When the nation’s No. 1 and No. 4 property and casualty insurance companies – State Farm and Allstate – confirmed that they would stop issuing new home insurance policies in California, it may have been a shock but shouldn’t have been a surprise. It’s a trend Florida and other hurricane- and flood-prone states know well.

Insurers have been retreating from high-risk, high-loss markets for years after catastrophic events. Hurricane Andrew’s unprecedented US$16 billion in insured losses across Florida in 1992 set off alarm bells. Multibillion-dollar disasters since then have left several insurers insolvent and pushed many others to reevaluate what they’re willing to insure.

I co-direct the Center for Emergency Management and Homeland Security at Arizona State University, where I study disaster losses and manage the Spatial Hazard Events and Losses database (SHELDUS). As losses from natural hazards steadily increase, research shows it’s not a question of if insurance will become unavailable or unaffordable in high-risk areas – it’s a question of when.

Reinsurers are worried

Insurance is a vehicle to transfer risk. When an individual buys an insurance policy, that person pays to transfer the risk of expensive repairs to the insurer if the home is damaged by a covered event, like a fire or thunderstorm. Most policyholders don’t experience major disasters, so insurance companies make money.

However, disasters are extremely costly when they do occur, so insurers also buy their own insurance, called reinsurance.

Reinsurance costs have been rising fast in response to expensive disasters around the world in recent years. Reinsurers’ risk-adjusted property-catastrophe prices rose 33% on average at their June 1, 2023, renewal, after a 25% rise in 2022, according to reinsurance broker Howden Tiger’s analysis.

If prices are too high and insurers can no longer transfer excessive risk to the reinsurance market, they are stuck “holding the risk” – meaning the cost of claims when disasters strike. A big enough disaster can put insurance companies out of business, or they can decide to leave the state, as seen in California, Louisiana and elsewhere.

Responsible insurers are not in the business of gambling, so they do what State Farm and Allstate did: They reevaluate their portfolios – the various lines of insurance they offer, such as auto, life, property insurance and health insurance – and their prices. Insurance is a highly data-driven business and uses some of the most sophisticated climate and risk modeling in the world to forecast future risks, including the likelihood a property will be damaged by wildfire or other natural hazards.

