Back in July last year Queensland Premier Campbell Newman was in a very black mood. All was gloom and doom in the Sunshine State, as he warned Queensland was “on the way to being bankrupted” without tough action. Back then, his government was shaping up to do a Jeff Kennett, painting the grimmest of pictures that would justify massive cuts to the Queensland public sector, just as the former Victorian premier did in his first term in power.

Yesterday was the day when it was all meant to come together, with Newman having to make the biggest call of his political life. In announcing his government’s response to an audit of the state’s finances, he had to decide whether his Government would support the sale of major pieces of Queensland’s “family farm” - particularly the state’s multi-billion-dollar power assets.

To the surprise of many, and despite a lot of pressure from the money men at the top end of town, Newman declared “we will save the farm”, rather than “taking the easy way out and having a fire sale of assets”. Instead, he outlined a much quieter and in some ways craftier program of outsourcing and competitive tendering. Private operators are likely to end up leasing and running more state-owned services, from ports, trains and buses, through to health care, including elective surgeries.

Queenslanders are no friend of privatisation, that’s for sure. Only 14 months ago, they savagely punished the Bligh Labor government for going down this path without a mandate. It would need a pretty strong case to convince a seasoned politician like Newman to try that option again. So how strong was the case in favor of a fire sale?

A closer look at the books

Just days after being elected, the Newman government appointed former federal Treasurer Peter Costello to lead a A$2.2 million audit of Queensland’s finances. The 1000-page final report - released in full yesterday - recommended selling the state’s electricity and port assets to raise more than A$25 billion and rapidly reduce debt.

Costello continued the hard sell right up until the last moment, including inside the cabinet room for his final briefing to MPs. In an article in the Australian Financial Review that cited a debt figure of A$82 billion, Costello declared: “Queensland has a problem. Its credit rating has been downgraded, it’s paying higher and higher interest costs and something has got to happen… If it doesn’t change, it’s just going to get worse and worse.”

But just how gloomy is the Sunshine State’s budget outlook?

While A$82 billion sounds like a lot of debt, the picture was always more complex than Costello would have us believe.

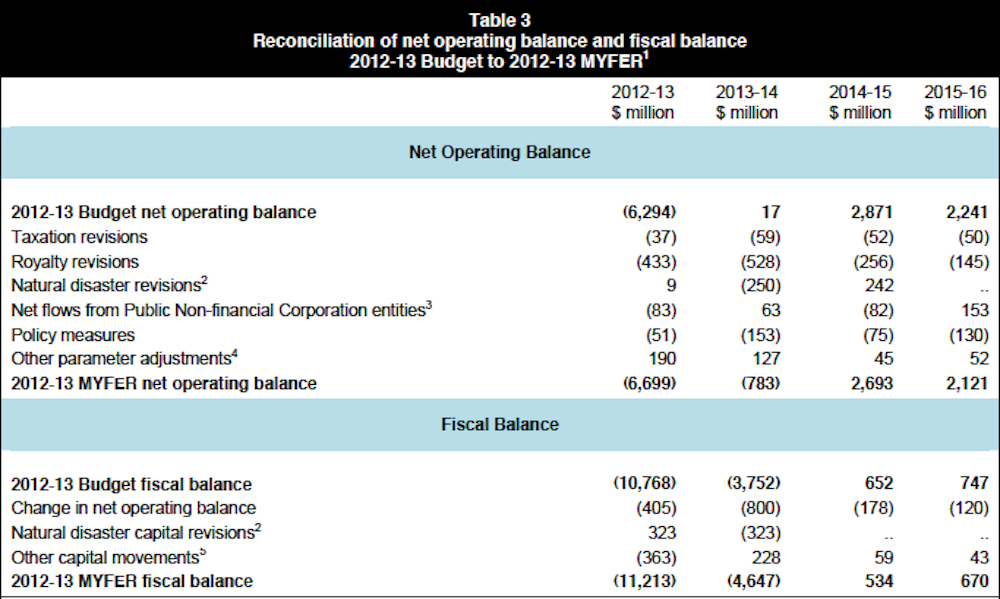

This table is taken from last December’s Mid-Year Economic and Budget Update. It shows the state’s general government balance sheet for the period from 2011/12 through to 2015/16. While it is true that gross debt or total liabilities will exceed $80 billion this financial year, the net debt figure (or gross debt less financial assets) is very different.

The Queensland general government sector in fact had no net debt in 2011/12. And while net debt is projected to grow to a peak of A$9.6 billion by 2013/14, it then starts to fall and then continues its downward trajectory.

Still, you might say, A$9.6 billion is a lot of money to owe. That would be true were we talking about a household or a business - but not for the Government of Queensland, which can tax its citizens to pay the bills and tax them more heavily if it really has to do so. Queensland is, after all, one of Australia’s lowest-taxed jurisdictions, with its per capita taxation in 2012/13 more than $450 below than the Australian average.

But according to Costello’s Commission of Audit, net debt is not the best measure of the state’s liabilities. It includes the financial assets that have been built up to fund the state’s super schemes and which therefore are not available to cover the gross debt on issue. It recommends a different measure, called net financial liabilities:

“As the net debt measure includes investments, it takes account of the large investments Queensland uses to offset its superannuation liability, it does not take account of the liabilities. Under existing Government policy, these investments are held to meet the State’s superannuation liability. Because these investments are not available to reduce gross debt, net debt is not a suitable metric to target in setting an appropriate fiscal strategy… The Commission consider that the most suitable measure of debt is the concept of net financial liabilities”.

The State’s net financial liabilities (A$39 billion in 2011/12) are much higher than its net debt, and it is this that needs to be paid down. But how good is this as a measure of the State’s balance sheet? The answer is not very, because it ignores the physical and other assets that are crucial to the balance sheet equation (worth a cool A$182 billion in 2011/12).

What’s a worthier economic measure?

Net worth is generally considered to be a better measure, for it includes all assets and liabilities and not just those that are financial. Far from being in trouble, Queensland is in fact well and truly in the black according to this measure, with a net worth in the general government sector exceeding A$170 billion in 2011/12, climbing steadily to almost A$180 billion not long after the next scheduled election.

All this is not to say that the Queensland budget is in fine shape. Far from it. But its problems stem not from its balance sheet but the substantial gap between operating income and expenses. Queensland’s operating budget shifted from surplus to deficit in four very difficult years, when revenues went into an unexpected spin and have yet to fully recover. This year the deficit is tipped to exceed A$11 billion, which is very large on any measure and would seem to be genuine cause for concern.

However, this includes one-off expenses associated with flood damage that cost more than A$4 billion. It also includes almost A$1 billion set aside for redundancies arising from Newman’s first budget. When these are excluded, the deficit is a more manageable A$6.3 billion. This is still large, but importantly is not tipped to last forever.

The Mid-Year Economic and Budget Update also shows that the operating account is projected to return to surplus by 2014/15, with the corrective measures already put in place being enough to turn the ship around without the need for any more drastic action.

If Queensland’s debt is not large, its net worth is positive, and the government by its own admission reckons it is on track to achieve its financial principles, why bother with a massive asset sales program that would antagonize the people?

Far better to be crafty and privatise services in other ways, through an outsourcing and competitive tendering program that can turn the public sector inside out, but hopefully jeopardise fewer MPs’ seats. For Premier Campbell Newman, who resides in a marginal electorate himself, hearing that the money men are disappointed may not be such a bad thing.