In the third in my series on the crisis besetting the National Electricity Market (NEM) in eastern Australia (see Part 1 & Part 2), I look at some evidence for how the market itself has played a role and specifically market power issues.

The recent troubles in our electricity market are well documented. As described in my earlier pieces in this series, two elements have focused the attention of our political masters and industry groups.

The first is the question of security, highlighted most dramatically by recent “black outs” in South Australia.

The second is the question of price, with both wholesale and contract market prices having risen dramatically across most regions in recent times but nowhere quite as dramatically as in Queensland (note that retail prices have also been rising as highlighted by the recent Grattan report).

As discussed in Part 2, the tightening of the demand-supply balance in Queensland in response to an additional ~800 megawatt load from the massive CSG field developments and LNG export processing facilities partly explains the rise in wholesale or pool prices there, but it is far from the full explanation.

Lurking in the details are issues to do with the very functioning of the market, and the exercise of market power by large generators who are able to exploit monopoly rents.

Concentrated power

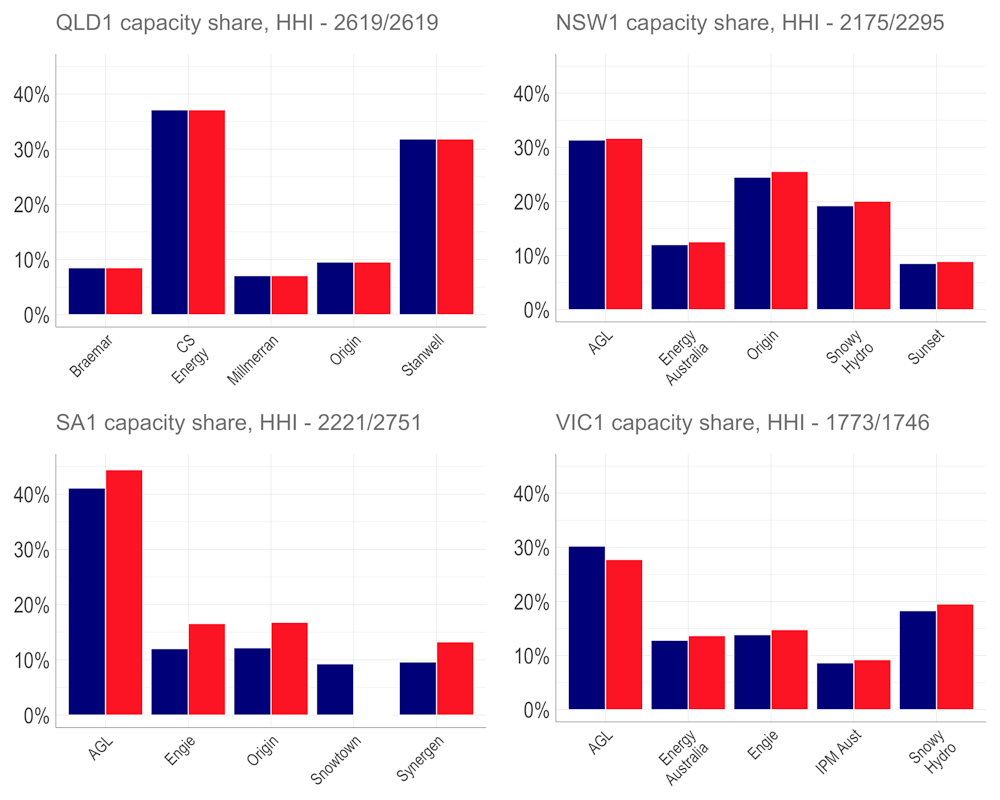

As shown below, ownership of generation assets across the NEM is very concentrated. AGL is the dominant player in New South Wales, Victoria and South Australia, while the state owned Stanwell and CS Energy command almost 70% of Queensland generation capacity.

The Herfindahl-Hirschman index (HHI) is a commonly used measure of market concentration given by summing the squares of the percentage market shares for all participating firms. A HHI of 10,000 is equivalent to a 100% share, and represents complete monopoly. A HHI of 2000 is used by the Australian Competition and Consumer Commission (ACCC) to flag competition concerns. The UK’s Office of Gas and Electricity Markets (OFGEM) regards an HHI exceeding 1000 as concentrated and above 2000 as very concentrated. With a current HHI value of 1243, the OFGEM considers the UK wholesale electricity market somewhat concentrated.