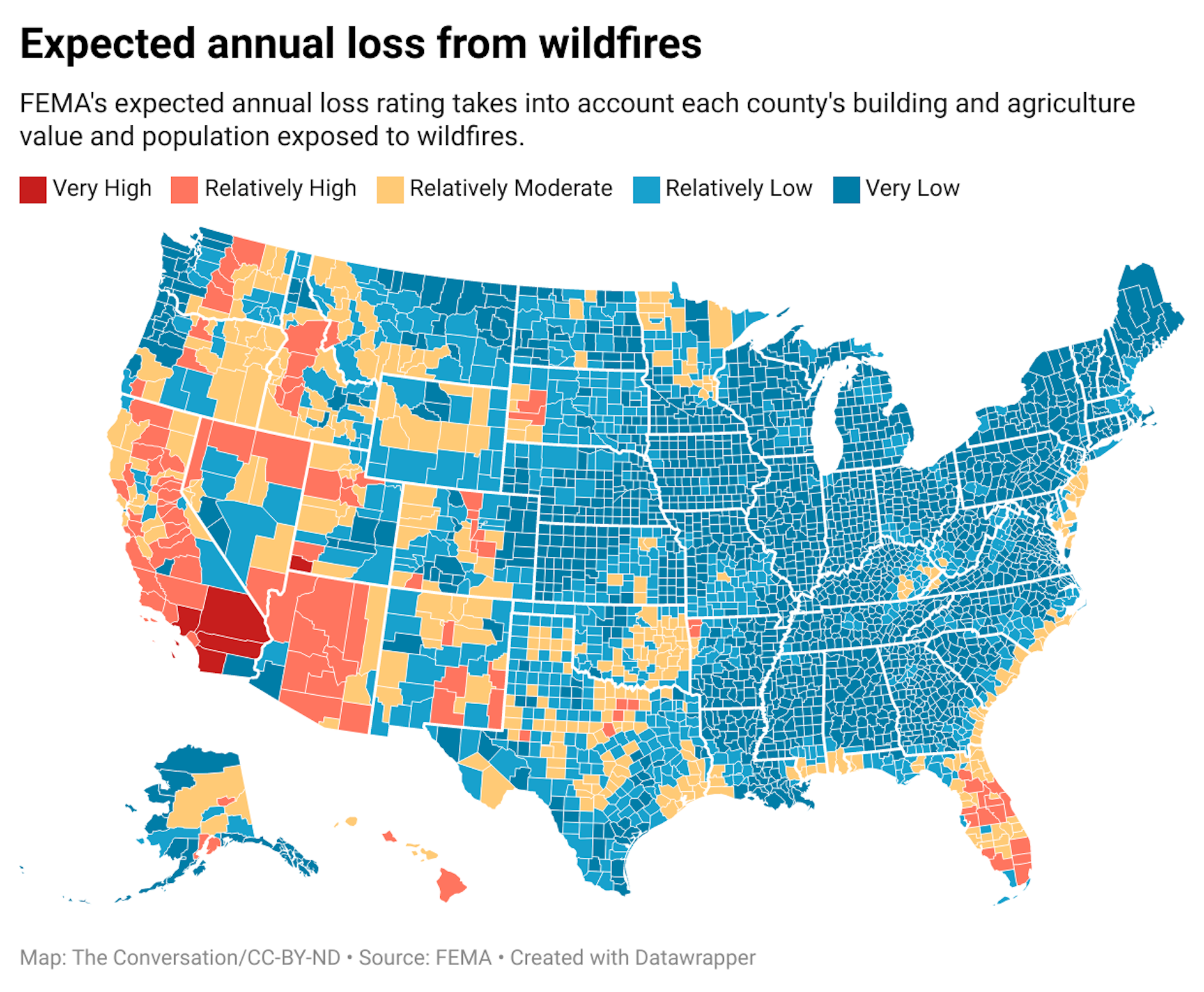

State Farm cited “catastrophe exposure” as a reason for ending new high-risk personal and commercial property and casualty policies in California. That refers to the likelihood that costly claims would exceed the risk State Farm was willing to accept.

{kind=link}

Why drop only California?

So, why did State Farm and Allstate only stop new policies in California and not in other wildfire-prone states like Colorado or Arizona?

The answer can only be speculative since State Farm or Allstate don’t publicly disclose their exposure. That’s calculated based on how many personal and commercial property and casualty policies the company holds in the state, particularly in the wildland-urban interface where fire risk is higher, and at what value.

State Farm did cite California’s increasing wildfire risk and home construction prices, but there are other influences to consider.

One is state insurance regulations that can limit premium increases, prohibit policy cancellations and require certain levels of coverage. Insurer Chubb’s chief executive mentioned restrictions that left it unable to charge “an adequate price for the risk” as part of the reason for its 2022 decision to not renew policies for expensive homes in high-risk areas of California. California also has a unique “efficient proximate cause” rule that forces property insurers to also cover post-fire flooding, such as mudslides. Rainy winters like 2023’s often trigger destructive mudslides in wildfire burn areas.

What happens now?

When insurers pull out of a community, residents and companies without access to property and casualty insurance are left holding their own risk – and paying the price if a disaster strikes. From a societal and political perspective, that’s a problem.

Residents and businesses without insurance tend to recover more slowly. Uninsured residents often depend on donations, loans or federal individual assistance. The latter, however, is only available for catastrophic disasters and covers only immediate needs.

To fill the gap and provide access to insurance, states including California, Florida, Louisiana and Texas have created either private or public insurance options of last resort with generally very pricey premiums.

Residents covered by these options transfer their risk to the state, such as in Louisiana and Florida – meaning state taxpayers, who fund the state insurance programs, hold the risk directly or indirectly. In California, the privately insured FAIR Plan, in existence since 1968, wrote close to 270,000 policies in 2021, nearly double the number in 2018.

Similarly, anyone purchasing flood insurance through the National Flood Insurance Program since 1968 is transferring their risk to federal taxpayers. The NFIP currently insures almost $1.3 trillion in value across 5 million policies.

Politicians are not catastrophe risk experts, though, and do not make decisions based on data alone.

In the short term, I expect that insurance pools, as well as federal- and state-run insurers of last resort, will add more policies, and that state legislators will incentivize the return of insurers. But while the political willingness to support such a trend exists, the financial resources do not.

The National Flood Insurance Program has plenty of lessons to teach about the challenges of balancing exposure and keeping premiums affordable: It is more than $20 billion in debt. Texas has resorted to charging insurers operating in the state to help cover its program’s costs.

Fixing insurance starts with the property itself

Despite the risk of properties becoming uninsurable, communities today continue to permit development in floodplains, along coastlines and in the wildfire-prone wildland urban interface. Inadequate building codes allow developers to build homes that cannot withstand severe weather. These practices have placed millions of residents and the things they value in harm’s way.

As climate change continues to dial up the frequency and severity of natural hazards, there are some steps states and communities can take involving property to lower the risk:

Make smarter land use choices and limit development in high-risk areas to avoid placing people and the things they value in harm’s way.

Adopt more stringent building codes and safety standards at state and community levels.

Price risk into home sales, either through an insurance contingency that allows the buyer to withdraw when they cannot secure insurance or lower assessed property values for real estate in high-risk areas, which can dissuade builders and buyers.

Require comprehensive disclosures of all present and future risks along with historic claims associated with a property to educate potential buyers.

Make risk information accessible and understandable. My research shows that most people have a hard time fully grasping how likely they are to be affected by a catastrophic event. They need better tools that communicate the information in a way that resonates with them.

Help residents in high-risk areas relocate through buyouts and managed retreat that returns the land to nature or public uses such as parks.