Rishi Sunak, the UK prime minister, has indicated that the upcoming UK election will not be until the second half of 2024, but this is just the tip of the iceberg for polling activity in the coming months. This is set to be the biggest election year in history, with polls also in the US and more than 50 other countries around the world, including India and Mexico. In total, over 4 billion people will be casting votes.

How will all this affect the economy and the financial markets? Incumbent politicians have an incentive to call an election when the economy is healthier, to enhance their chances of being re-elected. They often also manipulate taxes and spending to present a (short-lived) rosier picture to voters before polling day.

Yet timing an election is easier said than done. History shows that 18 out of the 31 elections held in the UK since 1900 have taken place during recessions, for instance (and 2024 could be another example). There are also significant gaps between the time any electoral “hand-outs” are implemented and their effects on the economy.

Elections and markets

The effect of elections on financial markets is similarly capricious. On the one hand, it’s well known that investors dislike uncertainty. This would point to lower stock market returns in the run-up to an election, then higher returns after the results are in. Yet the evidence doesn’t entirely support this. A study from 2000, which looked at 33 countries including the US and UK, found evidence of higher returns before elections.

There’s also conflicting evidence about how markets are affected by election results. Some findings show that left-wing victories tend to be associated with lower stock market returns, as investors anticipate higher inflation caused by increased spending and also higher taxes reducing consumption. Yet there’s also evidence of higher stock market returns under Democratic victories in the US.

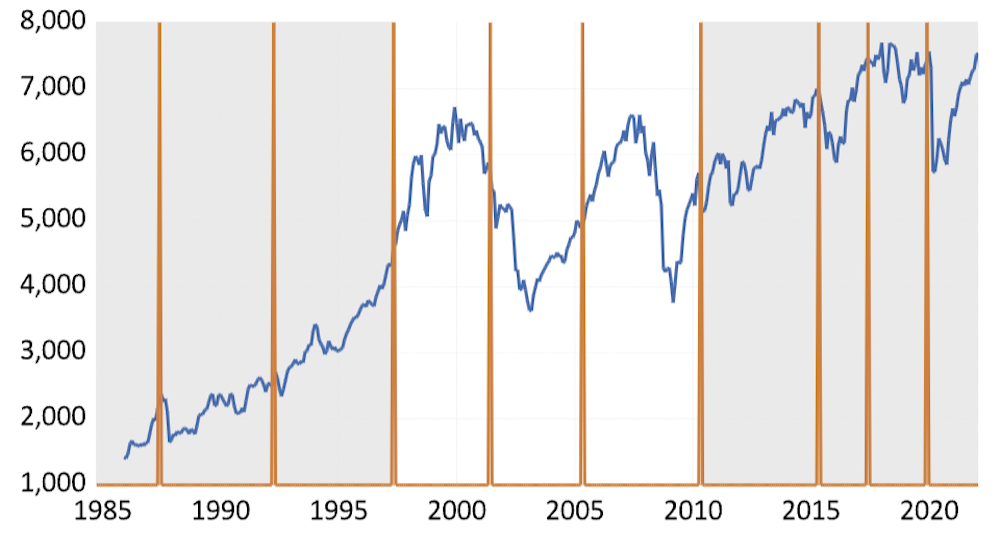

One explanation for these inconsistencies is that it can be difficult to discern a meaningful pattern when elections are relatively rare events. There’s similar inconsistency in the graph below, which plots the UK’s FTSE 100 index against its general elections (marked by the vertical brown lines). It also shows periods of Labour rule in white, and Conservative periods in grey (including the Con-Liberal coalition of 2010-15).

It’s hard to detect a meaningful and long-lasting effect either from the elections or changes in political leadership, particularly as other events can often move markets more. For instance, the dramatic drop in the FTSE in 2020, a few months after the 2019 election, was linked not to Boris Johnson’s landslide victory but to the COVID pandemic.

FTSE 100, political leadership and UK elections

The next figure looks at the US elections and stock market uncertainty, as measured by the Vix index, aka the gauge of investor fear – anything above 20 is considered to represent nervous times. It is true that the index has sometimes peaked in the run-up to elections, but this doesn’t necessarily mean causation. When the Vix reached a record panic-value of 60 in 2008 ahead of the Barack Obama v John McCain election, the nation was going through the global financial crisis and a GDP decline of over 4%.

US elections and stock market uncertainty

One way to attempt to overcome this extraneous noise is to narrow in on the election period. The table below focuses on a three-month window – the months before, during and after an election – to look at the average values of the main financial variables for the UK and the US in the last nine general elections.

Again, however, the results are not particularly revealing. You can see that investors’ uncertainty does tend to increase before elections and decrease afterwards, as shown by the Vix index. Yet this doesn’t lead the FTSE and S&P to follow a consistent pattern. In the UK, stock market returns have been on average positive during an election month for 67% of the time, against lower values before and after elections. The US stock market has tended to be lower before elections, before rising during and also after the elections.

US/UK elections and market behaviour

What about the foreign exchange market? In countries like the US and UK, where the currency is freely traded on exchange markets, it generally falls when investors think the economy will weaken and it rises when they think it will get stronger.

Looking at the British pound and US dollar (using index values that compare them to baskets of other currencies), both have tended to weaken during election months. This seems to support the idea of investor uncertainty before elections. Yet the inconsistency returns when you look at the month after elections, with the dollar usually slightly weakening and the pound slightly strengthening.

What it means

While elections are followed with great interest, these results show that their effect on financial markets is hard to discern, and at most short-lived. Yet that’s not to say the elections will be irrelevant to the markets in 2024.

Given the sheer size and number of countries called to vote and their importance to the financial and also commodities markets, the uncertainty could well push the markets down in the short term. There’s also a risk of financial contagion, where negative shocks propagate across different economies.

In the long run, however, what will ultimately matter for financial markets will not be short-term policies or electoral pledges, but the state of the economy.