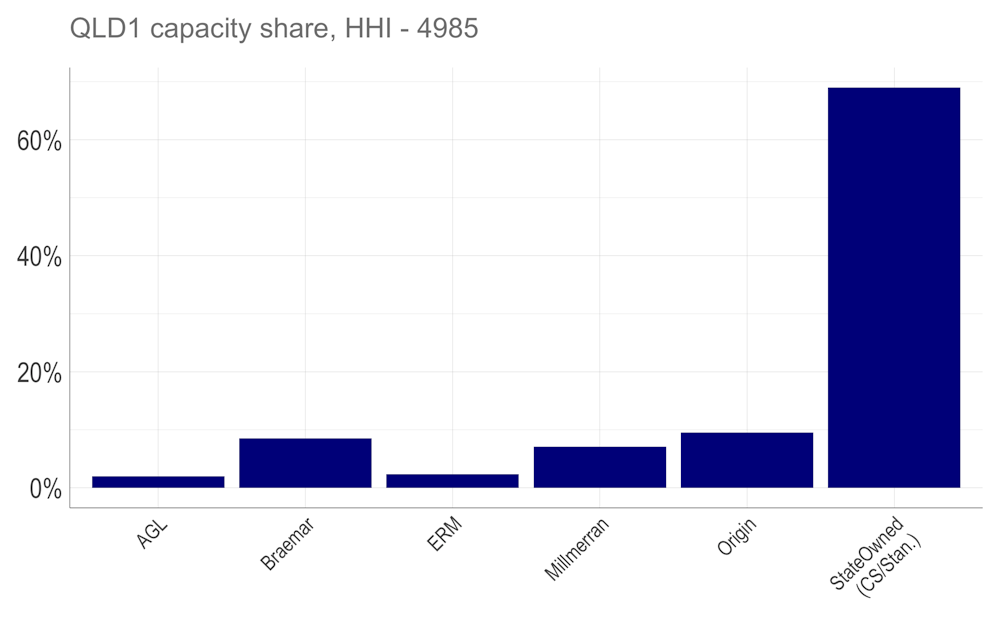

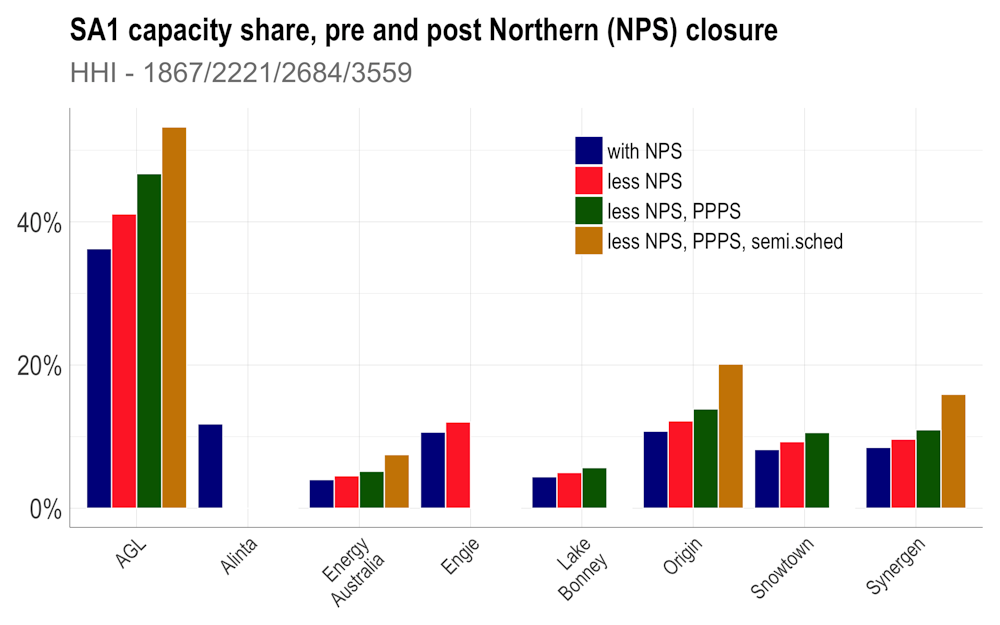

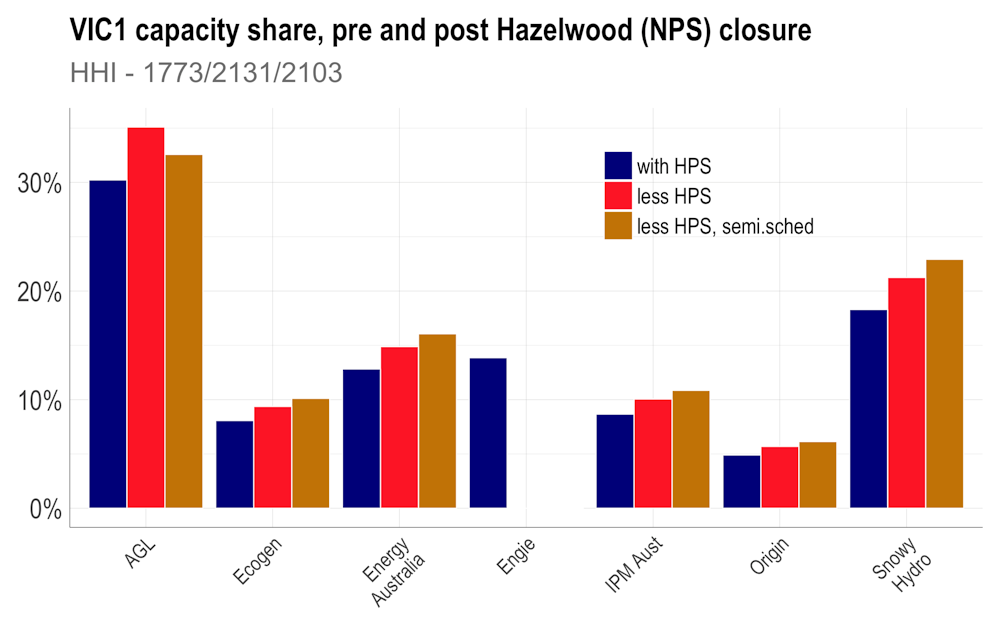

With notional HHI’s in the range ~1800-2600, the regions of the NEM vary between somewhat (VIC1) to very (QLD1) concentrated. Queensland is a particular issue since the two dominant generation entities, Stanwell and CS Energy, are both state-owned. As shown below, aggregating them yields an effective HHI of ~5000, which amounts to extreme market power.

The impact of intermittent wind generation, or semi-scheduled generation in NEM-speak, on market power depends on the structure of assets held by participants. In South Australia the HHI rises in times of low output because AGL holds a relatively minor proportion of that region’s wind assets. Contrawise, it declines in Victoria because AGL holds a much higher proportion of the total wind assets.

Interconnection serves to reduce market power, by allowing more competitive pressure. For example, the 650 MW Heywood interconnector between South Australia and Victoria helps ameliorate market concentration issues. This is especially important for the relatively small market of South Australia, though perhaps not as much as might be possible, given AGL holds the dominant market share in both regions.

As discussed further below, recent and proposed closures of coal fired power stations, such as Alinta’s Northern Power Station in South Australia and Engie’s Hazelwood Power Station in Victoria, have or will effect more concentrated market power.

A rule change

As described in the Part 1, the NEM is designed to signal changes in the balance of demand and supply via spot prices. But how much the prices respond is very dependant on the level of competition.

