Tony Abbott has warned there will be “tough decisions” in tomorrow’s federal budget – but would his government risk an industry and internal backlash by cutting back on multi-billion-dollar fuel tax credits for miners, farmers, trucking companies and others?

While some within the government have been keen to save money by cutting back on the fuel tax credits for off-road use of diesel, Treasurer Joe Hockey has reportedly reassured miners that the multi-billion-dollar fuel tax credits aren’t on his budget cut list. So would that be the right decision?

Today’s Viewpoints: should the government cut fuel tax credits in the budget? Two economists square off on the issue: Richard Denniss argues we should, while Sinclair Davidson argues we shouldn’t.

Richard Denniss:

The fuel tax credit scheme is an almost A$6 billion subsidy each year to industry. With the government saying that the age of entitlement is over, and the age of personal responsibility has begun, it is time for such sentiments to apply to business.

The fuel tax credit scheme rebates excise tax to those businesses that consume diesel on non-public roads.

Some claim that this is fair since they don’t use public roads – but this assumes that this scheme’s purpose is to pay for roads. While more than 50 years ago this was the case, such a link was broken in 1959. Since that time, fuel excise has gone into general revenue and can be used for any expenditure purposes.

There are other very sound reasons to levy an excise tax on fuel.

Economics tells us we should tax negative externalities: that is, we need to discourage the consumption of goods that create negative side effects such as pollution. The consumption of diesel on non-public roads creates the same amount of pollution and so should be subject to the same amount of tax. (Not to mention that we’re subsidising extra greenhouse gas emissions, as I’ll cover shortly.)

The fuel tax credits scheme is a subsidy to business that comes at a high cost to the budget. If the government is serious about ending corporate welfare and saving money, then it should consider cutting back or abolishing this subsidy.

Sinclair Davidson:

Many Australians enjoy receiving their annual tax refund. Having over-paid tax during the year, the Australian Tax Office sends them a cheque. Nobody thinks this is a subsidy; if the government were to propose to simply pocket that money, everyone would clearly see this as constituting an increase in taxation.

The logic underpinning the fuel tax credit works the same way.

Diesel excise was introduced in 1957 to fund public roads. Off-road diesel users were exempted. Since that time government has experimented with various mechanisms to ensure that the exemption isn’t rorted. At present, the administration of the excise gives the rebate an appearence of being a subsidy.

But is the rebate really an industry subsidy? Not according to the people who know best: the government, the Treasury, or the Productivity Commission. Even Chris Riedy in a 2007 Greenpeace Australia Pacific Report agrees the rebate is not a subsidy.

It is true that there is nothing to force our politicians to actually spend the money on roads. This is just another in a long, long line of broken promises. The fact is that section 81 of the Constitution requires all revenue to be paid into one Consolidated Revenue Fund – as such, hypothecated taxes constitute political fiction and fiscal illusion.

If Parliament wants to introduce a new tax on industry, it should do so explicitly and not through administrative contrivance.

Richard Denniss:

While some people would prefer that governments collect no tax, the fact is they do. But the way that fuel tax is collected at the moment means that while some industries pay, others don’t.

From an economic point of view, deciding to exempt a small number of industries from a tax is identical to posting them a cheque equal in size to the value of the tax exemption. That’s why most economists think that a tax exemption and a subsidy are the same thing.

The Abbott government says that it is committed to reducing greenhouse gas emissions, particularly through its direct action plan, which will cost Australians A$2.55 billion over the next four years. That makes the idea of exempting the mining industry from paying tax when they use fuel even less efficient.

A claim made in support of keeping subsidised diesel for some businesses is that diesel is an input into production and governments shouldn’t tax business inputs. This idea, of course, ignores the fact that taxation can be used to discourage the use of something.

But even then the subsidy is not being applied consistently. Trucking companies are charged the excise when moving goods around Australia and they seem perfectly capable of passing it onto their customers. Why is it that this special provision is only applied to a select group of businesses?

Sinclair Davidson:

Those wishing to abolish the scheme need to mount an argument in favour of increased taxation. Superficially there are many good reasons to increase taxation – after all, the previous government has left Australia a massive deficit and growing public debt. There is bipartisan agreement that the budget should be balanced, if not actually in surplus.

Generally, as a matter of policy, government does not tax business inputs. Such a practice would add to business costs and lead to economic distortions.

The economic costs associated with taxation can be quite high and one objective of good tax policy is to minimise those costs.

There is a presumption that fossil fuels have negative externalities and, it could be argued, government should tax those fuels to eliminate the externality.

