“Life imitates art far more than art imitates life,” according to Oscar Wilde. No more so than in the contemporary issue of debt. It seems that while we may have been born free, many of us will die financially indebted. The precarious austerity economy is kept afloat by endemic domestic debt – from students taking out ever larger government-backed loans, to the cash-strapped taking advantage of a proliferation of short-term loan companies.

Names such as Wageme or Wonga represent the quick and dirty, pay-day end of the loan market. With some companies charging 7,000% interest on loans, according to the Bureau of Investigative Journalism, the Wildean parallel in fiction should be the Spielberg movie Jaws. Yet the real fictional reference point for our modern-day debt collectors appears to be the 1984 cult film, Repo Man.

And it’s clearly not just the pay-day lenders who have been borrowing techniques from the film – but the Student Loans Company too.

Bogus letters

Repo Man’s narrative centres on a Los Angeles company that repossesses cars, among other things, from the debt-laden borrowers who have fallen behind on their loan payments. Essential to the “Repo Man’s” persuasive armoury is deception and the perceived threat of some force or sanction – a lesson not lost in the ever burgeoning loan business.

The short-term loan market is something of a precarious business model to say the least, especially when it comes to repayments. This, after all, is the new subprime hinterland. In Wongaland, the Repo Man’s threats meet their equivalent in the letter from a respectable law firm.

This strategy started back in 2005, when the likes of Wonga started pursuing those borrowers in arrears through legal firms such as Chainey, D’Amato and Shannon, specialising in debt recovery. But after a few years, the regulators and public discovered that Chainey, D’Amato and Shannon did not exist.

The impression left was that payday loan customers are fair game for the modern Repo Man because of their social and economic vulnerability. And research by Brian Melzer at the Kellogg School of Management in the US, shows that despite claims about the careful screening of loan applicants: “low-to moderate-income households… represent the vast majority of payday borrowers”.

Another credit-dependent, low-income group is also being targeted with legal correspondence by an unscrupulous loan company: university students. In June, it emerged that the SLC had lifted a leaf out of Wonga’s books.

Some 300,000 graduates received letters from a company called Smith Lawson and Company Recovery Services – with the initials SLC – between 2005 and 2014. The letters contained a banner in red stating “Do Not Ignore This Letter”, demanding that if payments were not met within seven days legal action would ensue. Of course, Smith Lawson and Company Recovery Services is a fugazi firm, a fake.

There were calls in parliament for the student victims of these Repo letters to be compensated. Such action would not be out of step with how regulatory authorities have responded to similar practices, mentioned above, by payday loan companies. For example, in late June, Wonga got a £2.6m slap on the wrists and the Financial Conduct Authority ordered the company to compensate 45,000 customers who had been intimidated by the company’s Repo Man letter antics between 2008-10.

The difference between Wonga and the Student Loan Company is that the latter exists chiefly to provide a public service and, more importantly, it is owned by the government. So why did the Student Loan Company stoop to the pay-day loan level of Wonga?

Was it a nudge?

One possibility could be the government using the soft tools of incentives derived from the science of behavioural psychology, or so-called Nudge Theory. But policy champions of nudge regard deception as very un-nudge-like.

The British political scientist Peter John, author of the book Nudge, Nudge, Think, Think, argues that behavioural nudges should be debated and deliberated with the public. Transparency, it seems, is fundamental to nudge, certainly if it is to have public legitimacy.

In fact, key policy evangelists of nudge, Richard Thaler and Cass Sunstein, have looked into how behavioural psychology can curb the irrational inclination towards the accumulation of debt – a behaviour encouraged and promoted by the credit industry. These authors would no doubt approve of the soft-touch regulatory interventions made by such US states as Florida and New Mexico in relation to credit. These states have placed limits on repetitive rollover borrowing from payday lenders in a bid to discourage the accumulation of debt.

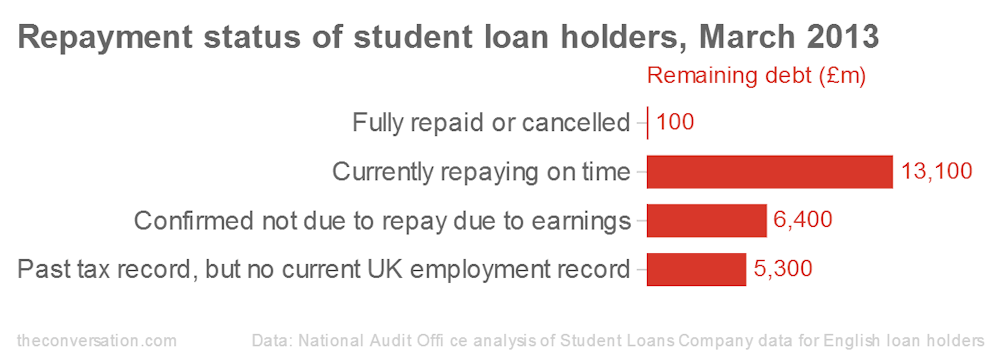

The explanation of why the SLC adopted pay-day tactics is less about psychological models than hard commerce. It is currently facing a business model where there is endemic non-payment on loans by former students. At the end of 2013, the National Audit Office revealed that 368,000 former students who took out student loans owed a total of £5.3bn, as the graph below shows. But this was not a case of co-ordinated mass defaulting: the department for business, innovation and skills had no employment records for all these former students and hence they could not be pursued.

In February 2014, Chris Brodie, previously a senior executive at the investment bank UBS, was appointed as the non-executive chair of SLC. On a modest £50,000 salary Brodie, who also chairs the council of Sussex university, was appointed to modernise the SLC’s computer systems – systems that are clearly deficient.

In the fall-out over the fake debt collection letters at the SLC, Brodie offered his resignation; it was declined. The SLC has subsequently ended its practice of issuing bogus legal threats to ex-students.

Despite the moral and economic hazards surrounding the loans industry, the provision of credit is close to being an inalienable human right. To quote Bud, one of the characters from Repo Man Bud: “Credit is a sacred trust, it’s what our free society is founded on”. Bud of course would say that – without loans he would have no job to recoup loans. It seems credit debt is an evil which has been made a necessity by the modern economy.