Recent experience of market participants flouting the spirit of the rules shines a light on competition issues and highlights a rather obvious, if somewhat trite, reality. That is, the benefits of competitive markets can only flow if markets are competitive.

The exercise of market power has been a perennial issue in the NEM. It is the role of the Australian Energy Market Commission (AEMC) to set the rules that allow for safe operation of the electricity network, and efficient operation of the market. It is the job of the Australian Energy Regulator (AER) to do the enforcing, while AEMO operates the market.

The AEMC periodically adjusts rules so as to minimise the impact of perceived or real anti-competitive behaviour. It did so most recently in December 2015 with the Bidding in Good Faith rule amendment because, to quote:

… The Commission considers that the current rules do not set adequate boundaries on the ability of some participants to influence price outcomes to the detriment of others. This is not reflective of an efficient market.

The statement “ability … to influence price outcomes” is key. It expresses AEMC’s concern that some participants have sufficient market power to extract so-called monopoly rents.

To fulfil my aim of providing a pictorial guide to the market power issues that motivated the rule amendment, it’s advisable (but probably not essential) to delve into the details of two intervals on which the market operates more so than discussed in Part 1. The two intervals are the five minute dispatch interval and the half hour trading interval.

Some arcane detail

(Warning, do skip to the next section if you would prefer to pass on the detail, as it is technical! It provides the background to why lines should be horizontal on the graphs discussed below, and the significance when they deviate).

