Scottish parliament’s budget and cause major political acrimony between Scotland and the UK. It would undermine the spirit of the Smith Commission agreement, which aimed to make Scotland more fiscally accountable without causing it any detriment.

And even once the new regime is up and running, there will be issues around how to carry it out in practice. In my view, the UK and Scottish governments should hand the power to settle disputes to an independent fiscal arbitrator. It is critical that the Scotland Bill and fiscal framework are seen to work fairly for both sides. The Treasury must not be seen as both a participant and arbiter. There is already a tradition of independent fiscal scrutiny in Scotland and the UK through the Scottish Fiscal Commission and the Office for Budget Responsibility (OBR). Appointing an independent arbitrator might lay the foundations for a more federal system of fiscal governance in the UK, which would benefit the whole country.