It is one thing to imagine that an externality might exist; it is quite another to demonstrate that social costs actually exceed social benefits. This can only be done through a careful analysis of actual costs and benefits and not simply asserted.

The challenge to those who want to increase taxation is three-fold. What are the benefits and costs of increased taxation? How much revenue will it raise? And on balance, is it worth increasing taxation?

As things stand the case for increasing taxation, due to a perceived externality, is superficial. Good public policy cannot rely on such simplistic notions.

Richard Denniss:

Sinclair seems to be trying to make something simple seem complicated. Treating all industries the same is the fairest and most efficient way to impose a tax.

The exemption that some industries have from paying fuel excise has more to do with history and political power than good tax design.

In an era when even Coalition governments say they want to reduce greenhouse gas emissions, the existing diesel fuel rebate for the mining industry makes even less sense. Even Sinclair agrees that burning fossil fuels create negative externalities and diesel burnt off-road creates the same amount of greenhouse gases and other pollution as when it is burnt on the road.

Economics also teaches that you should level the tax as close as possible to the externality to encourage behavioural change. The externality has created an inefficient outcome and the purpose of the tax is to correct that. To claim that taxing diesel inputs is inefficient misunderstands the problem and the solution. It also forgets that many businesses already have their diesel taxed, such as businesses in the trucking industry.

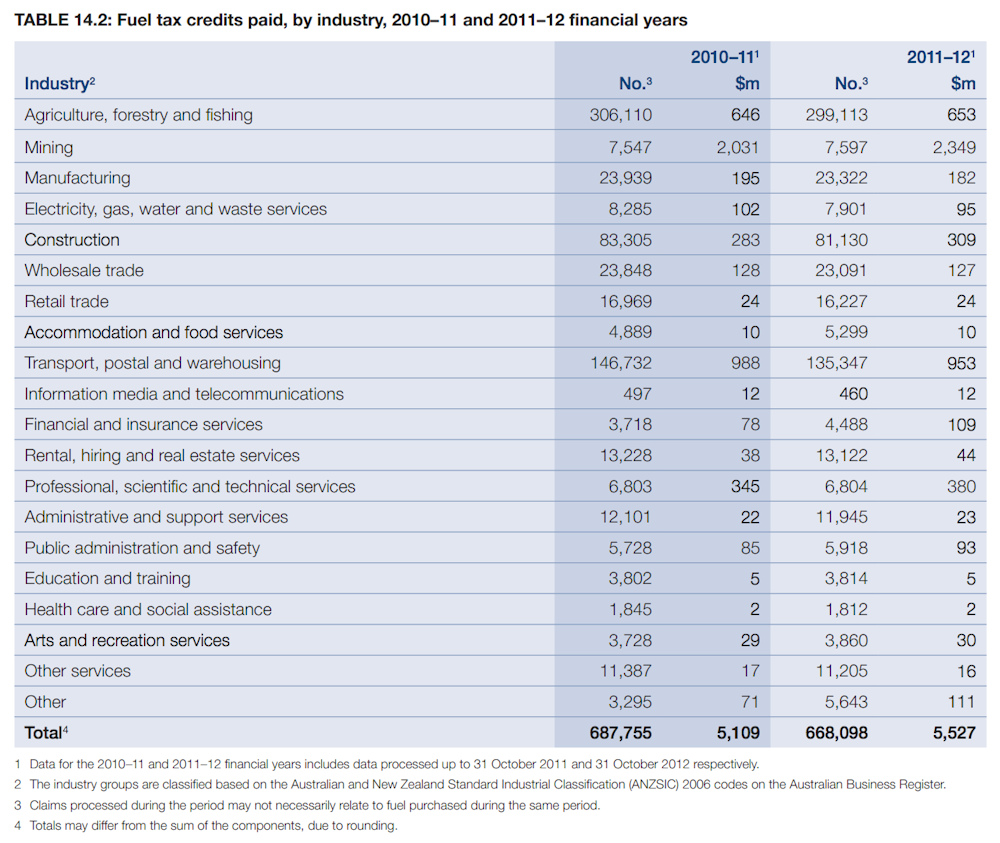

The fuel tax credit scheme is a subsidy that will shortly pass A$6 billion per year. Fuel excise has nothing to do with road construction and there are very good economic reasons for taxing diesel use. It’s time that this privileged group of businesses be taxed the same as everyone else.