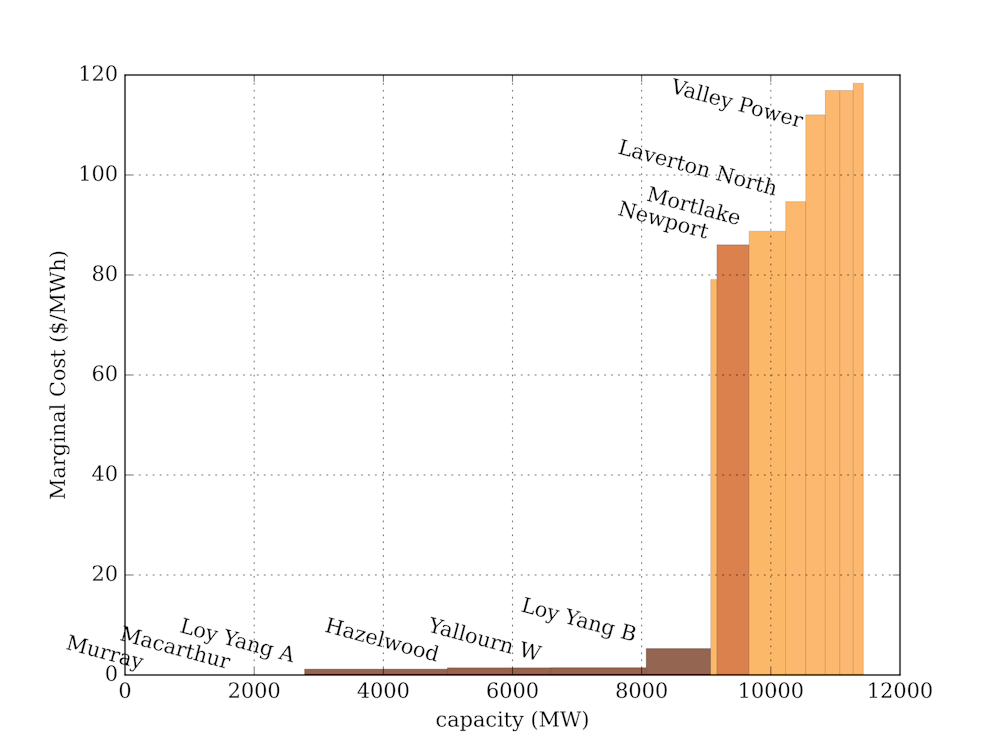

The five minute dispatch interval is where the physics of the power system (balancing supply and demand in real time) meets the economics of the market (serving demand at minimum cost). Functionally, our energy market operates by pooling offers from generators and allocating dispatch for each five minute interval in order of increasing offer price.

A generator offer specifies the price and quantity of electricity that will be supplied in a given trading interval, if needed. The dispatch price is set by the last (highest-price) offer needed to meet the dispatch interval demand. All generation dispatched receives the same dispatch price, regardless of the offer price. Offers at prices above the dispatch price are not needed and so receive nought. To ensure a slice of action, theory has it that generators will offer the majority of their capacity at their short run marginal cost, at prices like is shown for Victorian generators in the figure below.

In practice, individual generators apportion their capacity into a range of price bands. They are then allowed to rebid some capacity into different price bands at short notice allowing adjustments to unforeseen circumstances that periodically arise. AEMC’s Bidding in Good Faith rule amendment requires a justification for any late rebidding within 15 minutes of the start of the relevant dispatch interval.

The second interval is the half-hour trading interval or settlement period, across which dispatch prices are averaged to obtain a spot or settlement price, so called because it is the period on which financial payments are settled.

Since demand normally varies only slightly across a given half hour trading interval there should be little difference in the dispatch prices across the six corresponding dispatch intervals, especially when averaged over many such intervals. In an efficient market with generators offering the bulk of their capacity at near their short run cost, this trading interval averaging should not materially affect the financial outcomes of the market.

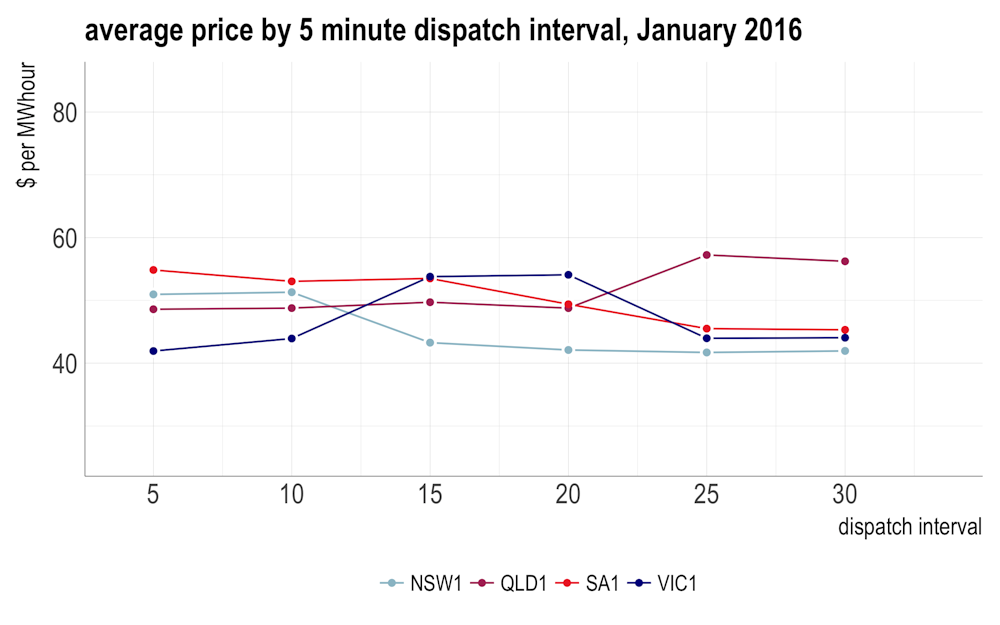

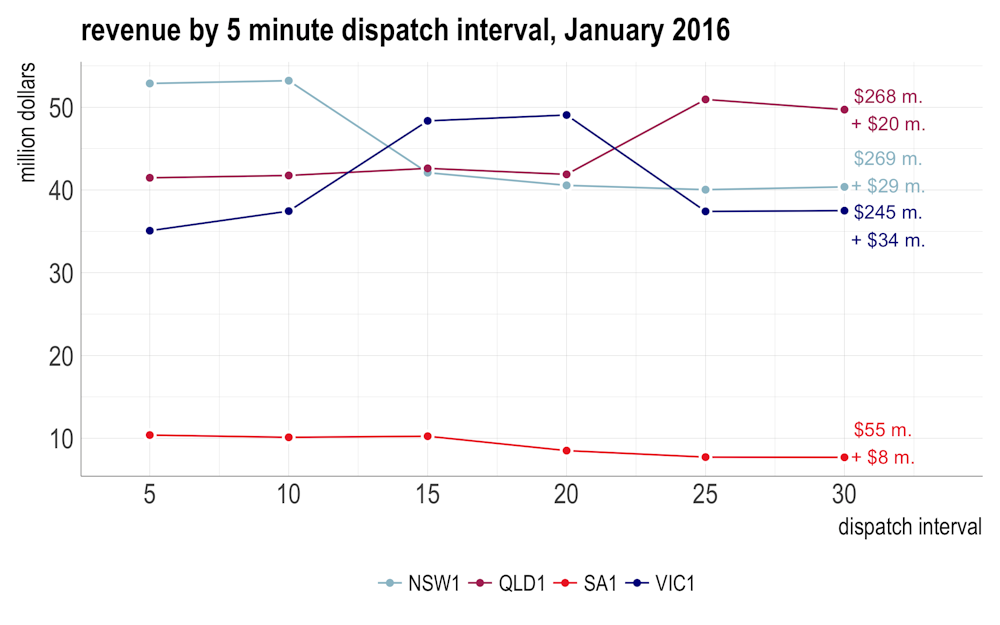

The figure below provides an illustrative case. It shows the dispatch prices for each dispatch interval averaged across January 2016. The narrow range of variation, and flat trace, meets the expectation of a well functioning market.

As revenues are the product of price and demand, their graph should similarly trace a flat line across the dispatch intervals, as it did for January 2016.

In a deregulated market like the NEM, optimal bidding is ensured primarily by the discipline of competitive forces. By preventing profiteering or gaming, it is that discipline that should ensure the lines in these figures lie flat. It goes without saying, that without adequate competition, there can be no such insurance, and one of the signals can be found when plots like these deviate from horizontal. Then, the only recourse is to impose rules on the market. The period shown in the figures above are for the first month following AEMC’s bidding in good faith rule amendment.

Why two intervals?

While the existence of a five-minute dispatch interval is essential to balance demand and supply in real time, there is no compelling reason for the exercise of a half-hour trading interval, it being something of a historical artefact. Interestingly, judging by submissions to a current proposed rule change that would dispense the trading interval, operators of our large generators seem to love it.

Why so? The cynic would say because the existence of the two intervals affords a convenient guise to engage in profiteering. For example, by rebidding capacity into higher price bands late in a trading interval, pool prices can be raised significantly. While such a material distortion of the market would only immediately impact un-contracted customers trading directly on the wholesale market, as explained in Part 1 any sustained price impact will pass through the contract markets thereby eventually affecting all customers.

So where is the evidence?

Do some participants engage in such profiteering? Well the AEMC certainly thought so, enough at least to amend the Bidding in Good Faith Rule in December 2015.