Sinclair Davidson:

The fuel tax credit scheme is not an example of corporate welfare – it is not a subsidy – and the case for increasing taxation is superficial. I advocate that it is left alone.

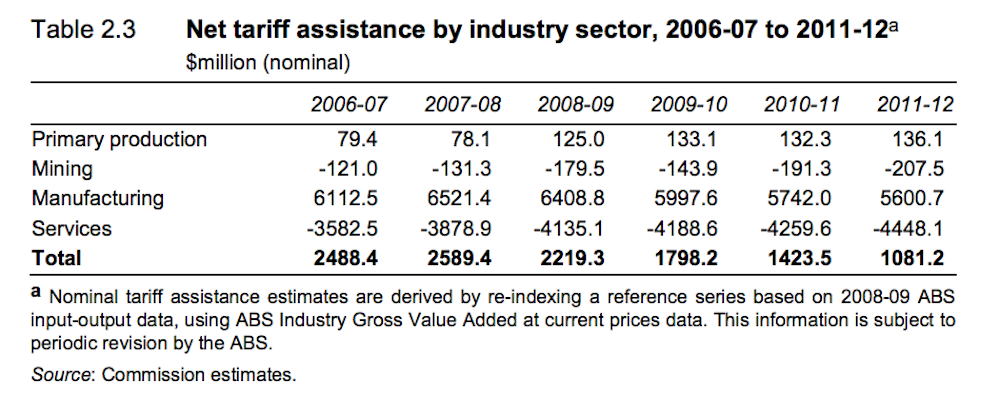

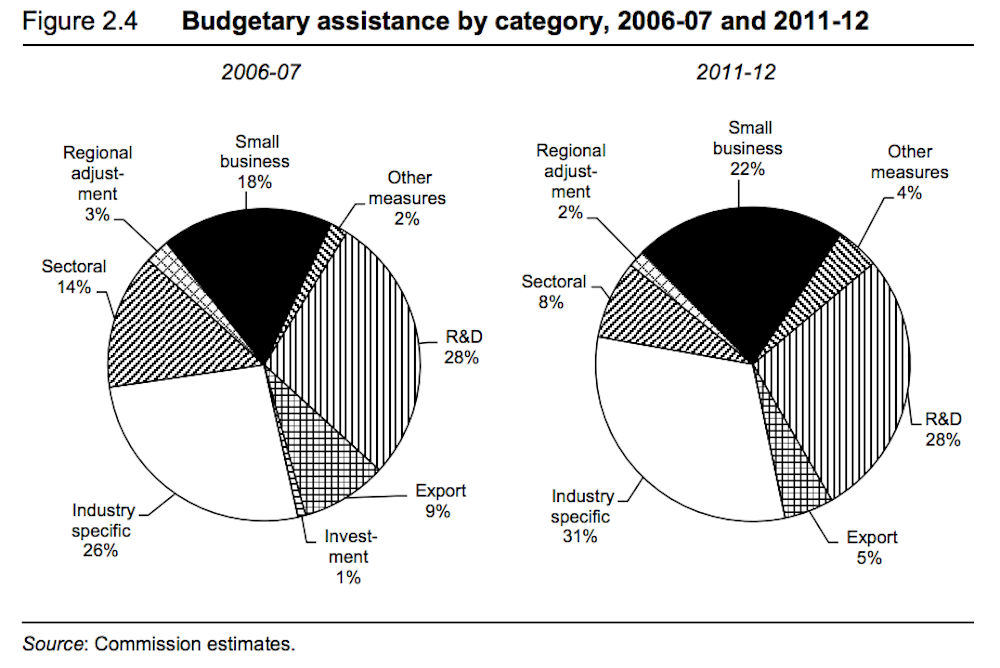

On the other hand, the age of entitlement is increasingly unaffordable and should be substantially wound back. A good place to start looking for examples of corporate welfare is the Productivity Commission’s annual Trade and Assistance Review reports.

According to the Productivity Commission there is a lot of tarriff assistance – especially to manufacturing, as you can see above – that can be reduced.

That’s not to mention the nearly A$10 billion in outlays and tax expenditures that can be cut.

Mind you: a lot of that corporate welfare consists of R&D expenditure, and subsidies to “clean energy” industry assistance (see page 25) … and don’t forget the rural assistance programs.

That’s the real problem here. One man’s unjustifiable subsidy is another man’s important government intervention. Declaring the end of entitlement is easy. But actually cutting entitlement is hard – and the devil is in the detail.

Should the federal government cut the fuel tax credits scheme, or leave it as it is? Share your comments below.