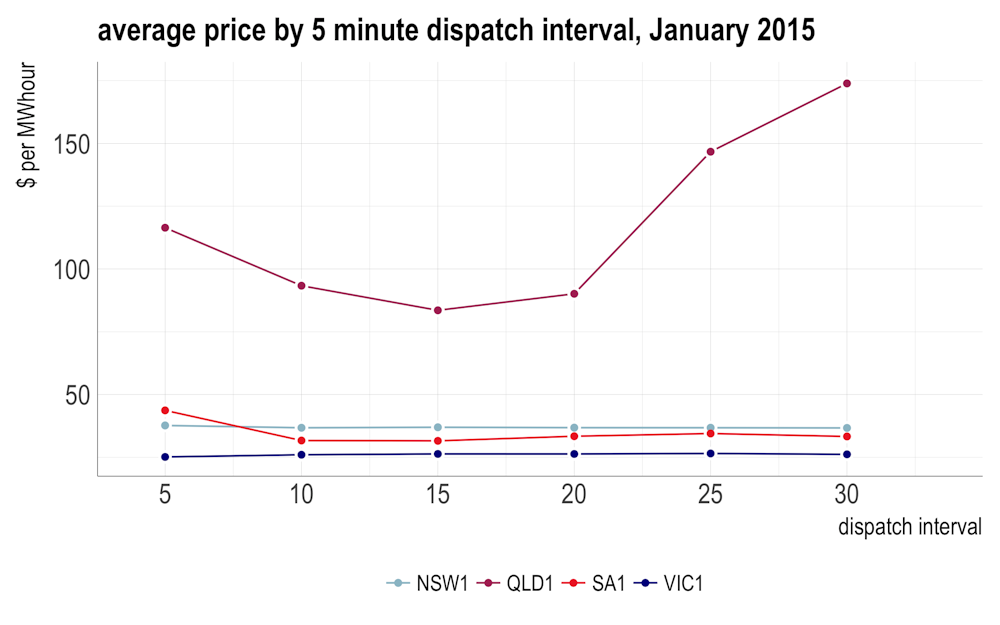

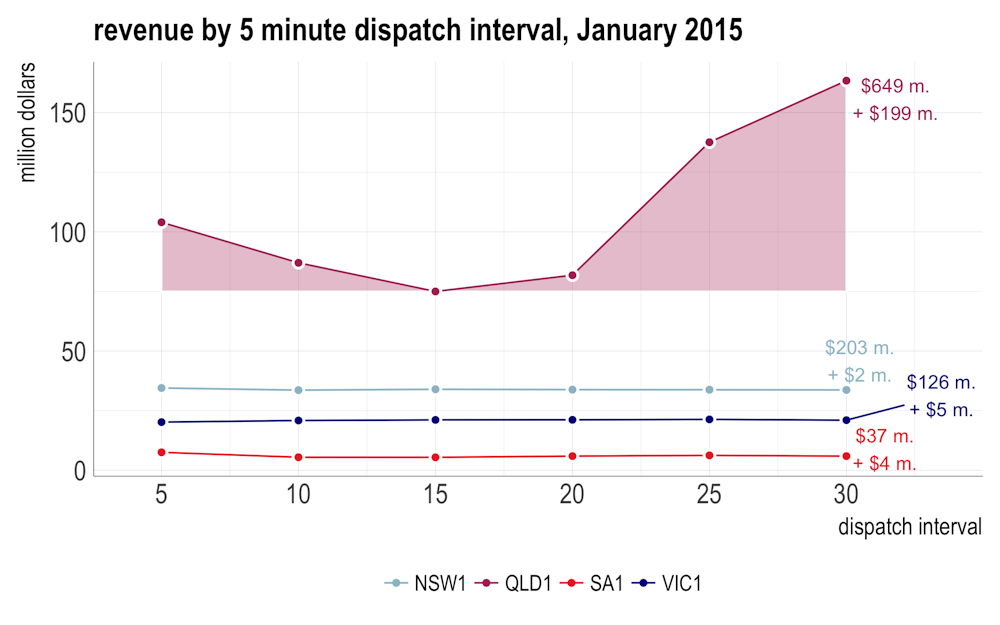

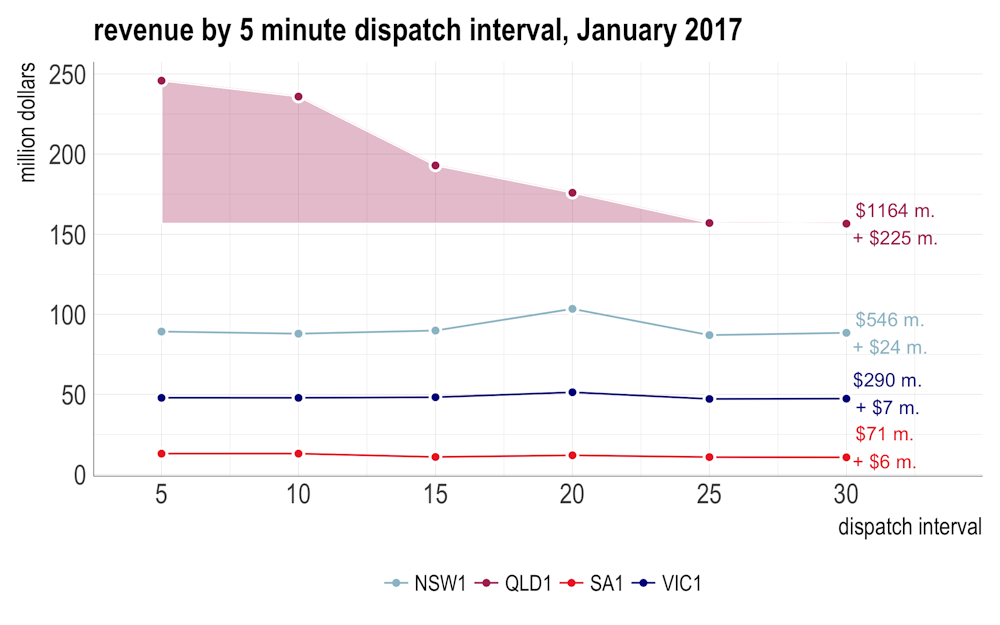

The AEMC was particularly concerned that such practices were impacting market outcomes in Queensland. The smoking gun lies deeply buried in the gory details of the offers and rebids, as documented in AER’s “State of the energy market 2015” report on page 49. But the pointers are quite apparent in the figures below which cover the month of January in 2015, prior to the AEMC’s rule amendment. They show the prices and the revenue by the five minute dispatch interval . The striking feature is the asymmetry in Queensland (QLD1) price and revenue distribution, increasing very substantially across the last two dispatch intervals, compared with the earlier intervals. As explained above, the distribution should be flat, like it is for the other states in January 2015.

A crude estimate of the excess revenue generated by the anomalous market behaviour in Queensland is given by the shaded area in the revenue verse dispatch interval plot below. As noted on the right, it amounted to some 30% of total market value, or ~ $200 million across the month.

By these metrics the magnitude of the Queensland anomaly is astounding, amounting to ~150% of the total revenue in the similarly sized Victorian market and adding as much as $40 per megawatt hour to Queensland spot over the month. The AEMC interest in a rule change is hardly surprising. To my mind they were a little conservative. To quote from AEMC’s rule determination:

… the price volatility that arises from deliberately late rebidding … [is] … estimated to have added around eight dollars per megawatt hour to the price of caps in Queensland in the final quarter of 2014, and around seven dollars per megawatt hour in the first quarter of 2015. Across the market, this represents additional expenditure of approximately $170 million.

Whatever the final accounting, Queensland customers should have been outraged. In conclusion the AEMC noted

… While it is not guaranteed that the changes to the rules will put an immediate stop to the conduct of concern, they are a proportionate response to the issue, and ought to make it easier for the AER compared to the current arrangements to take enforcement action in respect of deliberately late rebidding. At the same time, they should not prevent rebidding in legitimate pursuit of commercial interests.

Should we ask did it do so?

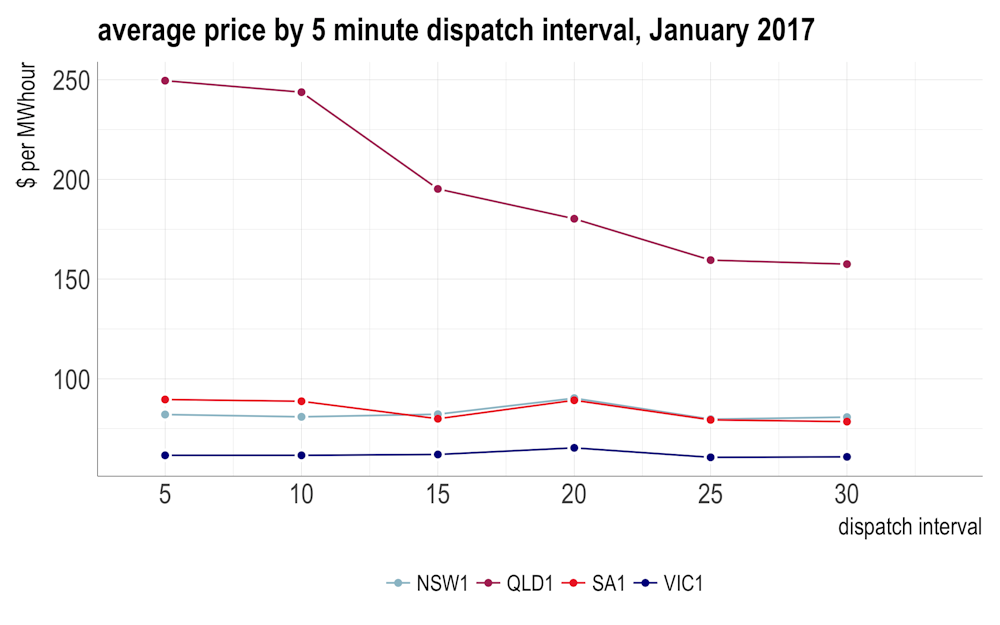

The answer is shown in the figures below, for January 2017. Essentially they are the mirror image of the January 2015 scenario, seemingly implying Queensland generators are now initially bidding in capacity into elevated price bands in the early dispatch intervals. Whatever the strategy it is achieving an almost identical outcome to 2015. Even if entirely within the rules, it would seem not in the spirit. The substantive result is situation normal for Queensland customers, with a $225 million monopoly rent extraction for this past January accompanying unprecedented spot price rises.

Concentrating power

There is such a lot to be said about this, and hopefully it will be. Queensland customers should be beyond outrage. The analysis provided above is but one, easily illustrated example of the exercise of market power. There are others, as for example described in the notes below [2]. From the perspective of this discussion it is illustrative of significant deficiencies in the current operation of the NEM. Those deficiencies are exacerbating our current energy crisis. A concentration of market power is adding materially to costs especially, but not only, in Queensland.

It is worth noting that the half-hour settlement period is currently under review by AEMC and, against the wishes of most established operators, will likely be scrapped [1]. Whatever is decided by AEMC, the underlying issue of market power cannot be addressed by tinkering with the rules. The concentration of market power is increasing as old power stations such as Alinta’s Northern Power Station in South Australia and Engie’s Hazelwood Power Station in Victoria are closed. For example, following closure of Northern, AGL’s proportion of registered capacity in South Australia increased 5% points, from 36% to 41%, improving its relative market power by more than 10%.

Following the closure of Northern, as well as the decision by Engie to mothball the Pelican Point Power Station, AGL played its hand ruthlessly during the first of the South Australian energy crises in July 2016 [2]. With the closure of Hazelwood in a few weeks, AGL will again be the beneficiary of increased market share in Victoria. Although not to the extent it was in South Australia, it will increase the likelihood of AGL being a necessary or pivotal supplier in future high demand events in Victoria. How AGL responds will be a key to how steeply prices rise in Victoria and neighbouring states.

Some reflections

A key objective of the NEM’s energy-only market is to bring competitive pressure to bear on wholesale prices. Until recently the NEM was performing quite well in this regard, with wholesale prices and volatility being very low in the period 2009-2014 in historical terms (see Part 2). But this has changed over the last few years, with a tightening of the market. Like with any industry, our electricity generators have shown adeptness at exploiting the opportunities availed by the market rules. Because of the concentrated nature of the market they have been able to influence price outcomes beyond what would be expected for an efficient market response to such tightening. In so doing they are helped provoke the current energy crisis.

One could only wish our generators turned such “adeptness” to helping drive our energy system to a place we need it to be, that is secure, affordable and with much, much lower emissions. To be so guided, our market rules will have to be radically reshaped to be more aligned to the national interest, explicitly including all three elements of our energy trilemma, and ensuring adequate levels of competition allow the benefits of the deregulated market flow to all participants.

Sadly, as our energy crisis has unfolded, partly in response to the need to address its emissions intensity, emissions have begun to rise again. Just by how much we do not know, as I will discuss in the next piece in this series.

Notes

[1] As Dylan McConnell has shown, the current rules also seriously disadvantage the economics of a number of emerging technologies such as battery storage, hindering innovation that would serve much needed competitive discipline into the market.

[2] For example, on page 51 of its “State of the energy market 2015” report , the AER documents the role of Snowy Hydro’s strategic bidding of its Angaston plant in South Australia on June 10th 2015 to manipulate price. In our analysis of the July 7th event in South Australia, we analysed the extent to which AGL bid capacity to high price bands (typically the market cap price) for the Torrens Island A Power Station. We also looked at the proportion of capacity that was available below and above $300/MWh. In aggregate, Torrens Island A offered its entire capacity to the market at less than $300/MWh 96.5% of time in 2015. For the remaining 3.5% of the year (or about 300 hours) some capacity was pushed into high price bands. Our analysis shows a correlation between periods of high scheduled demand and Torrens Island A’s bidding of capacity into high price bands. The proportion of time when some capacity was priced above $300/MWh is clearly skewed to times of high scheduled demand. In 2015, for the top 10% of scheduled demand periods, the amount of time some capacity was bid into these high price bands was 16.7%. For the top 1% of scheduled demand periods it increased to 35%. On July 7th 2016, it is clear is that Torrens Island had bid an unusually high volume of capacity at the market price cap, at a time it was needed to ensure supply as a pivotal supplier, consistent with exercising market power. While there is nothing in the rules to prevent this, the lack of appropriate competitive discipline means significant market distortion accumulated.